IRS Form 12277 Instructions

If you’ve received a notice of federal tax lien (NFTL), the IRS generally expects you to satisfy your outstanding tax debt before releasing the lien. However, you might be able to obtain a lien withdrawal by filing IRS Form 12277, Application for Withdrawal of Filed Form 668(Y), Notice of Federal Tax Lien.

This article will walk you through everything you need to know about IRS Form 12277, including:

- How to use Form 12277 to request a lien withdrawal

- Why you should attempt to get rid of a tax lien, if possible

- How to get rid of a tax lien, even if you cannot fully pay your tax bill

Let’s start with step by step guidance on how to complete Form 12277.

Table of contents

How do I complete IRS Form 12277?

We’ll walk through this one-page tax form, step by step.

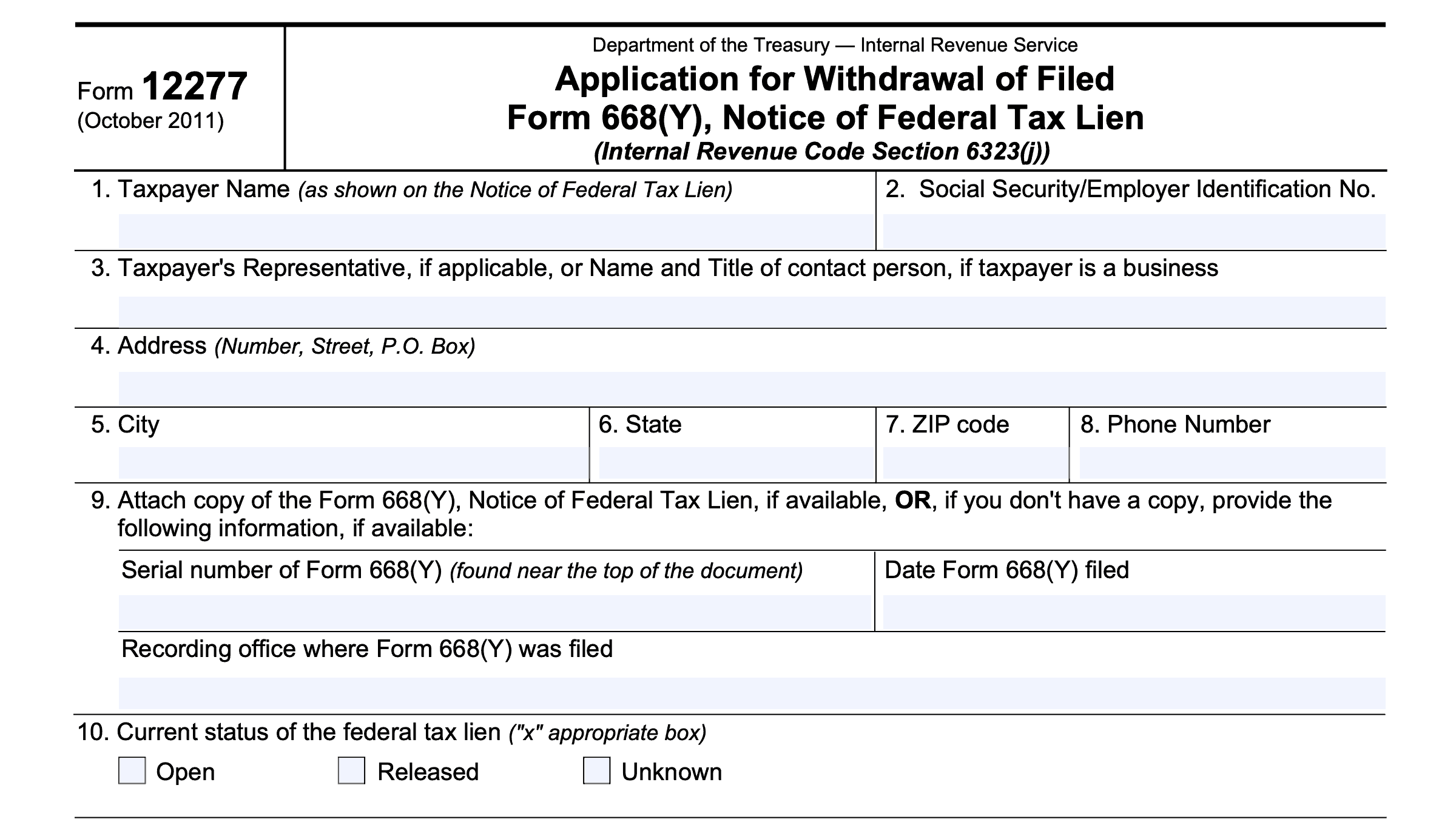

Line 1: Taxpayer name

Enter your name as shown on the notice of federal tax lien (NFTL).

