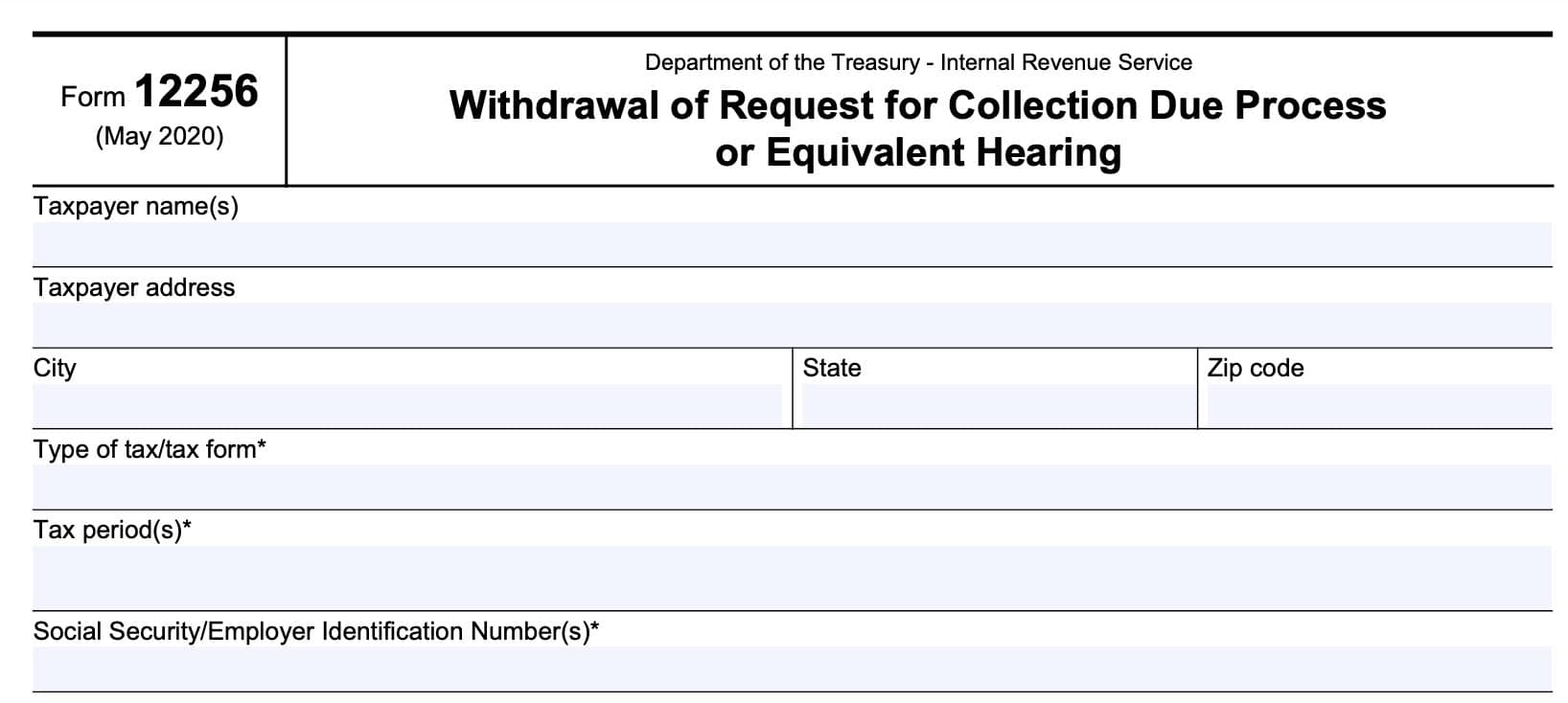

IRS Form 12256 Instructions

If you’ve requested a collection due process or equivalent hearing with the IRS, you have the right to have your case reviewed by the IRS Independent Office of Appeals. However, if you’ve reached a satisfactory agreement with your revenue officer, you may want to withdraw your request by filing IRS Form 12256, Withdrawal of Request for Collection Due Process or Equivalent Hearing.

