IRS Form 13711 Instructions

If you’ve submitted an IRS offer in compromise and the IRS rejects it, then you may be able to appeal the decision by filing IRS Form 13711, Request for Appeal of Offer in Compromise.

In this article, we’ll walk through this form so you know everything you’re supposed to about IRS Form 13711, including:

- Step-by-step instructions on how to complete this form

- Filing considerations

- Other options you might have to resolve your tax debt besides an offer in compromise

Let’s begin with an overview on how to complete IRS Form 13711.

Table of contents

How do I complete IRS Form 13711?

This tax form is relatively straightforward. Let’s begin at the top with the taxpayer information fields.

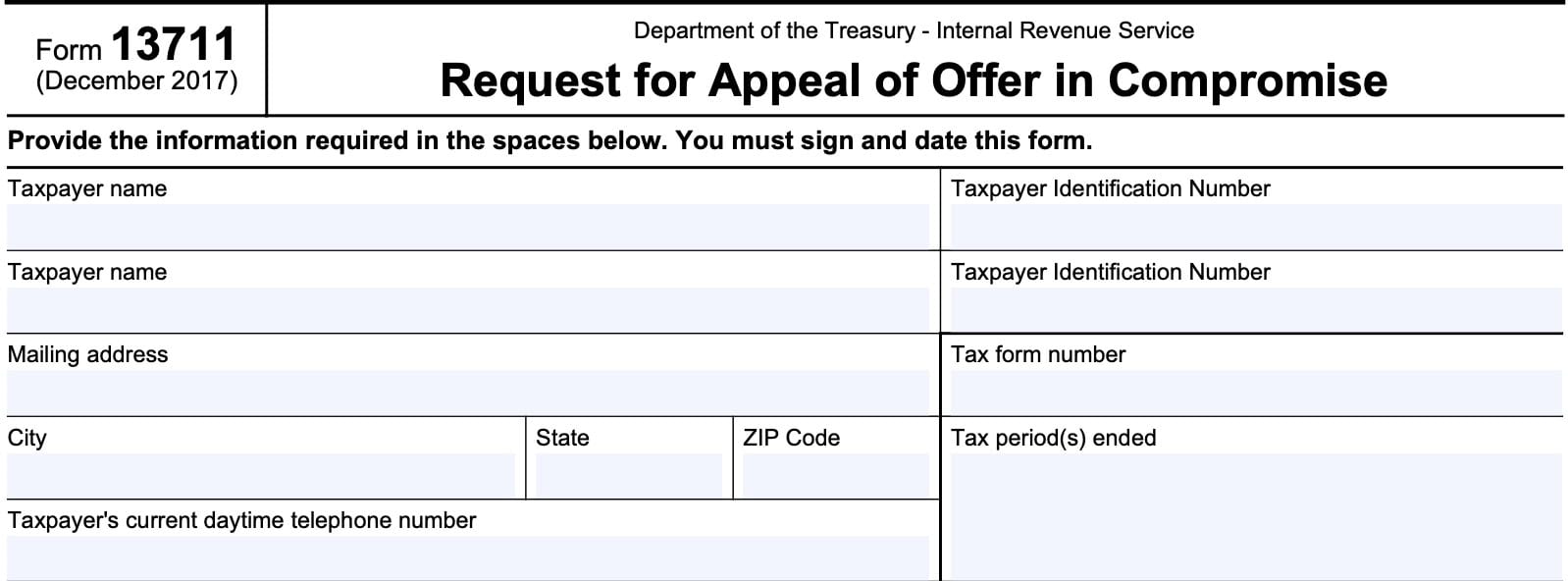

Taxpayer information

At the top of the form, you’ll need to enter your information. This will help the Internal Revenue Service recognize your tax situation and determine whether your special circumstances warrant another look.

Taxpayer name

In the space provided, enter your name as it appears on your taxpayer records or on your tax returns. If you are married filing a joint tax return, enter your spouse’s name in the space provided, as well.

Taxpayer identification number

Enter you taxpayer identification number in this field.

Individual taxpayers

Individual taxpayers should include their Social Security number in this field.

If you do not have a Social Security number, but you have an individual taxpayer identification number (ITIN), then enter your ITIN instead.

Joint couples should enter the taxpayer identification number for both spouses in the spaces provided.

