IRS Form 5713: International Boycott Report Guide

Section 999 of the Internal Revenue Code requires United States based taxpayers who conduct business involving international boycotts to submit an annual report to the Secretary of the Treasury. The Internal Revenue Service created IRS Form 5713 as an information return to meet this requirement.

This article will walk you through the basics of this tax form, including:

- Which taxpayers must file IRS Form 5713

- Conditions under which taxpayers file IRS Form 5713

- How to complete IRS Form 5713

Let’s start with some background information on this IRS form.

Contents

What is IRS Form 5713?

IRS Form 5713, International Boycott Report, is the tax form that U.S. persons use to report:

- Operations in or related to boycotting countries.

- The receipt of boycott requests and boycott agreements made

The IRS goes into a little more detail on a few key definitions.

U.S. persons

IRC Section 7701(a)(30) defines the following as U.S. persons:

- Citizens or residents of the United States

- U.S. companies, such as corporations or partnerships

- Any estate, other than a foreign estate

- Any trust in which:

- A U.S. court has primary jurisdiction, or

- One or more U.S. persons has authority over all substantial decisions of the trust

Operations

The IRS considers the term ‘operations’ to include all forms of business or commercial activities and transactions that include, but are not limited to, the following:

- Sales

- Purchases

- Leases

- Licensing

- Banking

- Financing or similar activities

- Extraction operations

- Processing

- Manufacturing & producing

- Construction

- Transportation

- Activities related to operations, such as negotiating contracts, advertising, etc.

- Performing services, even if not related to one of the activities previously listed

This term is used to describe types of operations that may be reportable.

Operations in a boycotting country

The IRS considers a U.S. taxpayer to have operations “in a boycotting country” if there is an operation that is carried out, in whole or in part, in a boycotting country, either for or with:

- The government, or government entities

- A company, or

- A national of a boycotting country

Operations with the government, a company, or a national of a boycotting country

You are considered to have operations “with the government, a company, or a national of a boycotting country” if you have an operation that is carried on outside a boycotting country either for or with:

- The government,

- A company, or

- A national of a boycotting country

Operations related to a boycotting country

You are considered to have operations “related to a boycotting country” if you have an operation that is carried on outside a boycotting country for the government, a company, or a national of a nonboycotting country if you know or have reason to know that specific goods or services produced by the operation are intended for use:

- In a boycotting country, or

- For use by or for the benefit of

- The government,

- A company, or

- A national of a boycotting country, or

- For use in forwarding or transporting to a boycotting country

List of boycotting countries

The Treasury Department maintains a list of countries considered to be boycotting countries. At the current time, this list includes:

- Iraq

- Kuwait

- Lebanon

- Libya

- Qatar

- Saudi Arabia

- Syria

- Yemen

The United Arab Emirates (UAE) was previously on the list of boycotting countries, but was removed as of April 8, 2021. Taxpayers only need to file Form 5713 for activities through the effective date of April 8, 2021.

When must a taxpayer file IRS Form 5713?

In addition to U.S. persons who directly have reportable operations, the following must also file IRS Form 5713:

- A member of a controlled group, as defined in IRC Section 993(a)(3), a member of which has operations.

- A U.S. shareholder (within the meaning of Section 951(b)) of a foreign corporation that has operations

- Only applies if the shareholder owns (within the meaning of Section 958(a)) stock of that foreign corporation).

- A partner in a partnership that has operations.

- A person treated (under Section 671) as the owner of a trust that has operations.

Exceptions to filing requirements

There are certain exceptions to the filing requirement, as well. Here are the filing requirement exceptions.

Foreign persons

A foreign person is not required to file Form 5713 unless that person:

- Claims the benefits of the foreign tax credit,

- Owns stock in an interest charge domestic international sales corporation (IC-DISC),

- Is a foreign sales corporation (FSC) that has exempt foreign trade income, or

- Has extraterritorial income (defined in IRC Section 114(e), as in effect before its repeal) excluded from gross income.

Members of a controlled group

A corporation that is a member of a controlled group, as defined in Section 1563 is not required to file Form 5713 if:

- All members of the controlled group joined in the filing of a consolidated income tax return and

- The common parent files Form 5713 on behalf of all members of the controlled group

If all members of a controlled group did not join in the filing of a consolidated income tax return, each member of the controlled group must file Form 5713 separately.

A member of a controlled group, as defined in Section 993(a)(3), is not required to file Form 5713 if all of the following conditions apply.