Line 2: Taxpayer Identification Number

This must match either the Social Security number (SSN) or Employer identification number (EIN) as shown on the original NFTL.

Line 3: Taxpayer’s representative, if applicable

If you’ve hired a tax professional or an experienced tax attorney to help you file this form, then enter that person’s name in Line 3.

For business owners, enter the name and title of a contact person for your business.

If you do not have an outside representative, leave blank.

Line 4: Address

Enter either the taxpayer’s address or the address of your designated representative named in Line 3.

Line 5: City

Enter the applicable city.

Line 6: State

Enter the applicable state.

Line 7: ZIP Code

Enter the zip code.

Line 8: Phone number

Enter a contact phone number.

Line 9: Tax Lien information

If possible, attach a copy of the original NFTL to this form. If you do not have a copy, provide the following information:

- Tax lien serial number (near the top of the document)

- Date tax lien was filed

- Recording office where the tax lien was filed

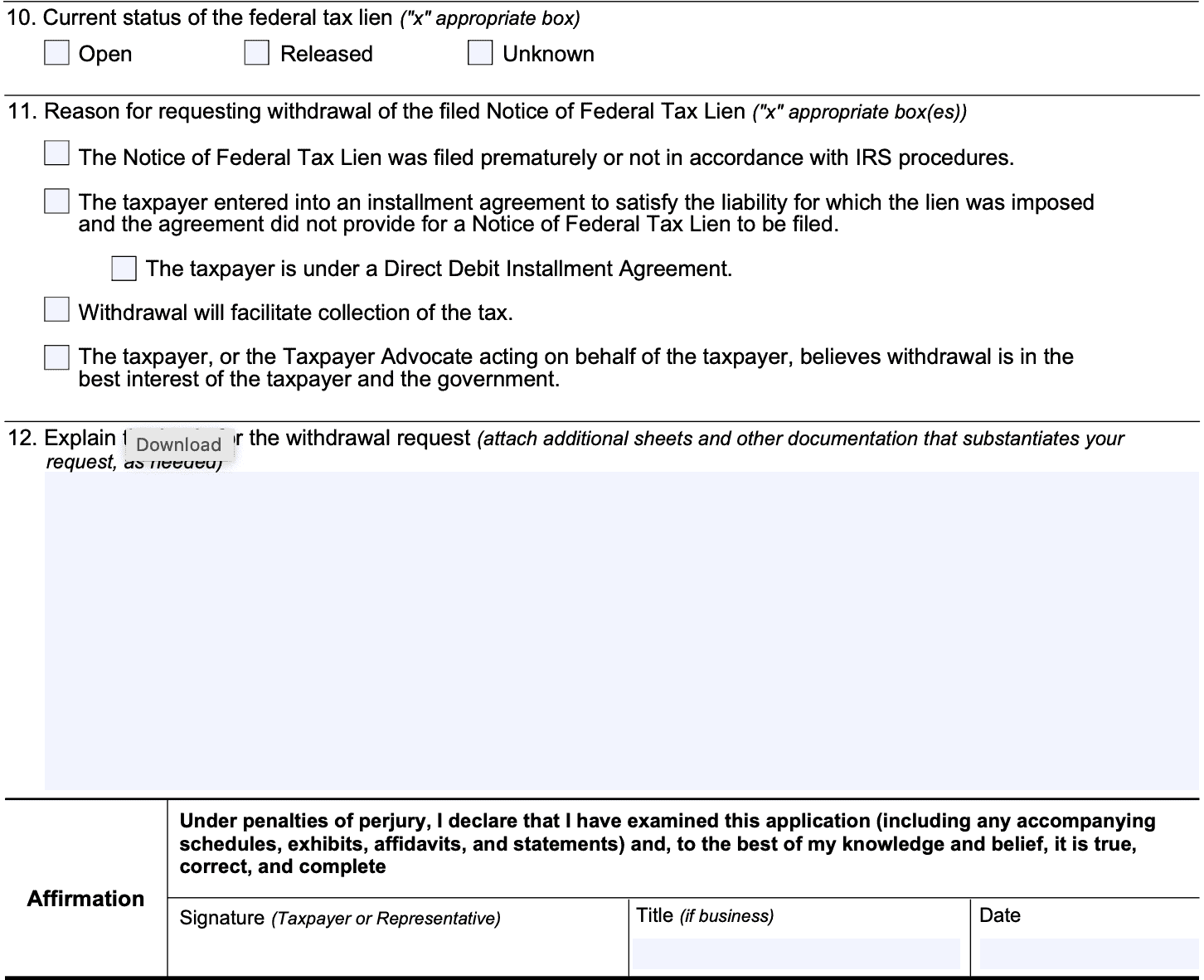

Line 10: Current status of the tax lien

Check the appropriate box:

- Open: There is an outstanding balance regarding the tax liabilities listed on the tax lien.

- Released: The tax lien has been satisfied, or is no longer enforceable.

- Unknown: Unknown means you do not know the tax lien’s current status.

Line 11

Check the appropriate box.

If you’ve recently entered into an installment agreement, you probably should ensure that the agreement either:

- Meets the IRS criteria listed above

- Did not contain a provision for a notice of the lien to be filed in the first place

If you are requesting a withdrawal of a released NFTL, you generally should check the last box regarding the best interest provision.

Line 12: Explanation

In this section, provide a detailed explanation of the events or the situation to justify the withdrawal request. Attach additional sheets and supporting documentation, if necessary.

Video walkthrough

Watch this instructional video for more guidance on completing Form 12277 to request a withdrawal of a notice of federal tax lien..

Why should I get rid of a tax lien?

