IRS Form 12203 Instructions

If you’ve recently received an audit letter from the Internal Revenue Service, and you don’t agree with the IRS auditor decision, you can bring your tax disputes to the IRS Independent Office of Appeals by filing IRS Form 12203, Request for Appeals Review.

In this article, we’ll go over everything you need to know about this tax form, including:

- How to complete and file IRS Form 12203

- When you can use IRS Form 12203 to make your appeals request

- Appeals situations where IRS Form 12203 is not appropriate

Let’s begin by walking through this one-page tax form, step by step.

Table of contents

How do I complete IRS Form 12203?

For your convenience, we’ve broken this form down into 3 sections:

- Taxpayer information

- Disagreed items

- Signature

Let’s take a closer look at each section, beginning with the taxpayer information fields.

Taxpayer information

Before entering your taxpayer information, take a moment to read the prompt at the top of Form 12203:

This form is to be used to request an Appeals review upon completion of an examination (audit) if you do not agree with our proposed changes from the audit.

In other words, be sure that this is the correct form before you begin to enter your contact information.

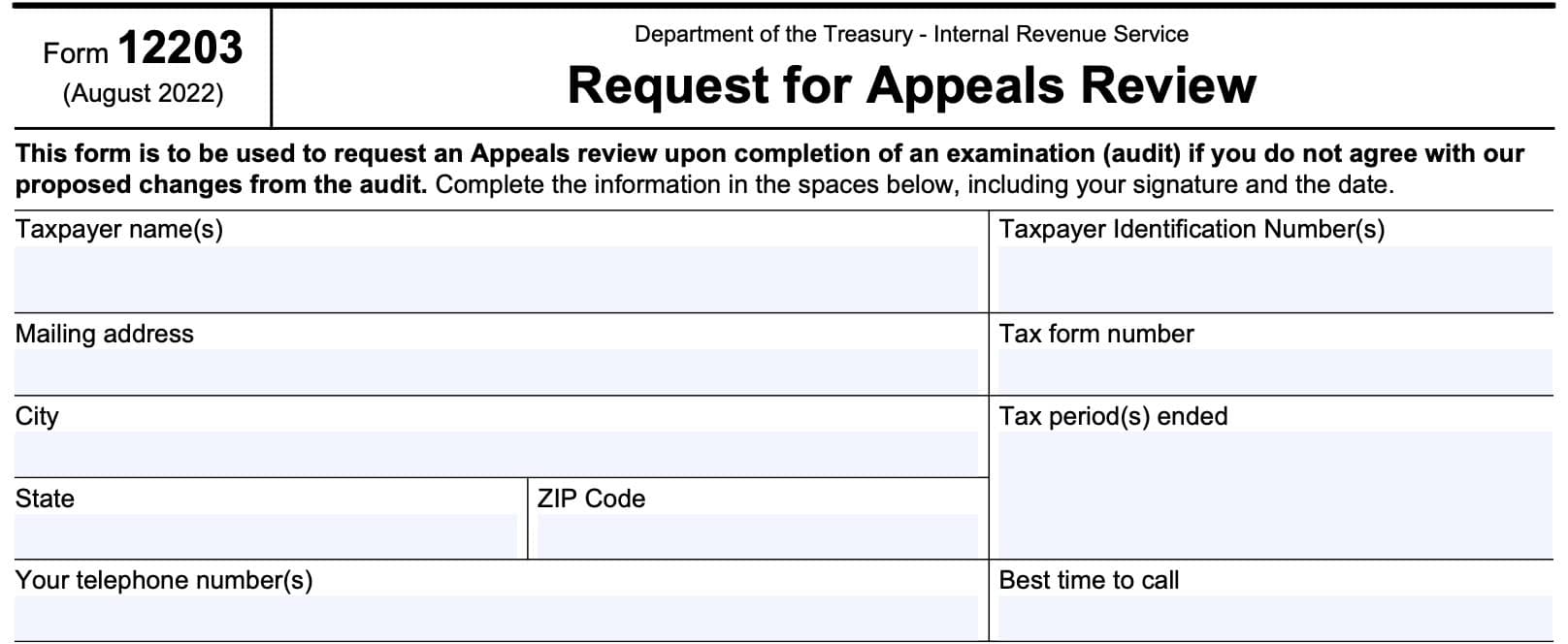

Taxpayer name(s)

Enter your name as it appears on your tax return or in your tax audit letter. For married couples filing a joint return, enter both spouses’ names.