- The member has no operations in or related to a boycotting country (or with the government, a company, or a national of a boycotting country).

- The member did not own stock, directly or indirectly, in any corporation having such operations.

- The member did not receive any boycott requests.

- The member did not own stock, directly or indirectly, of any corporation receiving a request.

- The member is not entitled to (or forfeits) the benefits of the foreign tax credit, the deferral of earnings of a controlled foreign corporation (CFC), IC-DISC benefits, FSC benefits, or the extraterritorial income exclusion.

- The member attaches to its tax return a certificate stating that Form 5713 was filed on the member’s behalf. This certificate must be signed by a person authorized to sign the income tax return of the common parent of the group.

Partners

A partner is not required to file Form 5713 if:

- That partner has no boycott operations that are independent of the partnership,

- The partnership files Form 5713 with IRS Form 1065, and

- The partnership did not cooperate with or participate in an international boycott

U.S. approved boycotts

A taxpayer can comply with an international boycott imposed by a foreign country if the boycott is approved by:

- U.S. law,

- Federal regulations, or

- Executive order

Taxpayers should not report U.S. approved boycotts on Form 5713.

Unsolicited invitations to bid

Taxpayers who receive an unsolicited invitation to bid for a contract that contains a request to participate in or cooperate with an international boycott, must file Form 5713 only if they accept the invitation.

Foreign corporations with U.S. sister or subsidiaries

A U.S. corporation that is a subsidiary or sister corporation of a foreign corporation can waive the requirement to report boycott operations of its foreign parent or sister corporation if they meet the following conditions:

- The foreign corporation is not required to file Form 5713 independent of its relationship with the U.S. subsidiary or sister corporation

- The U.S. subsidiary or sister corporation agrees to forfeit the benefits of:

- The foreign tax credit

- Deferral of taxation of earnings of a CFC

- IC-DISC benefits

- FSC benefits

- Extraterritorial income exclusion

Foreign corporation with U.S. branch

A foreign corporation engaged in a U.S. trade or business through a U.S. branch generally is required to file Form 5713 to report the boycott activities of its controlled group, including the U.S. branch. When reporting for the U.S. branch, the foreign corporation must report all information related to the U.S. branch’s boycott activities, including the boycott activities that do not relate to the U.S. trade or business.

The foreign corporation can, however, waive the requirements to report information about its U.S. branch if it does not claim or forfeits the benefits of:

- The foreign tax credit

- Deferral of taxation of earnings of a CFC

- IC-DISC benefits

- FSC benefits

This waiver does not relieve the foreign corporation of reporting boycott activities of all U.S. corporations that are members of the same controlled group of which the foreign corporation is a member.

Penalties for not filing IRS Form 5713

Willful failure to properly file Form 5713 can result in:

- $25,000 fine, and/or

- Up to 1 year imprisonment

How do I complete IRS Form 5713?

We’ll walk through this IRS form step by step. Most taxpayers might be better off having a tax professional, such as an enrolled agent or CPA, prepare this form with their tax returns.

Let’s start at the top of the form.

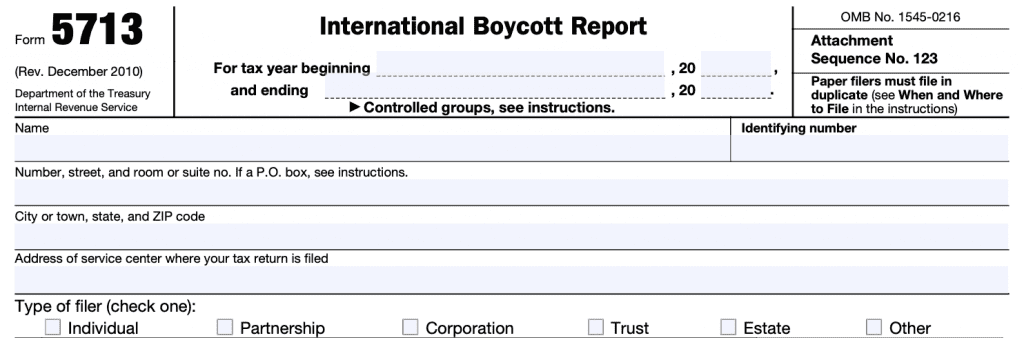

Taxpayer information

The top of the form contains taxpayer information, including:

- Tax year

- Taxpayer name

- Taxpayer identifying number

- This can be a Social Security number, taxpayer identification number, or employer identification number (EIN)

- Address, including city, state, zip code

- IRS Service Center address

- Type of filer (individual, partnership, etc.)