Non-individuals

Businesses (including S corporations), estates and trusts, tax-exempt organizations, and other non-individual tax entities should have an employer identification number (EIN). If you have an EIN, enter that number in the space provided.

Mailing address

Enter your mailing address in the space provided. Be sure to include the city, state, and ZIP code below the street address.

Changing your address

When receiving IRS correspondence, it is always important to keep your address up to date in your tax records. That way, you can keep on top of the latest letter or update.

When working your way through the IRS appeals process (or any aspect of IRS collection activities), it is even more important to keep your address up to date.

The easiest way to update your address is to file your regular tax return with the new address. However, if you’ve recently filed, or you know that you should expect IRS correspondence before your next tax return is due, then you should file a change of address form:

- Individual taxpayers: IRS Form 8822, Change of Address

- Businesses & non-individuals: IRS Form 8822-B, Change of Address or Responsible Party – Business

Tax form number

Enter the tax form number as it appears in your IRS letters concerning your unpaid taxes. For example, most individual taxpayers would enter IRS Form 1040.

Tax Period(s) Ended

Enter the ending date (or dates) of the tax period or periods involving your unpaid taxes.

Taxpayer’s current daytime telephone number

Enter your telephone number in the space provided.

Authorized representative information

If you’ve appointed a tax professional, such as a certified public accountant or enrolled agent, to represent your interests in front of the IRS, you’ll enter that person’s information in this section.

Name of authorized representative

Enter the name of your authorized representative here.

Appointing an authorized representative

The IRS will only recognize someone to represent you in the appeals process that you have appointed using IRS Form 2848, Power of Attorney and Declaration of Representative. You must attach a completed copy of Form 2848 with your request.

Representative’s mailing address

Your representative’s mailing address goes into this space.

Authorized representative’s telephone number

Enter your representative’s telephone number in this space.

Best time to call

Your representative should enter the best times for the IRS office to call with regards to your tax problem.

