IRS Form 1139 Instructions

Corporate taxpayers can apply for a tentative refund based upon changes to prior-year returns by filing IRS Form 1139, Corporation Application for Tentative Refund.

In this article, we’ll help you better understand what you need to know about IRS Form 1139, including:

- How to complete and file IRS Form 1139

- When you can make an eligible refund claim using this tax form

- Frequently asked questions

Let’s begin with a step by step overview on how this tax form works.

Table of contents

How do I complete IRS Form 1139?

This one-page tax form is relatively straightforward. Let’s begin at the top with the taxpayer information fields.

Taxpayer information

At the top of the form, enter information about the corporation, beginning with the corporation’s name.

Taxpayer name

Enter the name of the corporation.

Employer identification number

Enter the corporation’s employer identification number (EIN) here.

Number and street address

Enter the street address of your office location here.

City or town, state and zip code

Enter the city, state, and zip code of your corporate office location.

Date of incorporation

Enter the date of incorporation in this field.

Daytime telephone number

Use this space to provide a telephone number where the IRS can reach the corporate point of contact.

Background information

Lines 1 through 10 contain additional information about the circumstances surrounding the corporation’s tentative refund claim.

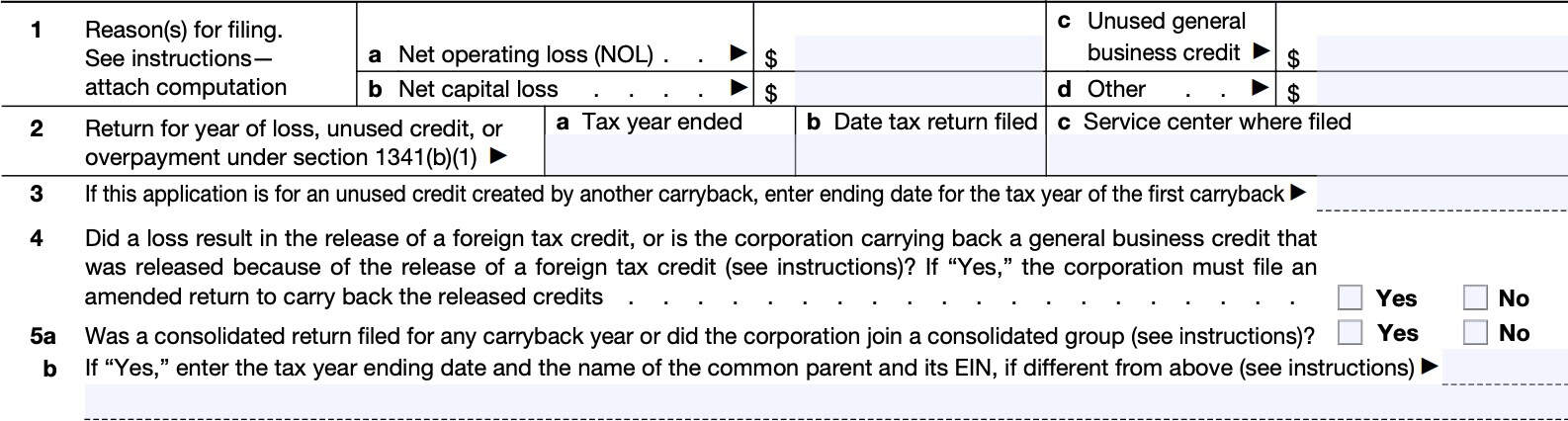

Line 1: Reason(s) For Filing

Enter your reason or reasons for filing IRS Form 1139. We’ll cover each reason in detail.

Line 1a: Net operating loss

If the corporation is claiming a tentative refund based on the carryback of any net operating losses (NOLs) discussed under Definitions and Special Rules, include the carryback amount here.

Attach any required statements.

Net operating losses defined

For corporations, a net operating loss (NOL) is the excess of the deductions allowed over gross income, computed with the following adjustments:

- The NOL deduction for an NOL carryback or carryover from another taxable year is not allowed

- The dividends-received deductions for dividends received from domestic and foreign corporations and for dividends received on certain preferred stock of a public utility are computed without regard to the limitation on the aggregate amount of deductions under IRC Section 246(b)

- The dividends-paid deduction for dividends paid on certain preferred stock of a public utility is computed without regard to the limitation under IRC Section 247(a)(1)(B).