Income information

The following section contains income information. Complete the applicable section.

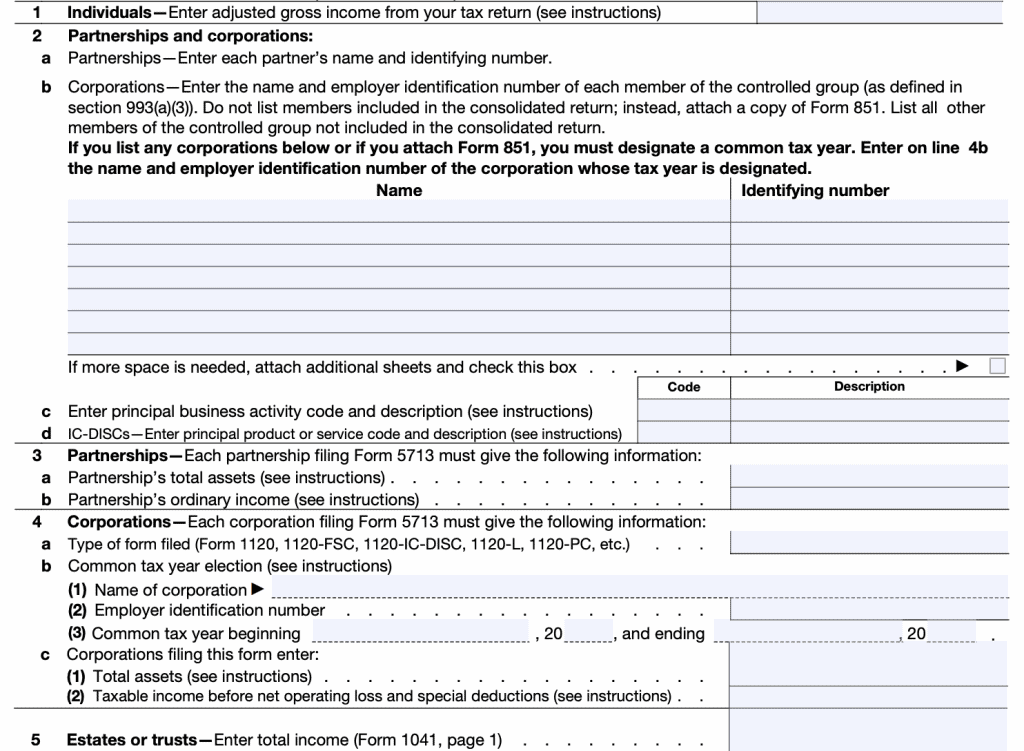

Line 1: Individuals

Enter the adjusted gross income (AGI) from your federal income tax return as computed on Form 1040.

Line 2: Partnerships and corporations

Partnerships and corporations fill in Line 2, as appropriate.

Line 2a: For partnerships, enter each partner’s name and identifying number in the field.

Line 2b: Corporations must enter the name and EIN for each controlled group member, but not individual members. Instead, attach a copy of IRS Form 851, Affiliations Schedule.

If you require more space, attach additional sheets and check the applicable box.

Line 2c: Partnerships and corporations

Enter the principal business activity code number and description from the list at the end of the form instructions. If more than one business activity code applies, enter the code number for the specific industry group from which the largest percentage of total receipts was derived.

Line 2d: IC-DISCs

Enter the major product code number for the major product or service, as measured by export gross receipts, sold or provided by the IC-DISC

This information is available on Form 1120-IC-DISC, Schedule N, Line 1a).

Line 3: Partnerships

Partnerships who file IRS Form 5713 must provide:

- Partnership’s total assets

- From the amount on Form 1065, Schedule L, “Total assets” line, column (d)

- Partnership’s ordinary income

- From Form 1065, Line 22, Ordinary business income (loss).

- For electing large partnerships, enter the portion of taxable income (Form 1065-B, amount on “Taxable income (loss) from passive loss limitation activities” line) that is attributable to trade or business activities.

Line 4: Corporations

Each corporation must give the following:

- Type of form filed

- Common tax year election (binding election that can only be changed with approval from the Treasury Secretary)

- Name of corporation

- EIN

- Common tax year with beginning and ending dates

- Total assets

- Taxable income before net operating loss and special deductions

For more specifics, refer to the form instructions.