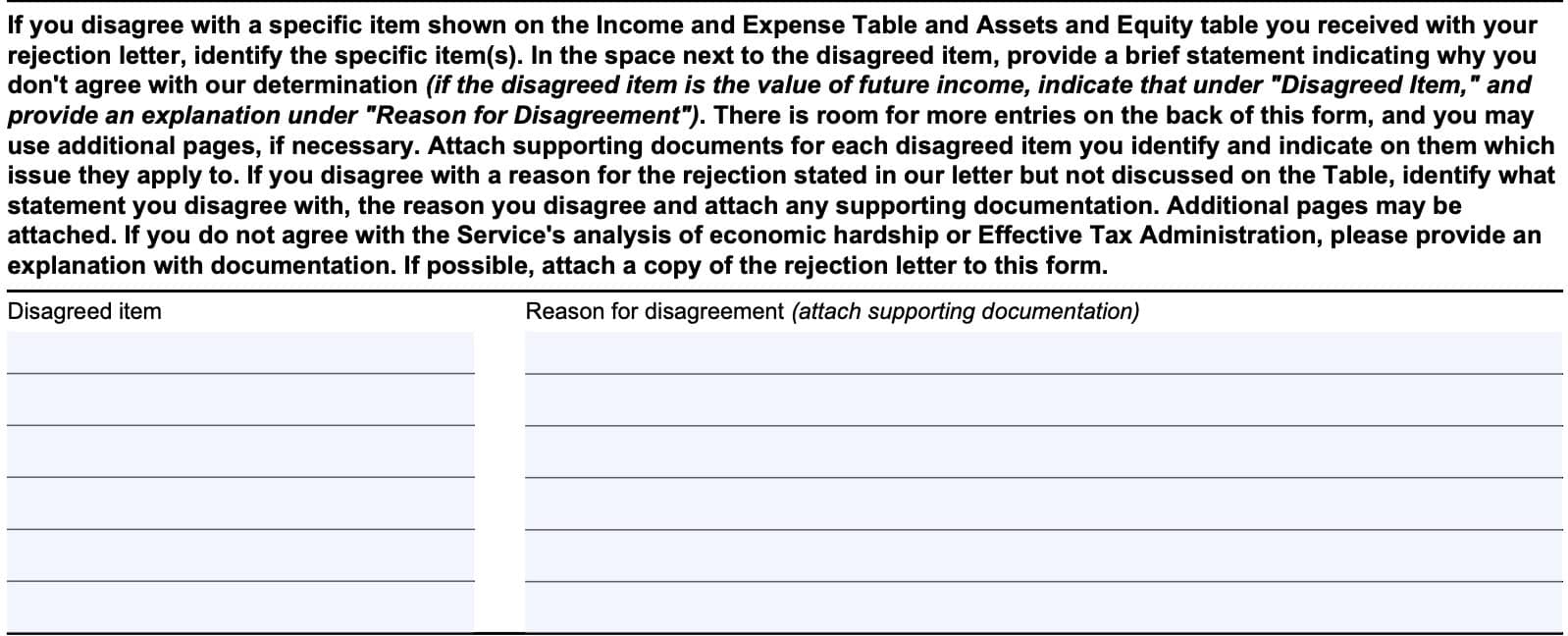

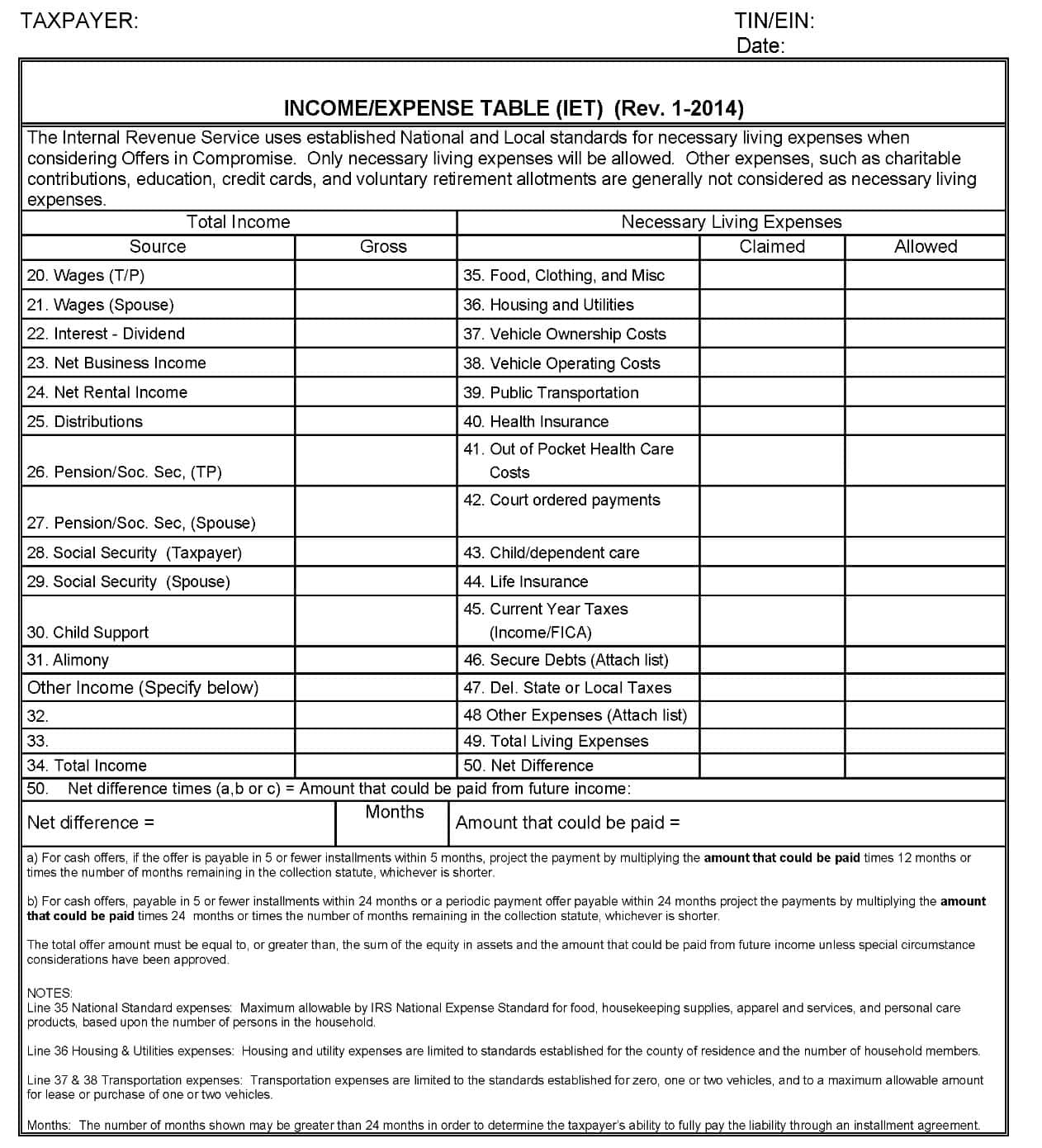

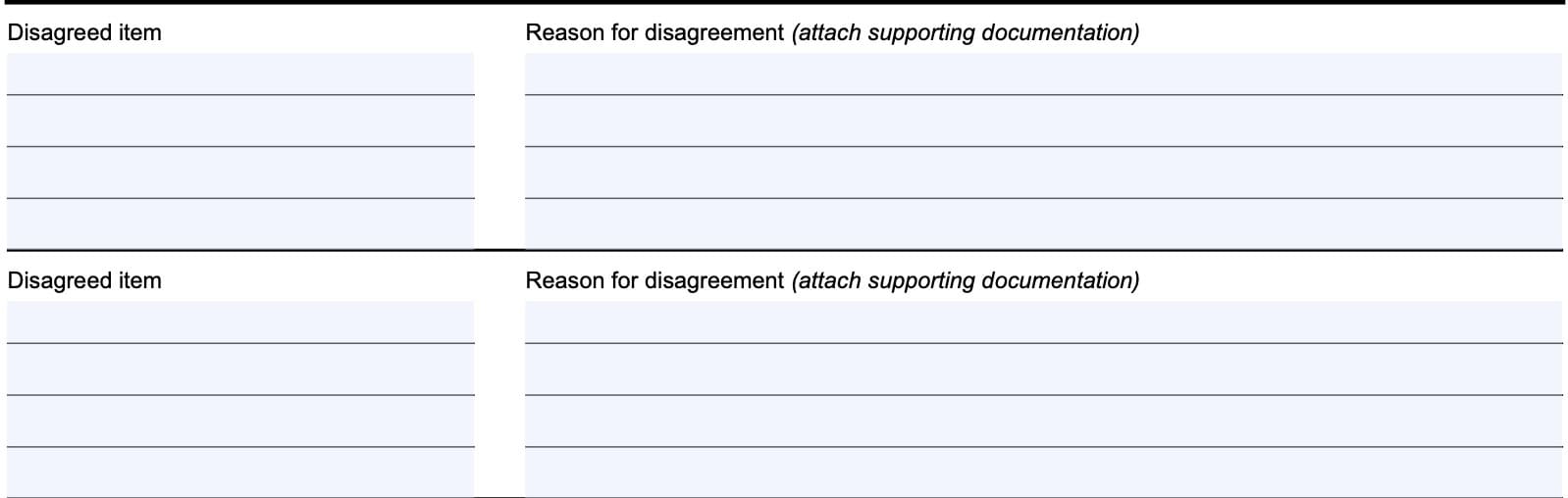

Disagreed item or items

IRS Form 13711 provides sufficient space for taxpayers to indicate one or more items that they may disagree with, from the rejected offer in compromise rejection letter.

You should have a copy of the rejection letter, as well as the following items for quick reference:

- Income and expense table

- Assets and equity table

You should have received copies of these tables, with an IRS determination, when you received your OIC denial letter. Let’s take a look at what you should do if you disagree with something on one of these tables.

If you disagree with a specific item shown on the income and expense table or assets and equity table

If you disagree with a specific item on either table that you received with your rejection letter, then you should identify that item and enter a brief statement outlining your argument.

Also, be prepared to attach supporting documents if they contain additional information about the disputed item.

If you disagree with a reason for the rejection stated in our letter but not discussed on a table

Perhaps you disagree with the IRS’ stated reason for rejecting your offer in compromise application, which wasn’t discussed on either the income and expense table or the assets and equity table.

In this situation, you should:

- Identify the statement that you disagree with and why you disagree with it

- Attach supporting documentation to support

If you do not agree with the Service’s analysis of economic hardship or effective tax administration

You can provide a written explanation with supporting documentation. You should also attach copy of the rejection letter to IRS Form 13711 when you submit it.