Taxpayer Identification Number(s)

Enter your taxpayer identification number, as reported on your tax return or audit letter. This can be one of the following:

- Social Security number (SSN)

- Individual taxpayer identification number (ITIN)

- Employer identification number (EIN)

For a married couple, enter both tax ID numbers.

Mailing address

Enter your mailing address as it appears on your tax return. This should include the following information:

- Street name and address

- City, state, ZIP code

Telephone number

Enter your 10-digit phone number, beginning with your area code.

Tax form number

Enter the tax form number of the tax return in question. For example, if you’re making a small case request regarding your individual income tax return, enter ‘1040.’

Tax Period(s) Ended

Enter the ending date or dates for the tax period or periods for which you are requesting an appeal.

Best time to call

Enter the best time of day for the Internal Revenue Service to place a telephone call.

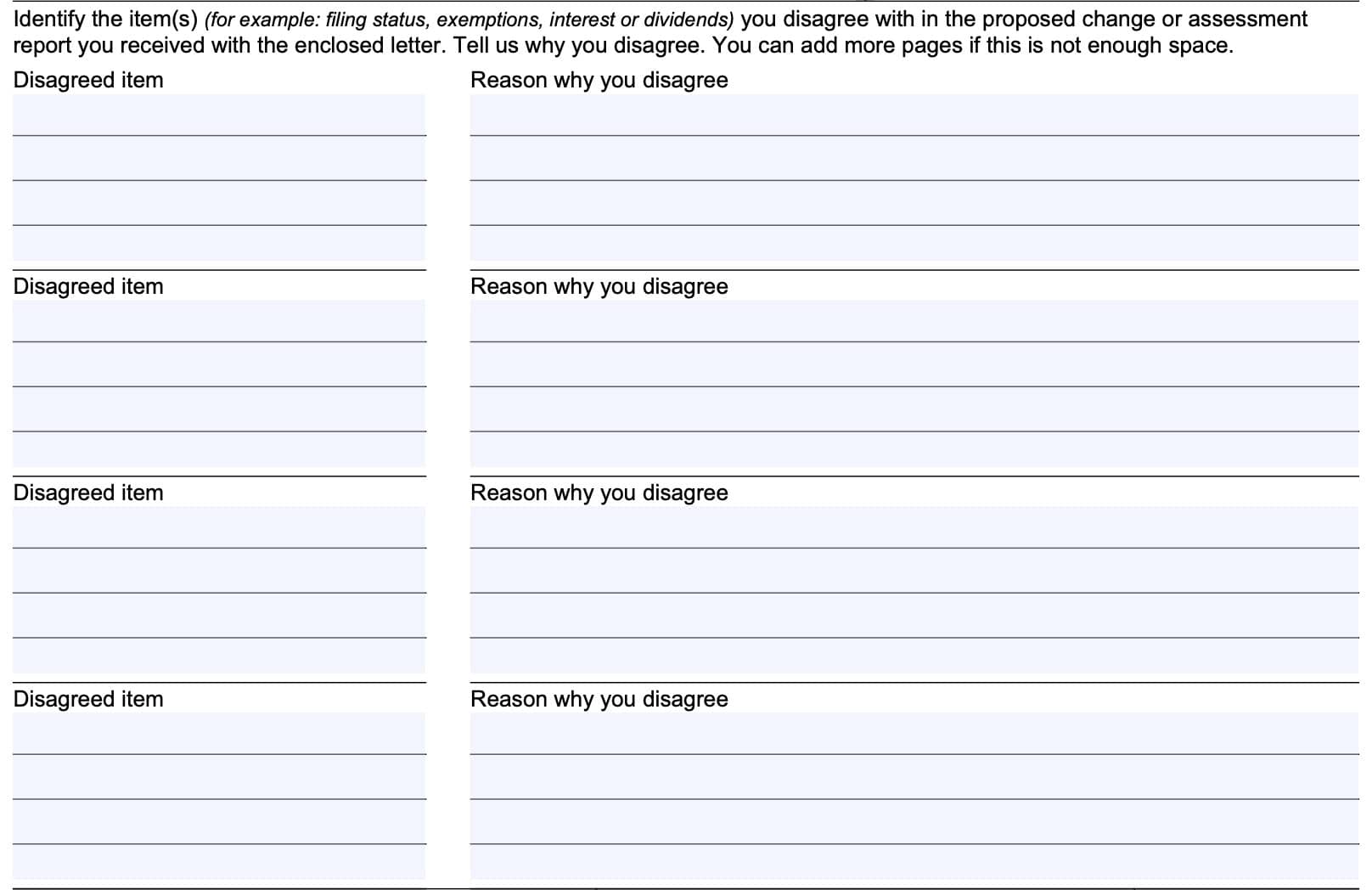

Disagreed items

In this section, you’ll enter the item(s) that you disagree with in the changes or assessments proposed by the revenue officer during your IRS examination. You may list up to 4 separate items, but you may attach more pages if you wish to include additional information.

For each item, you would enter the disagreed item, and as much specific information as you can include as to why you agree with the assessment.

Examples

The IRS website does not give any specific examples of how to list items of disagreement, or what type of information you should include here. The top of the form includes some of the following as examples:

- Filing status

- Exemptions

- Interest or dividend income

However, IRS Publication 5, Your Appeal Rights and How to Prepare a Protest if You Disagree, states that you should include the following under formal written protest procedures:

- A list of all disputed issues, tax periods or years involved, proposed changes, and reasons you disagree

- Facts supporting your position on each disputed issue

- Law or authority, if any, supporting your position on each disputed issue

Before you include a certain item, you should make sure that you have enough facts to support your position, and that the law or tax authority supports your position.

Examples of tax authority

Below are examples of tax authority:

- Legislative authority

- U.S. Constitution: Grants Congress the right to raise and assess taxes

- Internal Revenue Code: The Internal Revenue Code is the section of federal law that pertains to all aspects of tax authority.

- For example, Internal Revenue Code Section 6001 covers the taxpayer’s responsibility to maintain appropriate tax records for audit or examination purposes

- Considered to be legislative authority

- Administrative authority: Tax authority determined by the executive branch of the federal government. Administrative authority is determined in the following order:

- Treasury Regulations

- IRS Revenue Rulings

- IRS Revenue Procedures

- Private Letter Rulings

- General Counsel Memorandums

- Internal Revenue Manual

- Judicial authority: Taxpayers may appeal IRS decisions through the judicial review process by filing a tax court petition. Judicial authority over tax matters is recognized in the following order of ascension:

- United States Tax Court

- United States District Court

- U.S. Circuit Court of Appeals

- Supreme Court

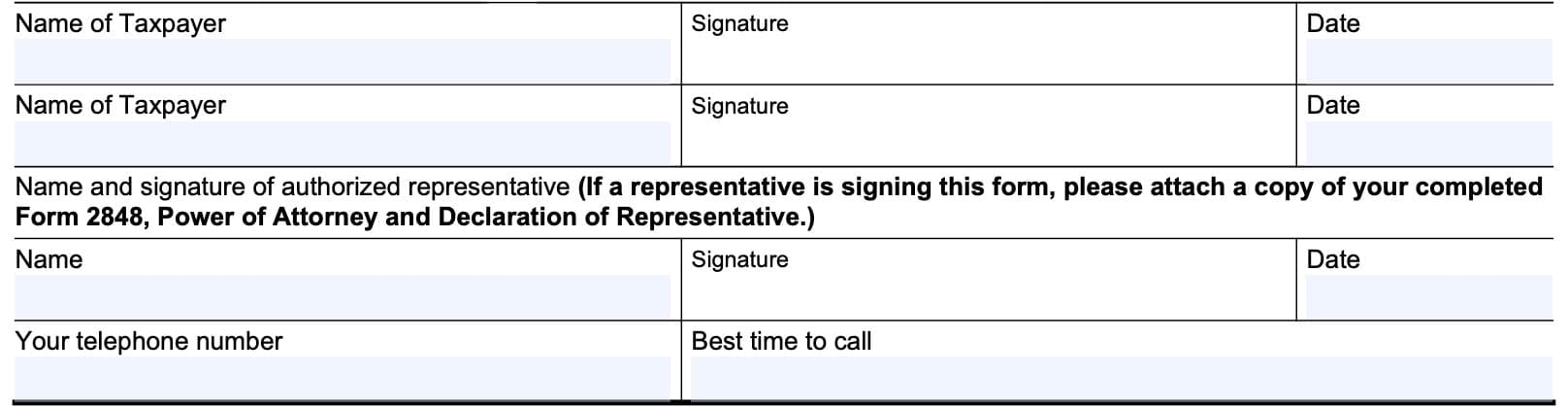

Signature

At the bottom of IRS Form 12203, enter your name, then sign and date in the spaces provided. If a married couple is requesting an administrative appeal, then both spouses should sign.

Appointing a representative

When requesting an appeals conference, it’s generally a good idea to appoint a representative who is familiar with the IRS tax appeal process. If you appoint a representative, you must complete and sign IRS Form 2848, Power of Attorney and Declaration of Representative, for the IRS to recognize his or her during the appeal.

Although the IRS will allow certain non-tax professionals to represent taxpayers before the IRS in administrative procedures, only a tax professional may represent you as part of the appeals process. The IRS represents the following as tax professionals:

- An attorney

- Does not have to be recognized as a tax attorney

- May represent clients before the IRS and in tax court

- A certified public accountant, or

- An enrolled agent authorized to practice before the IRS

Any tax professional must be in good standing with either the IRS or by their jurisdiction.

Filing considerations

Once you’ve completed this tax form, you aren’t done. In this section, we’ll cover some additional items, such as:

- How to file your Form 12203

- Situations when you should not file this form

- What you should know about small case procedures

Let’s start by going over how to file your completed form.

How to send your completed IRS Form 12203

You’ll need to file your completed form to the correct IRS address within the appropriate amount of time. Fortunately, you should already have this information.

When responding to an IRS letter, you’ll need to pay particular attention to several parts:

- Date of the letter: Generally, you have a limited period of time to file an appeal. This time limit starts as of the date of the IRS letter.

- Generally, the IRS website says that you have 30 days from the date of the letter. However, pay close attention in case the letter says otherwise.

- Address: According to the IRS website, once you’ve completed your protest, you can mail it to the IRS address on the letter that explains your appeal rights

If you have any doubt, contact the IRS as the phone number contained in your letter. According to IRS Publication 5181, Tax Return Reviews by Mail, you can also call the IRS at: 1-800-829-3676.

When the IRS will not accept IRS Form 12203

The IRS website allows a taxpayer to use IRS Form 12203 to make a small case request.

Small case requests

A small case request is one that:

- Is $25,000 or less

- Including tax, penalties and interest for each tax period in question

- Does not require a formal written protest

The IRS will accept IRS Form 12203 under small case request procedures. If a case does not qualify as a small case request, then you must submit a formal written protest.

When a formal written protest is required

The following situations cannot be appealed using IRS Form 12203, and a formal written protest is required:

- Employee plan and tax-exempt organization cases, regardless of dollar amount

- Partnerships and S corporation cases, regardless of dollar amount

- Any other cases that don’t qualify for small case request procedures, including appeals consideration for the following:

- Liens

- Levies

- Seizures

- Installment agreements

Appealing a collection decision

When it comes to the IRS collections process, there are several different ways you might dispute the collection decision to the IRS Independent Office of Appeals:

- Collection Appeals Program (CAP)

- Collection Due Process (CDP)

- Offer in Compromise (OIC)

- Trust Fund Recovery Program (TFRP)

There is also a different tax form for each type of collection dispute. Let’s take a closer look at each.