Line 5: Estates or trusts

Estates and trusts must enter total income, found on IRS Form 1041, page 1.

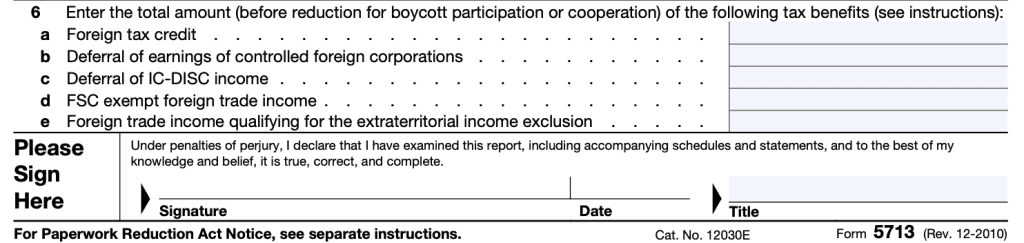

Tax benefits previously claimed

In Line 6, taxpayers will enter the total amount of certain tax benefits, before reduction for boycott participation. We’ll go through each entry, line by line.

Line 6a: Foreign tax credit

Enter on Line 6a the foreign tax credit before adjustment from either Form 1116 or Form 1118. This includes the totals of credits for taxes on:

- Section 951A category income

- Foreign branch category income

- Passive category income

- General category income

- Section 901(j) category income

- Certain income re-sourced by treaty

- Lump sum distributions

Line 6b: Deferral of earnings of CFCs

Enter the pro rata share of total earnings from CFCs, as defined in IRC Section 952(a)(3)(A), on Line 6b.

Line 6c. Deferral of IC-DISC income

Shareholders of an IC-DISC should figure the deferral as follows:

Shareholder that is not a C corporation

Enter on Line 6c the pro rata share of the Section 995(b)(1)(F)(i) amount. This is the pro rata share of the amount found on Form 1120-IC-DISC, Schedule J, Part I, Line 8.

Shareholder that is a C corporation

Enter on Line 6c the pro rata share of the Section 995(b)(1)(F)(i) amount multiplied by 16/17. This is the pro rata share of the amount found on Form 1120-IC-DISC, Schedule J, Part I, Line 8, times 16/17.

Line 6d: FSC exempt foreign trade income.

Enter on Line 6d the total exempt foreign trade income. This is the total of columns (a) and (b) of Form 1120-FSC, Schedule B, Line 10.

Line 6e: Foreign trade income qualifying for extraterritorial income exclusion.

Enter on Line 6e your foreign trade income that otherwise qualifies for the extraterritorial income exclusion. You will find this amount on IRS Form 8873, Line 49.

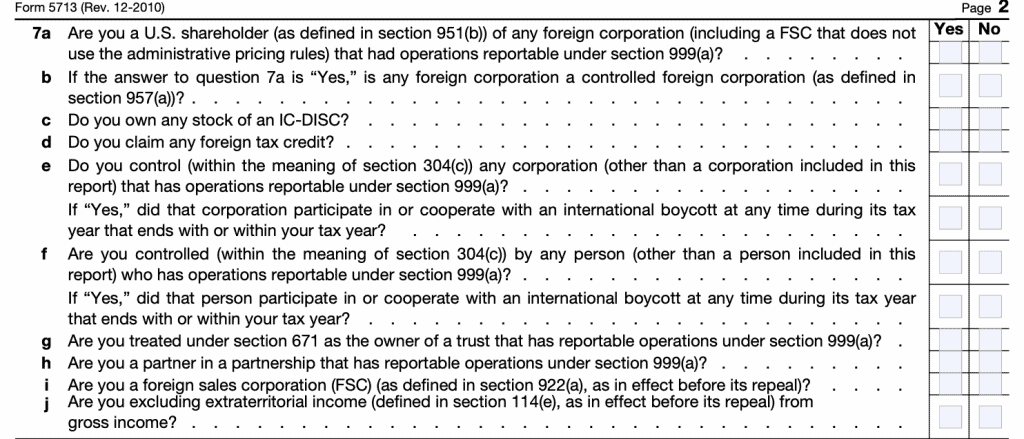

Additional questions

The top of page 2 contains 10 Yes/No questions. The form instructions contain no additional guidance on these questions.

If you cannot answer these questions on your own, you may need your tax professional to help you answer them.