In this article, we’ll walk you through everything you need to know about IRS Form 12256, including:

- Step by step instructions on completing the form

- Taxpayer rights you may be giving up by filing

- Frequently asked questions

Let’s begin with a top-down overview of IRS Form 12256.

Table of contents

How do I complete IRS Form 12256?

This one-page tax form is relatively straightforward. For your convenience, we’ve broken this form into four parts:

- Taxpayer information

- Tax authorities

- Taxpayer rights that you’re giving up

- Signature

Let’s take a closer look at each section of IRS Form 12256 in more depth, beginning with the information fields at the top of the form.

Taxpayer information

At the top of the form, you’ll need to enter information about yourself and your tax situation. Let’s go through each line, step by step.

Taxpayer name

Enter your name in this field. Married couples filing a joint tax return should enter both names here.

Taxpayer address

Enter your address here. Include the following information:

- Street number and street name

- City

- State

- Zip code

Change of address

If you’ve recently moved, you should consider updating your IRS records with your new address. This will help you stay on top of additional IRS correspondence.

You can change your address in several ways:

- Filing your income tax return

- Calling the IRS

- Individual taxpayers: (800) 829-1040

- Business owners: (800) 829-4933

- Filing a change of address form

- Individuals file IRS Form 8822, Change of Address

- Business owners file IRS Form 8822-B, Change of Address or Responsible Party – Business

Type of tax or type of tax form

Enter the type of tax form or tax return that you’ve requested a collection due process (CDP) or equivalent hearing for.

Tax Period(s)

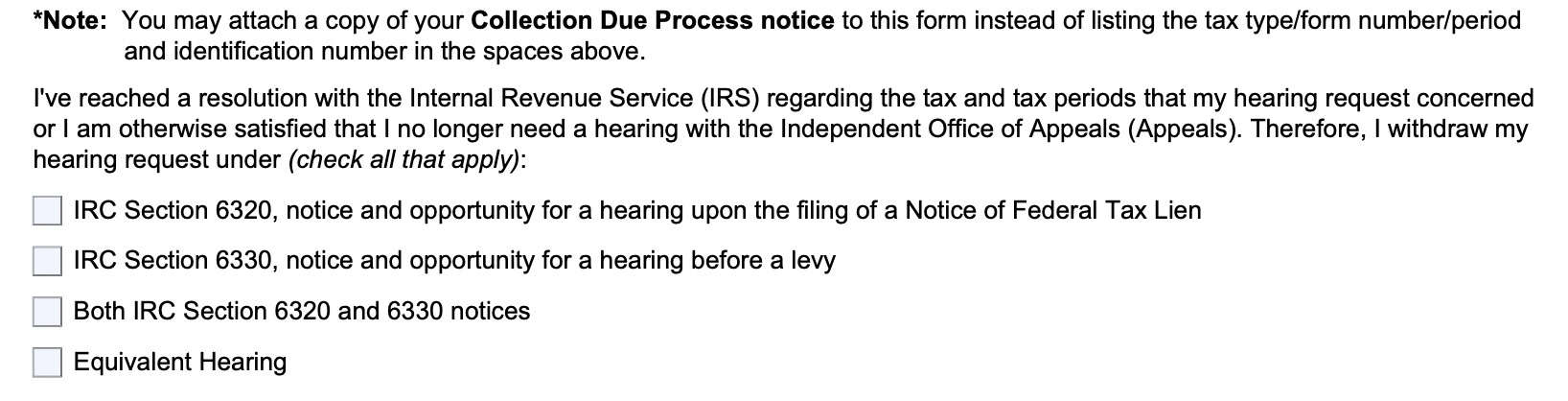

Note: For the following fields, you do not have to enter your tax type, form number, time period, or identification number. Instead, you can attach a copy of your CDP notice to IRS Form 12256.

If you do not have your CDP notice, or if you do not wish to include it, then enter the tax period or periods for which you requested the CDP or equivalent hearing. This can be in tax years for annual returns or in tax quarters for quarterly returns.