Before you do this, it might be useful to better understand the IRS definition of economic hardship and effective tax administration.

How the IRS defines economic hardship

Internal Revenue Code 6343 authorizes the IRS to suspend collection actions when the Treasury Secretary determines that a collection action may create an economic hardship.

Treasury Regulations and the Internal Revenue Manual (IRM) further define this term as occurring when an individual is unable to pay his or her reasonable basic living expenses.

According to IRM 5.8.11.3.1, below are factors that the IRS will consider when determining whether a taxpayer’s financial hardship rises to the level of economic hardship:

- Basic living expenses

- Age and employment status,

- Family size: Number, age, and health of the taxpayer’s dependents,

- Cost of living in the area the taxpayer resides, and

- Any extraordinary circumstances such as:

- Special education expenses

- Medical catastrophe, or

- Natural disaster

Below are additional factors that may support an economic hardship determination:

- The taxpayer is incapable of earning a living because of a long term illness, medical condition or disability, and it is reasonably foreseeable that the financial resources will be exhausted providing for care and support during the course of the condition

- The taxpayer may have a set monthly income and no other means of support and the income is exhausted each month in providing for the care of dependents.

- The taxpayer has assets, but is unable to borrow against the equity in those assets, and liquidation to pay the outstanding tax liabilities would render the taxpayer unable to meet basic living expenses.

Let’s take a closer look at effective tax administration.

How the IRS defines effective tax administration

In addition to economic hardship, the IRS will decide whether to accept an offer-in-compromise application based upon effective tax administration.

Effective tax administration includes economic hardship and public policy or equity grounds. In other words, a taxpayer can make a case that a certain IRS position is not consistent with sound public policy.

According to IRM 5.8.11.5.1, a taxpayer must establish they have:

- Exceptional circumstances that warrant acceptance of an OIC,

- Even though similarly situated taxpayers may have paid their full tax liability

Let’s take a look at some of the other things the IRS recommends you take a look at.

Things you should review

According to the IRS website, below is a partial list of things you should review as you compile your appeal.

- The Asset/Equity (AET) and Income/Expense (IET) Tables that accompanied the OIC denial letter;

- Your completed Form 433-A (OIC), Collection Information Statement for Wage Earners and Self-Employed Individuals;

- Compare your Form 433-A with your AET or IET tables for accuracy

- Be sure that you completed your Form 433-A in accordance with the IRS instructions

- The supporting documentation submitted with the Form 433-A (OIC); and

- Did you submit enough documentation with your original OIC statement?

- Publication 1854: How to Prepare a Collection Information Statement PDF.

- Did you miss any steps when completing your collection information statement?