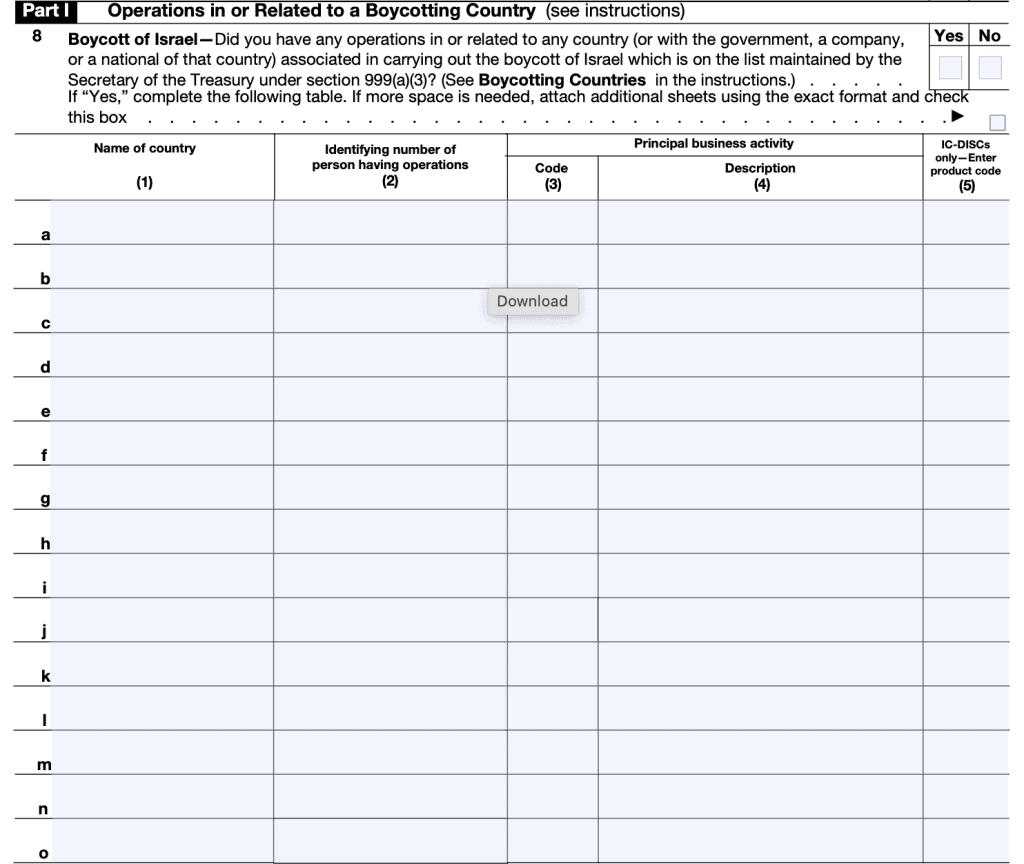

Part I: Operations in or Related to a Boycotting Country

Line 8: Boycott of Israel

The question on Line 8 concerns operations in or related to countries on the Secretary’s list of countries associated in the boycott of Israel. Use a separate line for each country or each person having operations in that country.

Do not use separate lines for separate operations by the same person in the same country.