- No deduction of qualified business income (QBI) under IRC Section 199A is allowed.

- The Section 250 deduction for foreign based intangible income is not allowed.

NOL carrybacks

For losses incurred in tax years beginning after December 31, 2020, only the following losses can be carried back:

- Farming losses

- Insurance company losses (except for life insurance companies)

The NOL carryback period is 2 years.

Line 1b: Net capital loss

Generally, a net capital loss can be carried back 3 years and treated as a short-term capital loss in the carryback year.

A corporation may carry back the net capital loss only to the extent that the loss does not increase or produce an NOL in the tax year to which it is carried.

For special rules for capital loss carrybacks, see Internal Revenue Code Sections 1212(a)(3) and (4).

Line 1c: Unused general business credit

If the corporation is claiming a tentative refund based on a carryback of an unused general business credit (GBC), then attach a copy of the appropriate credit form for the tax year in which the credit arose.

Except as provided in IRC Section 39(d), an unused GBC can be carried back 1 year.

Recalculate the tax credit for the carryback year on IRS Form 3800, or the applicable credit form.

Line 1d: Other

Complete this line if filing Form 1139 to claim a tentative refund based on an overpayment of tax due to a claim of right adjustment under IRC Section 1341(b)(1).

Line 29 contains additional instructions.

Line 2: Return for year of loss

Enter information about the tax return filed for the year of loss, unused credit, or overpayment under IRC 1341(b)(1).

Line 2a: Tax year ended

Enter the tax year in Line 2a.

Line 2b: Date tax return filed

In Line 2b, enter the date that you filed the tax return.

Line 2c: Service center where filed

Enter the IRS service center where the corporation filed this tax return.

Line 3

If this application is for an unused credit created by another carryback, enter ending date for the tax year of the first carryback.

Line 4

Did a loss result in the release of a foreign tax credit, or is the corporation carrying back a general business credit that was released because of the release of foreign tax credits? Answer Yes or No.

If Yes, the corporation must file an amended tax return to carry back the released tax credits.

Foreign taxes taken as a credit in a prior year can be reduced to zero by the carryback of an NOL or a net capital loss on Form 1139.

Filing an amended tax return

A corporation must file Form 1120X (or other amended return) instead of Form 1139 to carry back a prior year foreign tax credit released due to an NOL or net capital loss carryback.

Line 5a

Did the corporation file a consolidated return for any carry back year, or did the corporation join a consolidated group? Answer Yes or No.

Line 5b

If you answered Yes to Line 5a, then enter the following information, if different from the information already provided

- Tax year ending date

- Name of common parent

- Common parent’s EIN

Line 6a

If the corporation ever filed IRS Form 1138 to request an extension of time to file the corporation’s income tax return for the tax year of the NOL, did the IRS grant the extension? Answer Yes or No.

Line 6b

If you answered Yes in Line 6a, enter the tax return’s new due date.

Line 6c

If you previously filed IRS Form 1138, enter the filing date in Line 6c.

Line 6d: Unpaid tax

In Line 6d, enter the amount of unpaid tax for which the corporation’s tax extension remains in place.

Line 7: Date of accounting period change

If the corporation changed its accounting period, enter the date that the IRS granted permission to change.

Line 8: Date of dissolution

If this form is an application for a dissolved corporate entity, then enter the dissolution date.

Line 9

Has the corporation filed a petition in Tax Court for the tax year or years to which the carryback claim applies? Answer Yes or No.

Line 10

Is any part of the tax decrease due to a loss or tax credit resulting from a reportable transaction? Answer Yes or No.

If Yes, attach a copy of the corporation’s reportable transaction disclosure statement, known as IRS Form 8886.