Social Security number or employer identification number

Individual taxpayers should enter their complete Social Security number (SSN) in this field. Married taxpayers filing jointly should enter the SSN for both spouses.

Business owners should enter their employer identification number, or EIN in this field.

Tax authorities

In this section, you’re acknowledging the following:

- You’ve reached a resolution with the IRS about the tax issue that your CDP hearing request was supposed to reach, or

- You’ve decided that you no longer need a hearing with the IRS’ Independent Office of Appeals.

In either situation, you’ll need to check the box or boxes that apply to you. Let’s take a closer look at each of the following:

- IRC Section 6320, Notice and Opportunity for a Hearing Upon the Filing of a Notice of Federal Tax Lien

- IRC Section 6330, Notice and Opportunity for a Hearing Before a Levy

- Equivalent Hearing

IRC Section 6320

IRC 6320 allows a taxpayer to request an appeal based upon a Notice of Federal Tax Lien filing, or an NFTL filing.

A tax lien is the federal government’s legal claim against your property when you neglect or fail to pay a tax debt. The lien protects the government’s interest in all your property, including real estate, personal property and financial assets.

Contrary to popular belief, a tax lien does not ‘take’ your property. Instead, a tax lien simply indicates to creditors, financial institutions, or other taxpayers that the IRS has an interest in that piece of property.

Tax lien example

When I was a financial planner, my first significant client case came as a result of a tax lien.

In this case, the client owed over $100,000 in tax debt. As a result, the IRS placed a lien on the client’s house. Once the client paid down the tax debt, through an installment agreement plan, the IRS released the lien.

At no point was the client in actual danger of losing their house as a result of a tax lien. That doesn’t happen until the IRS issues a notice of intent to levy.

While a tax lien doesn’t seize property, there might be other adverse impacts that impact a taxpayer, such as a reduced credit score, frozen assets, or inability to obtain financing. However, there might be ways that a taxpayer resolves a tax lien without resorting to appeals, and before they’ve paid off their entire tax debt.

Ways that taxpayers may be able to resolve their tax lien without paying it off

There are three primary ways that a taxpayer may have to resolve issues surrounding their tax lien without paying it off:

- Tax lien subordination

- Tax lien withdrawal

- Tax lien discharge

Let’s take a closer look at each.

Tax lien subordination

Tax lien subordination does not remove the lien, but allows other creditors to move ahead of the IRS, which may make it easier to get a loan or mortgage.

To request a subordination of your tax lien, you may file IRS Form 14134, Application for Certificate of Subordination of Federal Tax Lien.

Tax lien withdrawal

A tax lien withdrawal removes the public Notice of Federal Tax Lien and assures that the IRS is not competing with other creditors for your property. However, you are still liable for the amount due.

To request a tax lien withdrawal, file IRS Form 12277, Application for Withdrawal of Filed Form 668(Y), Notice of Federal Tax Lien.

Tax lien discharge

A tax lien discharge removes the lien from a specific piece of property. If the IRS has multiple tax liens in place, a taxpayer may request a tax lien discharge from a piece of property, while the IRS maintains the other tax liens in place.

To request a tax lien discharge, you can file IRS Form 14135, Application for Certificate of Discharge from Federal Tax Lien.

IRC Section 6330

IRC Section 6330 allows a taxpayer to request an appointment with an appeals officer before the IRS takes levy action.

What is a tax levy?

Unlike a tax lien, where the IRS simply secures an interest in a taxpayer’s property, a tax levy allows the IRS to actually seize a taxpayer’s property to pay off tax debts.

If you’ve reached a resolution with the IRS that allows you to minimize property seizure, then you can file your withdrawal of request under IRC 6330.

Equivalent hearing

An equivalent hearing is similar to the collection due process hearing. However, there are two significant differences:

- The equivalent hearing may not prohibit levy actions or suspend the 10-year period for collecting taxes

- A taxpayer cannot go to tax court to contest a decision issued by the IRS Office of Appeals

Generally, if you request a collection due process hearing on IRS Form 12153, but do not meet the time frame for a timely CDP hearing request, the IRS will grant an equivalent hearing.