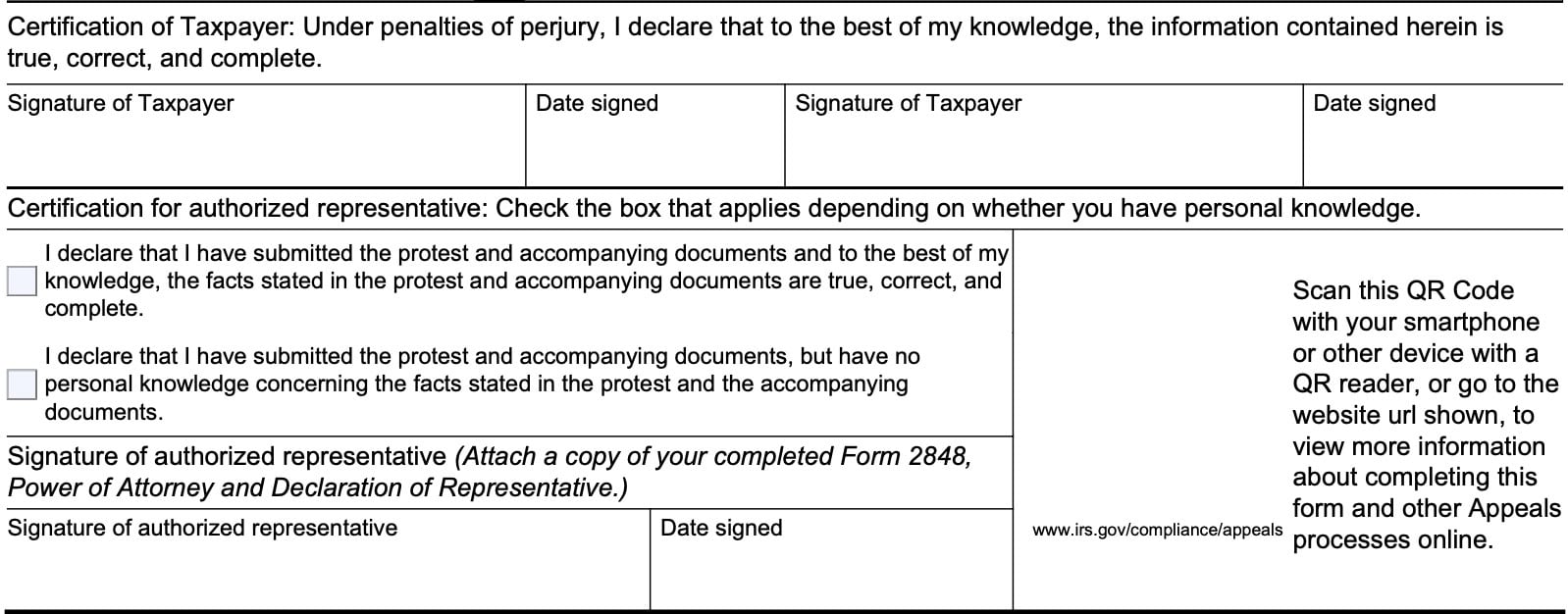

Certification and signature

At the bottom of the form, both the taxpayer and his or her authorized representative will:

- Certify that the following information is true, correct, and complete to the best of their knowledge

- Under penalties of perjury

- Sign and date the completed form

Married couples filing jointly should have both spouses sign the form.

Authorized representative certification

Your authorized representative should check the appropriate box, based upon whether he or she has personal knowledge about the facts listed in your protest.

If your representative has actually reviewed the information and is generally aware of the facts as you understand them, then he or she should check the first box. If your representative does not have personal knowledge about your financial situation, then he or she may select the second box.

Additional fields

Additional space is provided on Page 2 of this form, if you have additional information to support an appeals review.

Filing considerations

Below are some things you should consider when preparing IRS Form 13711.

The IRS website does not contain specific instructions for this tax form

Normally, the IRS website will contain a set of instructions on how to complete a tax form, as well as when to file and where you should file that form.

Since IRS Form 13711 does not contain instructions, you should follow the instructions on your rejection letter. Your letter should also include contact information

You may have options besides an offer in compromise

In addition to requesting a review from the IRS Independent Office of Appeals, you may be able to pursue one of the following:

- Installment agreement or periodic payment plan

- Penalty abatement, if you can demonstrate that this was a first-time occurrence or you have reasonable cause

- Mediation, if you don’t agree with the IRS examiner or revenue officer, but you believe that you can reach a solution

You only have 30 days to request an appeal of the IRS decision

If you received a letter notifying you that the IRS rejected your offer, you have 30 days from the date of the OIC rejection letter to request an appeal of the decision. If it’s been more than 30 days from the date of the rejection letter, your appeal won’t be accepted.

Remember to mail your appeal to the office that sent you the rejection letter.

Video walkthrough

Watch this YouTube video to learn how to complete IRS Form 13711, step by step.

Frequently asked questions

IRS Form 13711, Request for Appeal of Offer in Compromise, is the tax form that individuals and businesses may use if the IRS has rejected an offer in compromise. Taxpayers must request an appeal within 30 calendar days of the date on the rejection letter.

You generally have 30 calendar days from the rejection letter date to request an appeal from the IRS’ Independent Office of Appeals. According to the IRS, appeals requested to review a rejected offer after the 30-day period will not be considered.

According to the IRS, an offer in compromise allows you to settle your tax debt for less than the full amount you owe. It may be a legitimate option if you can’t pay your full tax liability or doing so creates a financial hardship.

Where can I find IRS Form 13711?

You can find IRS Form 13711 on the IRS website. For your convenience, we keep the latest versions of IRS forms, such as IRS Form 13711, in our articles.