Collection Appeals Program

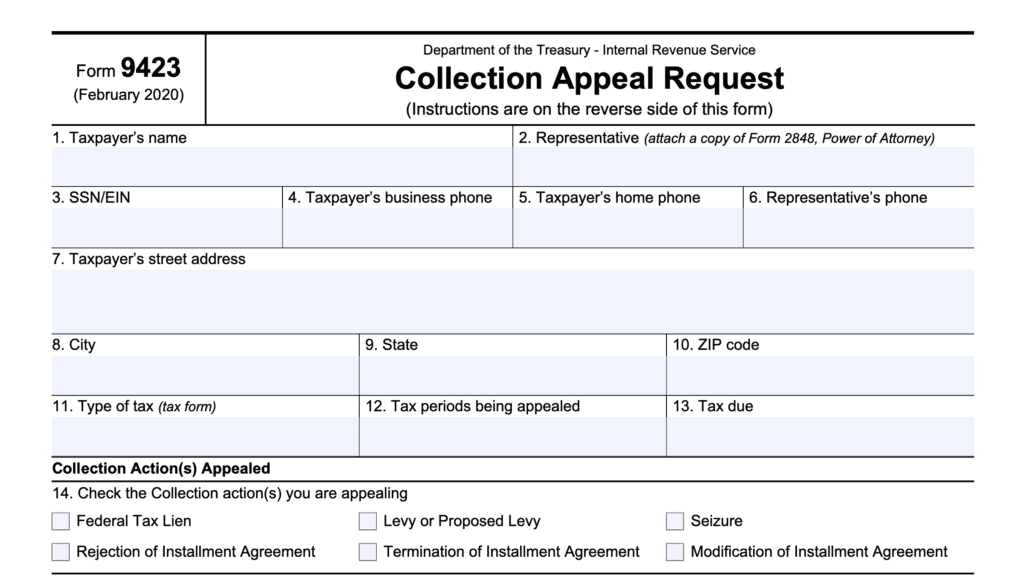

The Collection Appeals Program is available for a broad range of collection actions, such as:

- Notice of Federal Tax Lien, filed or proposed to be filed

- Levy action, taken or proposed

- Rejection, termination, or modification of Installment Agreement

- Disallowance of taxpayer request to return to levied property

- Seizure

CAP cases are regarding a specific collection action proposed or taken, and are generally resolved very quickly. However, you can’t go to court if you disagree with the Appeals decision at the CAP hearing.

You can make your collection appeals program request by filing IRS Form 9423, Collection Appeals Request.

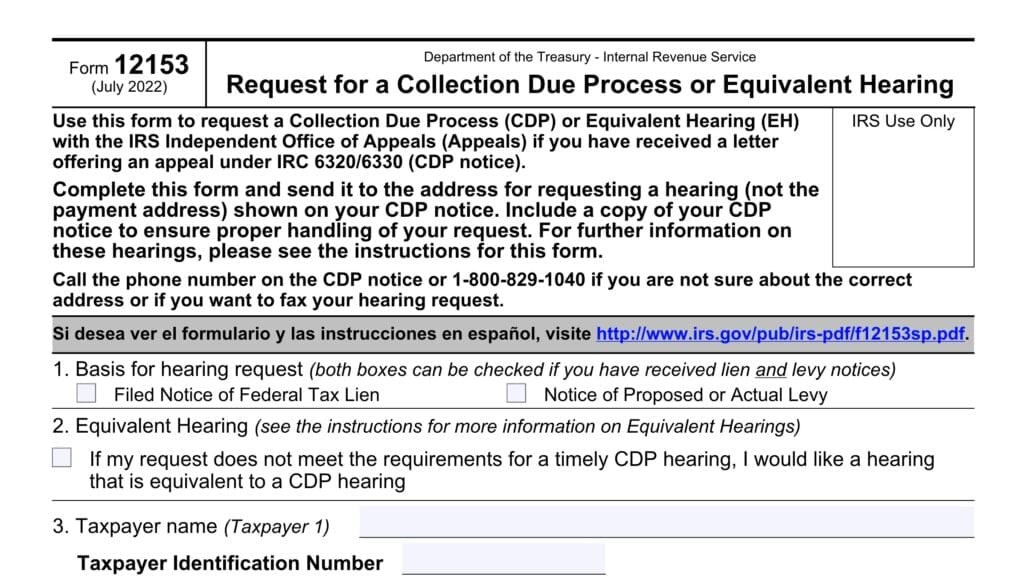

Collection Due Process

You are entitled to a Collection Due Process (CDP) hearing with the IRS Appeals Office if the IRS sends you a notice that states you have the right to request a CDP hearing, such as:

- Notice of Federal Tax Lien Filing and Your Right to a Hearing Under IRC 6320

- Final Notice – Notice of Intent to Levy and Notice of Your Right to A Hearing

- Notice of Jeopardy Levy and Right of Appeal

- Notice of Levy on Your State Tax Refund – Notice of Your Right to a Hearing

- Post Levy Collection Due Process (CDP) Notice

Unlike the collection appeals program, you can appeal the outcome of a CDP hearing in tax court.

You may request your CDP hearing by filing IRS Form 12153, Request for a Collection Due Process or Equivalent Hearing, within 30 days of the date of the letter or notice.

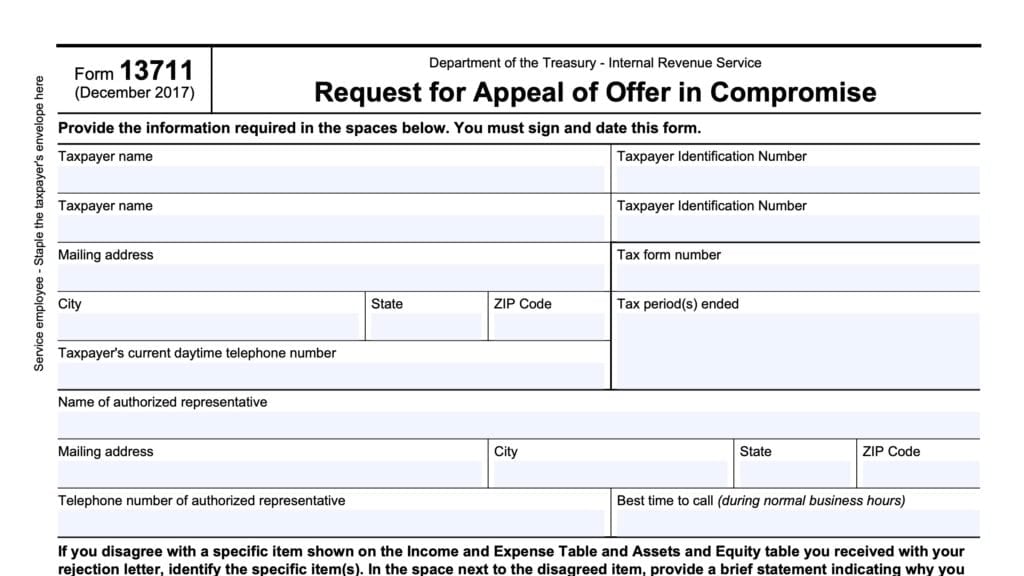

Offer in Compromise

An Offer in Compromise (OIC) is an agreement between the taxpayer and the government that settles a tax liability for payment of less than the full amount owed.

If you received a letter notifying you that your offer was rejected, you have 30 days from the date on the letter to request an appeal of the decision by filing IRS Form 13711, Request for Appeal of Offer in Compromise.

Video walkthrough

Frequently asked questions

IRS Form 12203, Request for Appeals Review, is the tax form used by a taxpayer to appeal the IRS’ decision regarding a tax issue during the audit process. Taxpayers may use IRS Form 12203 to request a review for qualifying cases valued at less than $25,000.

To request an appeal review, send your completed request to the IRS address indicated in your most recent IRS letter or notice. If you no longer have the IRS notice, contact the IRS at their toll free number: 1-800-829-3676 for further guidance.

Where can I find IRS Form 12203?

You can find the latest versions of IRS forms on the IRS website. For your convenience, we’ve attached the latest version of IRS Form 12203 (English and Spanish version) in this article.