Generally, you must make a timely request for an equivalent hearing. Timely requests are made within the following time frame:

- Lien Notice: One year plus five business days from the filing date of the Federal Tax Lien.

- Levy Notice: One year from the date of the CDP levy notice.

Let’s move on to understand taxpayer rights you may be giving up.

Taxpayer rights that you’re giving up

By withdrawing your CDP request or your request for an equivalent hearing, you are giving up certain taxpayer rights. Let’s take a closer look at each.

Withdrawing a request for CDP hearing

Below is a little more background on each of the specific taxpayer rights that you give up by filing IRS Form 12256.

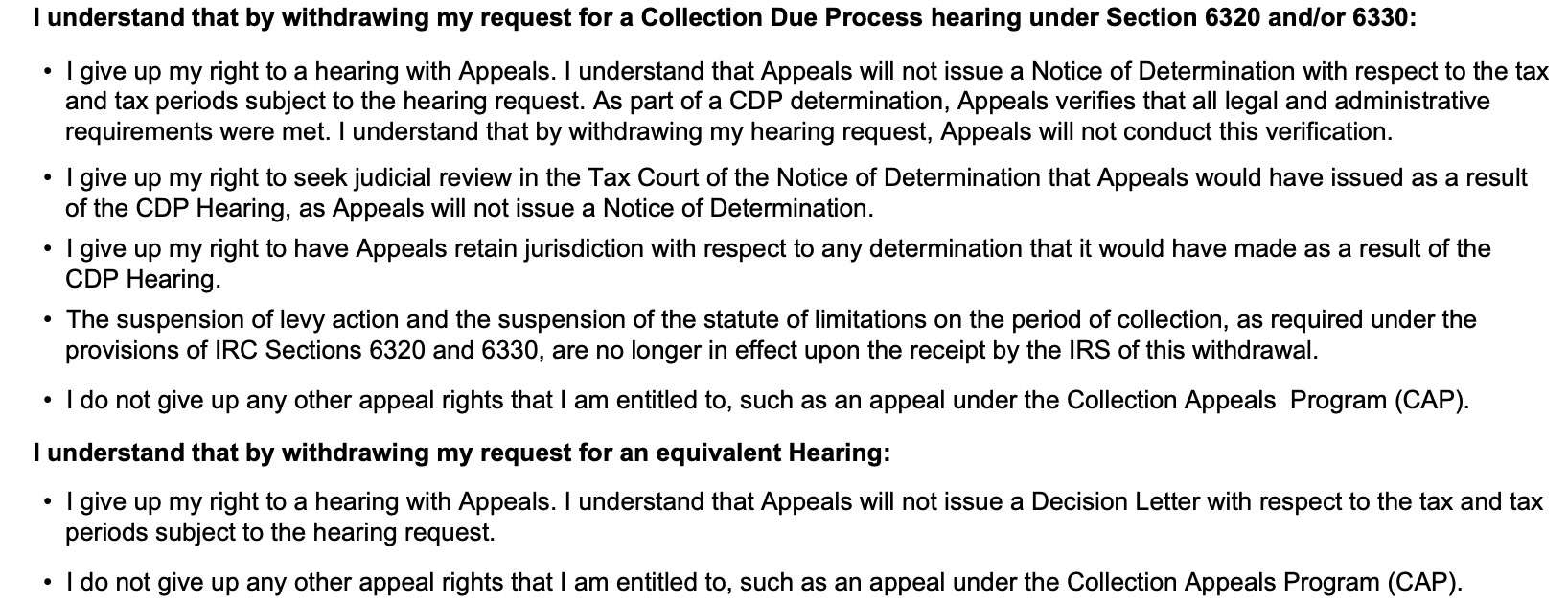

I give up my right to a hearing with Appeals

I understand that Appeals will not issue a Notice of Determination with respect to the tax and tax periods subject to the hearing request. As part of a CDP determination, Appeals verifies that all legal and administrative requirements were met. I understand that by withdrawing my hearing request, Appeals will not conduct this verification.