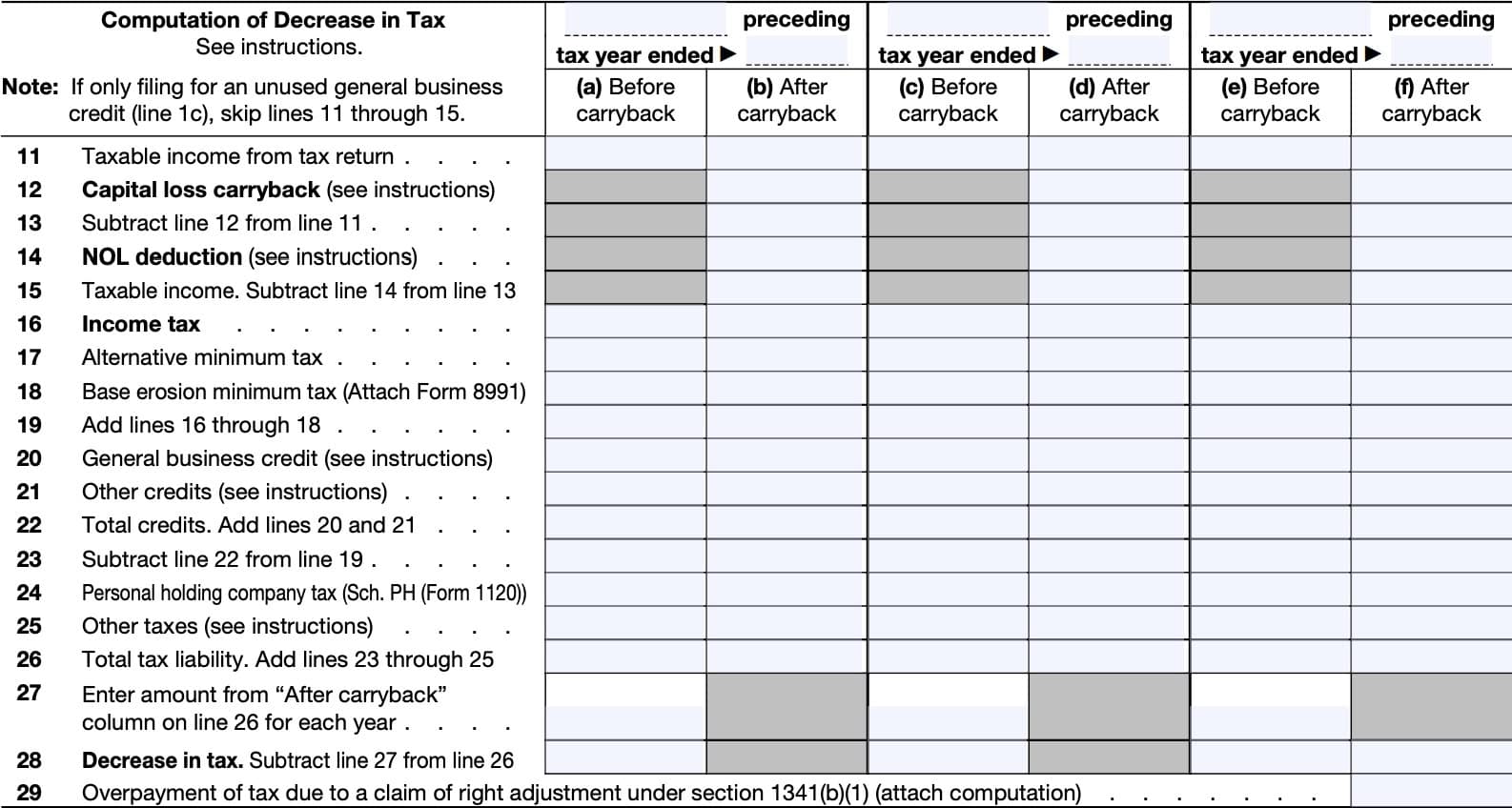

Computation of tax decrease

In Lines 11 through 29, we’ll compute the tax decrease that will justify your refund claim. There are 3 sets of columns, for up to 3 separate tax years.

Each tax year has the following columns:

- Before carryback: Columns (a), (c), and (e)

- After carryback: Columns (b), (d), and (f)

In columns (a), (c), and (e), enter the amount for the applicable carryback year as shown on your original or amended return or as adjusted by the IRS.

Use columns (a) and (b), (c) and (d), or (e) and (f) to enter amounts before and after carryback for each year to which the loss is carried. Start with the earliest carryback year. Use the remaining pairs of columns for each consecutive preceding year until the loss is fully absorbed.

Enter the ordinal number of years the loss is being carried back and the date the carryback year ends in the spaces provided above columns (a) and (b), (c) and (d), or (e) and (f).