There are several reasons why you should want to get rid of a tax lien.

There’s a direct impact to your credit score

A federal tax lien, just like other liens, directly impacts your credit score. The odds are high that with a tax lien in place, you will have a much more difficult job obtaining financing.

This is true even for mortgage refinancing because tax liens usually subordinate other lien holders. In other words, the IRS reserves first right to collect should anything happen to you. So mortgage-holders looking to refinance may find difficulty doing so with the tax lien in place.

Even if the new mortgage frees up money for them to pay down the tax debt!

The IRS doesn’t always release the tax lien in a timely manner

The IRS website states that the IRS releases tax liens within 30 days after the outstanding tax liability is satisfied.

If you wait 30-45 days after your last payment, you should check your credit report. Odds are the lien might still be on there. If so, you should probably file for a lien withdrawal.

You have an installment plan in place

If you’ve entered into a IRS payment plan that meets certain requirements, IRS procedures allow for the lien withdrawal, even if you still have an outstanding balance.

Why leave a tax lien in place if you’re making tax payments?

How do I get rid of an IRS tax lien?

According to the Internal Revenue Service, the best way to completely rid yourself of a federal tax lien is to completely pay off your outstanding tax debt. The IRS website states that an IRS lien release occurs within 30 days of full payment of all federal taxes, plus any tax penalties and interest.

However, the IRS recognizes certain instances where it might be in the best interest of the taxpayer and the IRS to reduce the impact of a tax lien if a federal lien release is not feasible. There are three alternative options that the IRS offers, provided that they serve the best interests of both the government and the taxpayer:

Let’s take a closer look at each situation.

Discharge of property

A lien discharge does not absolve the taxpayer of the unpaid taxes they still owe. However, it removes the government’s legal claim to the taxpayer’s property from the property itself.

When Can I obtain a discharge of property from a tax lien?