In other words: The IRS Office of Appeals is an independent part of the Internal Revenue Service, whose mission statement is:

“To resolve disputes, without litigation, in a way that is fair and impartial to the government and to you.”

By filing this form, you may not know whether the appeals officer or settlement officer would have found something wrong with the collection action or actions being taken.

I give up my right to seek judicial review in tax court

I give up my right to seek judicial review in the Tax Court of the Notice of Determination that Appeals would have issued as a result of the CDP Hearing, as Appeals will not issue a Notice of Determination.

In other words: Under normal circumstances, if you do not agree with the decision reached by the appeals officer, you can submit your case to a federal court, such as Tax Court, for judicial review.

When you file IRS Form 12256, you give up this right and accept the IRS’ position.

I give up my right to have Appeals retain jurisdiction

I give up my right to have Appeals retain jurisdiction with respect to any determination that it would have made as a result of the CDP Hearing.

In other words: Since the Appeals Office is not involved, they do not have jurisdiction over your tax case. You accept the binding decision from the revenue officer in charge of your case.

Suspension of levy action and statute of limitations on the period of collection are no longer in effect

The suspension of levy action and the suspension of the statute of limitations on the period of collection, as required under the provisions of IRC Sections 6320 and 6330, are no longer in effect upon the receipt by the IRS of this withdrawal.

In other words: As part of the collections process, the IRS must give the taxpayer a certain period of time to file an appeal, usually a 30-day period. During this time, the IRS cannot seize property, and the statute of limitations on the collection period is suspended. If you waive your rights to an appeal, these suspensions no longer apply.

I do not give up any other appeal rights

I do not give up any other appeal rights that I am entitled to, such as an appeal under the Collection Appeals Program (CAP).

In other words: You do not give up all taxpayer rights by filing IRS Form 12256. To learn more about the rights you may still have, you can check out the IRS’ Taxpayer Bill of Rights.

Withdrawing an equivalent hearing request

When requesting an equivalent hearing, you’ve already given up some rights afforded under the CDP process. But there are still rights that you maintain, until you file IRS Form 12256.

I give up my right to a hearing with Appeals

I understand that Appeals will not issue a Notice of Determination with respect to the tax and tax periods subject to the hearing request. As part of a CDP determination, Appeals verifies that all legal and administrative requirements were met. I understand that by withdrawing my hearing request, Appeals will not conduct this verification.

In other words: The IRS Office of Appeals is an independent part of the Internal Revenue Service, whose mission statement is:

“To resolve disputes, without litigation, in a way that is fair and impartial to the government and to you.”

By filing this form, you may not know whether the appeals officer or settlement officer would have found something wrong with the enforcement action or actions being taken.

I do not give up any other appeal rights

I do not give up any other appeal rights that I am entitled to, such as an appeal under the Collection Appeals Program (CAP).

In other words: You do not give up all taxpayer rights by filing IRS Form 12256. To learn more about the rights you may still have, you can check out the IRS’ Taxpayer Bill of Rights.

Let’s proceed to the signature section.

Signature

Sign and date the form at the bottom. If you are married, your spouse must also sign and date.

If you’ve authorized a representative by filing IRS Form 2848, Power of Attorney and Declaration of Representative, then that person may sign on your behalf.

Video walkthrough

Watch this instructional video to learn more about withdrawing your collection due process hearing by filing IRS Form 12256.

Frequently asked questions

IRS Form 12256 is the tax form that taxpayers may file when they wish to withdraw an outstanding request for a case file review through the IRS Independent Office of Appeals. This may be done because the IRS and taxpayer have already reached a satisfactory conclusion to the tax case.

You may still be able to request assistance from the IRS Taxpayer Advocate Service (TAS), Low-Income Tax Clinic (LITC), or from your revenue officer. However, once you withdraw your appeals request, you won’t have access to the appeals process, which include legal options outside the IRS.

Where can I find IRS Form 12256?

You can find the latest versions of IRS forms on the Internal Revenue Service website. For your convenience, we’ve included the most recent copy of IRS Form 12256 here, in this article.