Example

For example, if the loss year is the 2023 calendar year and the loss is carried back 2 years, enter “2nd” and “12/31/21” in the spaces provided above columns (a) and (b).

After making the entries, it reads “2nd preceding tax year ended 12/31/21.”

Carryback of unused general business credit

If you are only carrying back an unused general business credit, and nothing else, then you may skip Lines 11 through 15 and begin on Line 16. Otherwise, go to Line 11.

Line 11: Taxable income from tax return

In columns (b), (d), and (f), enter the amounts from columns (a), (c), and (e), respectively.

Line 12: Capital loss carryback

Enter the capital loss carryback. However, do not enter more than capital gain net income.

Capital gain net income

Determine capital gain net income by using the following steps:

- Calculate capital gain net income without regard to the capital loss carryback of the loss year or any later year. Attach a copy of Schedule D (Form 1120) for the carryback year.

- Enter the amount of the capital loss carryback as a positive number on Line 12.

When carrying over a net capital loss to a later tax year, reduce the amount of the net capital loss that can be used in the later years by the amount of the net capital loss deductions used in the earlier years.

For details on capital loss carrybacks, see IRC Section 1212(a)(1).

Line 13

Subtract Line 12 from Line 11. This represents the amount of income available for applying NOL deductions.

Line 14: NOL Deduction

Enter the NOL deduction applicable for each year in Line 14.

Tax years beginning before January 1, 2021

For tax years beginning before January 1, 2021, the NOL deduction is the total of:

- NOL carryforwards to that year, plus

- NOL carrybacks to that year

Tax years beginning after December 31, 2020

For tax years beginning after December 31, 2020, the NOL deduction for the year cannot exceed the

aggregate amount of NOLs arising in tax years beginning before January 1, 2018, carried to that year plus the lesser of:

- The aggregate amount of NOLs rising in tax years beginning after December 31, 2017, carried to that tax year; or

- 80 percent of the excess over an NOL carryover to the tax year from tax years beginning before January 1, 2018, if any, of taxable income determined without any of the following:

- NOL deduction

- Section 199A deduction (QBI deduction), or

- Section 250 deduction

An exception applies for NOLs from insurance companies that are not life insurance companies. The 80% taxable income limit does not apply for these entities.

NOL carryback rules

Unless the corporation has elected to waive the carryback or elected to exclude IRC Section 965 years from the carryback period, NOLs are first applied to the earliest year in the carryback period.

Any unused amount is carried to the next tax year in the carryback period. Any amount of the loss not used during the carryback period is carried forward.

Line 15: Taxable income

Subtract Line 14 from Line 13, then enter the result for each column. This represents the corporation’s taxable income for that year.

Line 16: Income tax

In columns (b), (d), and (f), enter the recalculated income tax after accounting for the carryback(s).

See the instructions for the corporate income tax return for the applicable year for details on how to figure the income tax. Attach a computation of the refigured tax.

Account for Section 1561 limitations when refiguring the income tax.

Line 17: Alternative minimum tax

For columns (b), (d), and (f), refigure the alternative minimum tax, if applicable. Complete and attach IRS Form 4626 for 2017 or earlier tax years.

As part of the Tax Cuts and Jobs Act, corporations are no longer subject to alternative minimum tax for 2018 and subsequent tax years.

Line 18: Base erosion minimum tax

Enter any base erosion minimum tax applicable for each tax year in Line 18, in the respective column. If applicable, attach a copy of IRS Form 8991 for each tax year.

Base erosion minimum tax

The base erosion minimum tax applies to corporations that have:

- Average annual gross receipts exceeding $500 million for the 3 preceding tax years, and

- Deductions paid or accrued to foreign related parties in excess of 3% of their total deductions

- 2% in the case of certain banks or registered securities dealers

The base erosion minimum tax does not apply to the following entities:

- Regulated investment companies (RICs)

- Real estate investment trusts (REITs)

- S corporations

IRC Section 59A contains additional information about the base erosion minimum tax.

Line 19

Add the following:

Enter the total for each column in Line 19.

Line 20: General business credit

In columns (b), (d), and (f), enter the total of the corrected general business credits (GBCs). Attach all

applicable forms used to redetermine the GBC for each column.

If an NOL carryback or a net capital loss carryback eliminates or reduces a GBC in an earlier tax year, the released GBC can be carried back 1 year.