Internal Revenue Code Section 6325(b) authorizes the discharge of property secured by a federal tax lien under one of the following circumstances:

- Fair market value of the property secured by the lien is at least twice the amount of the lien and all other debts associated with the property

- Most applicable to real property in a rising real estate market

- Lien has been partially satisfied, and/or the federal government determines that their interest in the property has no value

- The property is sold and the available funds are held in a separate account that the U.S. government has the same priority over the funds as with the property

- Taxpayer either:

- Makes a payment equivalent to the amount secured by the lien

- Furnishes a bond acceptable to the federal government for the amount secured by the lien

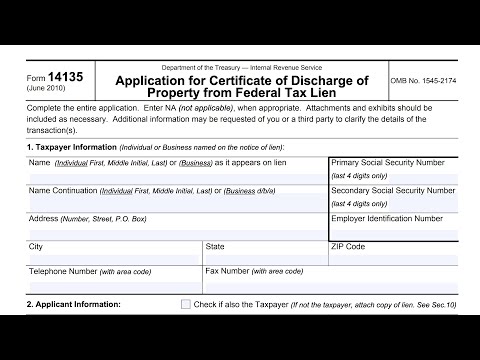

A lien discharge might be a good idea for taxpayers with a lien on real estate that they are trying to sell or refinance. Taxpayers may file IRS Form 14135, Application for Certificate of Discharge of Property from Federal Tax Lien, to request that the IRS discharge specific property secured by a federal tax lien.

Subordination of tax lien

Federal law also allows the IRS to subordinate their tax lien so that another creditor may move ahead of the IRS in position. This may be particularly helpful for taxpayers who are looking to refinance their mortgage, but have been consistently paying their taxes.

IRC Section 6325(d) states that the federal government may subordinate a federal tax lien under one of the following circumstances:

- The taxpayer has made an additional payment equal to the amount of the lien or interest to which the certificate subordinates the lien of the United States

- The federal government believes that subordinating the tax lien will help the taxpayer continue to pay down their tax liability

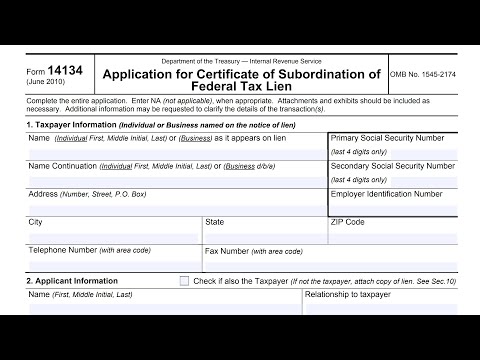

Taxpayers may file IRS Form 14134, Application for Certificate of Subordination of Federal Tax Lien, to request that the IRS subordinate the tax lien to another creditor’s debt.

Withdrawal of tax lien

The final option involves a withdrawal of the federal tax lien. IRC Section 6323(j) states that the federal government may withdraw notice of a federal tax lien under one or more of the following circumstances:

- The IRS or the Treasury Secretary determines that the lien notice was premature or otherwise not filed according to established procedures

- The taxpayer has entered into a direct debit installment agreement with the IRS

- Withdrawal of the lien notice will actually facilitate collection of the tax, or

- With the consent of the Taxpayer Advocate or at the Taxpayer Advocate’s recommendation that a tax lien withdrawal would be in the federal government’s best interest

We should note the additional requirements that the IRS has placed on tax lien withdrawal. Specifically regarding a taxpayer’s payment agreement.

When does a taxpayer’s installment agreement meet the criterial for tax lien withdrawal?

As a result of the IRS Fresh Start Program, a taxpayer may apply for tax lien withdrawal, even if they have not completely paid their tax liability.

However, they must meet the following requirements:

- Taxpayer must be qualified

- Individuals

- Businesses with income tax liability only

- Out of business entities with any type of tax debt

- Taxpayer owes $25,000 or less

- If the outstanding balance exceeds $25,000, a taxpayer may pay down the balance to $25,000 prior to requesting withdrawal of the Notice of Federal Tax Lien

- The Direct Debit Installment Agreement must full pay the amount you owe within the earlier of:

- 60 months, or

- Before the Collection Statute expires

- Taxpayer is in full compliance with other filing and payment requirements

- Taxpayer has made three consecutive direct debit payments

- Taxpayer has never defaulted on either the current or any previous Direct Debit Installment agreement

How do I file IRS Form 12277?

Do not file this tax form with your income tax return.

Instead, mail your application to the IRS office assigned to your account. This should be on your NFTL, or you can call the IRS to find out.