Line 21: Other credits

See the corporation’s tax return for the carryback year for any additional credits that will apply in that tax year.

If any entry appears on Line 21, attach a statement identifying the credits claimed.

Line 22: Total credits

Add Lines 20 and 21 for each column. Enter the total here.

Line 23: Tax after credits

Subtract Line 22 from Line 19. Enter the total here.

Line 24: Personal holding company tax

Enter the amount of any personal holding company tax, as calculated on Schedule PH on IRS Form 1120.

Line 25: Other taxes

Enter other taxes that might apply here.

If any entry appears on Line 25, attach a statement identifying the credits claimed.

Line 26: Total tax liability

Add the following:

Enter the total in each column on Line 26.

Line 27

In columns (a), (c), and (e), enter the Line 26 amount, marked “After Carryback,” for columns (b), (d), and (f), respectively.

Line 28: Decrease in tax

Subtract Line 27 from Line 26 for each column. This reflects the tax decrease for each tax year.

Line 29: Overpayment of Tax Due to a Claim of Right Adjustment Under Section 1341(b)(1)

For a tentative refund based on an overpayment of tax under IRC Section 1341(b)(1), enter the overpayment on Line 29.

Attach a computation showing the information required by Treasury Regulations Section 5.6411-1(d).

Taxpayer signature

At the bottom of the form, a corporate officer must sign, date, and enter their title. This person affirms, under the penalties of perjury, that this is an eligible refund claim, and that the statements are true, correct, and complete.

A paid tax preparer will complete the Paid Preparer Use Only Section with the following information:

- Tax return preparer’s name & PTIN

- Firm’s name, EIN, and address

Filing considerations

Below are some filing considerations when applying for a quick tax refund using IRS Form 1139.

When to file IRS Form 1139

Generally, the corporation must file IRS Form 1139 within 12 months of the end of the tax year in which an net operating loss (NOL), net capital loss, unused credit, or claim of right adjustment arose.

The corporation must file its income tax return for the tax year no later than the date it files IRS Form 1139.

Where to file IRS Form 1139

File IRS Form 1139 with the Internal Revenue Service Center where the corporation files its income tax return. However, do not file IRS Form 1139 with the corporate tax return.

What to attach to your IRS Form 1139

Attach all of the following, as applicable, for the year of the loss or tax credit:

- The first two pages of the corporation’s income tax return.

- All other forms and schedules from which a carryback results

- Examples include Schedule D, IRS Form 3800, etc.

- All copies of IRS Forms 8886, Reportable Transaction Disclosure Statement, attached to the corporation’s tax return

- Any applicable election statement

- All carryback year forms and schedules for which items were refigured.

- IRS Form 8302, Electronic Deposit of Tax Refund of $1 Million or More

- Electronic deposits can be made only for a carryback year for which the refund is at least $1 million

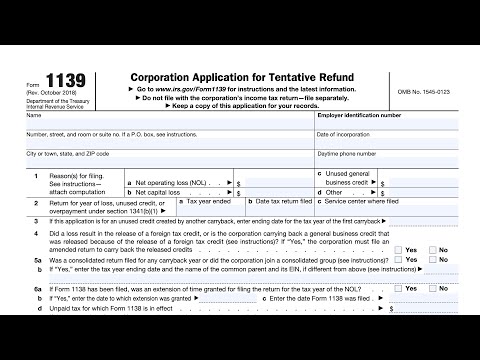

Video walkthrough

Walk through IRS Form 1139, step by step, in this YouTube video!

Frequently asked questions

A corporation may file IRS Form 1139 to claim a quick refund of taxes from the carryback of a net operating loss, net capital loss, unused general business credit, or certain tax overpayments which result in a lower tax liability than allowed in the original corporate return.

S corporations cannot complete IRS Form 1139. However, S corporation shareholders may apply for tentative refund based upon carrybacks reported to them by the S corporation by filing IRS Form 1045, Application for Tentative Refund.

No. Do not file IRS Form 1139 with any federal income tax returns. However, you may file an amended tax return to make an eligible refund claim as a result of a carryback that produces a lower income tax bill.

Where can I find IRS Form 1139?

You may find IRS Form 1139 and other applicable tax forms on the Internal Revenue Service website. For your convenience, we’ve attached the most recent version of IRS Form 1139 here, in this article.