If the account is not assigned, or you’re not sure where it is assigned, you should mail the completed form and supporting documents to:

Internal Revenue Service, ATTN: Advisory Group Manager, in the state or area where you live. IRS Publication 4235, Advisory Group Addresses, contains a list of offices by state.

What happens if the IRS does not approve IRS Form 12277?

If the IRS does not approve your request, you may appeal the decision to the IRS’ Independent Office of Appeals in a couple of ways. The two primary ways are to:

- Request an appeal through the collection appeals program (CAP)

- Request a collection due process or equivalent hearing

We’ll take a closer look at each of these, as well as how you can obtain representation.

Collection due process or equivalent hearing

By law, you have the right to a CDP hearing when you receive a Notice advising you of this right and you timely postmark a request for a hearing to the address indicated on the Notice.

For a lien notice, the IRS is required to notify you the first time a Notice of Federal Tax Lien is filed for each tax and period, within 5 business days after the lien filing. This notice may be mailed, given to you, or left at your home or office.

You then have 30 days, after that 5-day period, to request a hearing with Appeals. The lien notice you receive will indicate the date this 30-day period expires.

You are limited to one hearing for each tax assessment within a tax period under the following statutes:

- IRC Section 6320: Notice and Opportunity for Hearing Upon Filing of Notice of Lien

- IRC Section 6330: Notice and Opportunity for Hearing Before Levy

You may contest the CDP determination in the United States Tax Court.

File IRS Form 12153 to request a collection due process or equivalent hearing.

Collection appeals program

The Collection Appeals Program, or CAP procedure, is available under more circumstances than a collection due process, or CDP hearing. Also, the CAP procedure usually results in a quicker decision.

You may appeal the proposed filing of a Notice of Federal Tax Lien (NFTL) or the actual filing of an NFTL at the first and each subsequent filing of the NFTL. You may also appeal the following denials:

- Requests to withdraw a NFTL

- Discharges, subordinations, or non-attachments of a lien

However, there are a couple of limitations under the CAP procedure that you should know before requesting this type of appeal:

- You may not challenge the existence or amount of your tax liability

- You cannot challenge the Appeals decision in court

You can request CAP procedure by filing IRS Form 9423, Collection Appeal Request. Learn more about filing IRS Form 9423 in this video.

IRS Representation

As a taxpayer, you can always represent yourself in IRS proceedings. However, you may also have someone else, such as a tax professional, immediate family member, or a business associate (for business returns), represent you.

Appointing a representative

To appoint an IRS representative, you must file IRS Form 2848, Power of Attorney and Declaration of Representative. This power of attorney form allows your representative to receive information directly from the IRS. Your representative can also represent your interests during the appeals process, including during a CAP procedure or CDP hearing.

If you wish to have a third-party receive tax information related to your situation, but you do not wish for the person to represent you in front of the IRS, then you may complete IRS Form 8821, Tax Information Authorization, instead. This form does not delegate representation powers in front of the IRS.

Neither IRS form allow a tax professional to represent you in a court of law, even the U.S. Tax Court. Tax court procedures are legal in nature, and specifically require legal representation that enrolled agents and CPAs cannot provide.

Low income tax clinics

A Low Income Taxpayer Clinic (LITC) may represent you if you qualify. LITCs are independent from the IRS and most provide representation before the IRS or in court on audits, tax collection disputes, and other issues for free or for a small fee.

Some clinics can provide multilingual information about taxpayer rights and responsibilities. IRS Publication 4134, Low Income Taxpayer Clinic List, provides information on clinics in your area.

Frequently asked questions

IRS Form 12277, Application for Withdrawal of Filed Form 668(Y), Notice of Federal Tax Lien, is the tax form that a taxpayer may use when pursuing a withdrawn lien is the best course of action.

Under the IRS’ Fresh Start initiative, a taxpayer may apply for a lien withdrawal if their tax liability has been paid in full, or if they meet certain criteria demonstrating their intent and ability to consistently pay down their debt pursuant to an IRS installment agreement.

The withdrawal of a federal tax lien means that the federal government no longer has a tax lien on your property. While this might be preferable to subordinating a lien or removing a lien from only one property item, it might not be feasible in every situation.

Where can I find IRS Form 12277?

You may find a copy of Form 12277 on the IRS website or by selecting the file below.