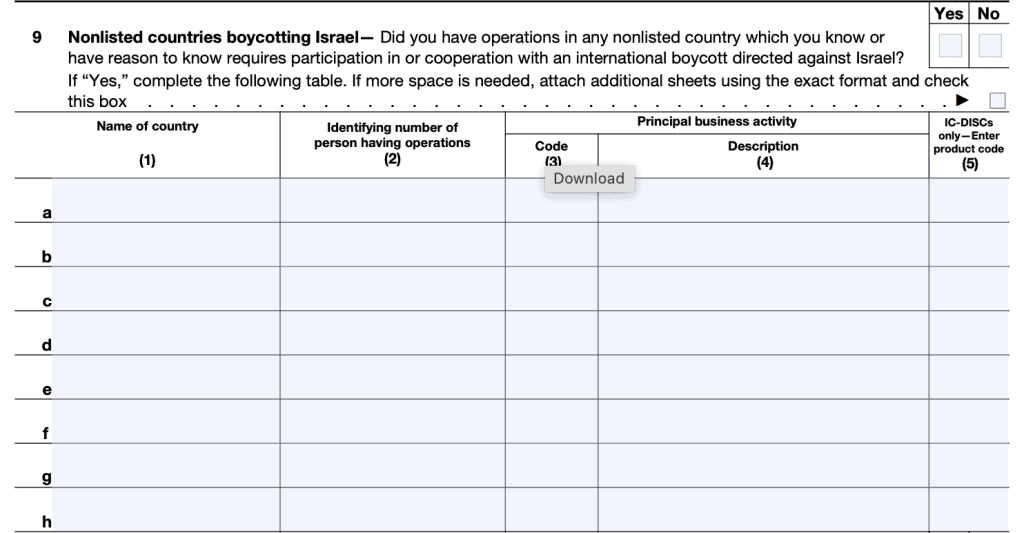

Line 9: Nonlisted countries boycotting Israel

If the answer to the question on Line 9 is “Yes,” use the same procedure outlined in the instructions for Line 8 for any nonlisted countries which you know or have reason to know require participation in or cooperation with the international boycott of Israel.

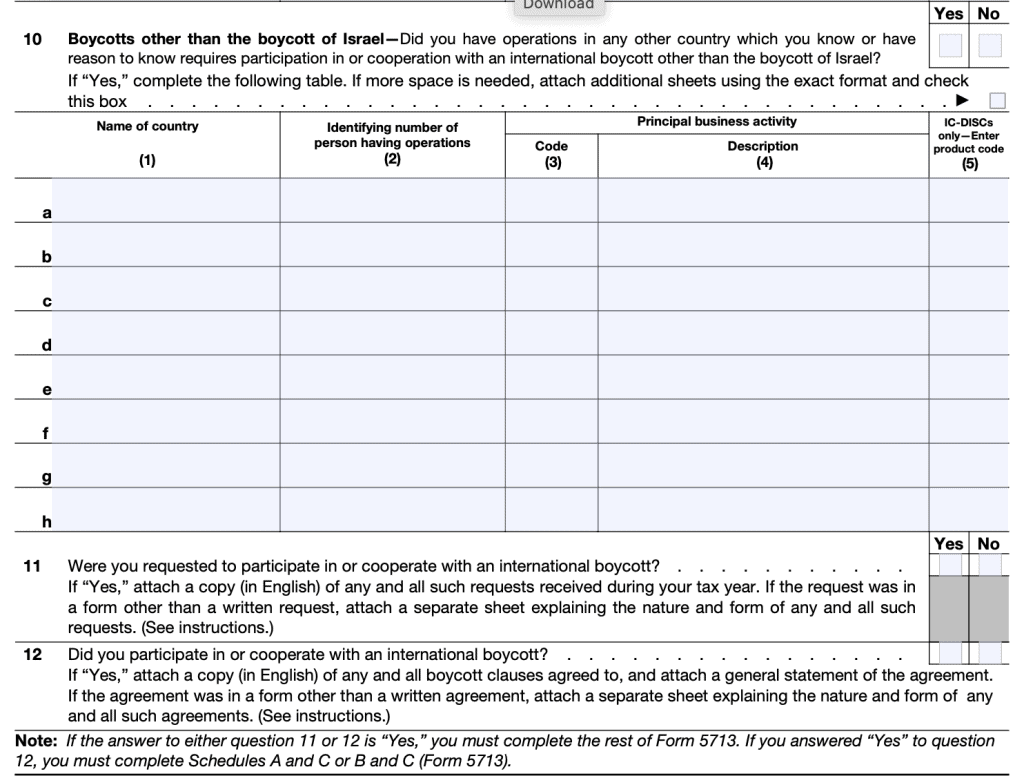

Line 10: Boycotts other than the boycott of Israel

If the answer to the question on Line 10 is “Yes,” use the same procedure outlined in the instructions for Line 8 for an international boycott other than the boycott of Israel.

Line 11: Where you requested to participate in or cooperate with an international boycott?

If Yes, attach a copy of such a request. If you routinely receive many such requests, attach one copy and an accompanying statement showing the number and nature of these requests.

Line 12: Did you participate in or cooperate with an international boycott?

If a substantial number of boycott agreements were entered into or were effective for the period covered by the report, and the boycott clauses are similar, you can attach a sample boycott clause and a statement showing the number and general nature of all other boycott clauses and agreements entered into.

An agreement to participate in or cooperate with an international boycott continues for the entire period that it is in effect and must be reported each year that it is in effect.

Note

If you answered “Yes” to either Question 11 or 12, you must complete the rest of Form 5713. Otherwise, you may stop here.

If you answered “Yes” to Question 12, you must complete either:

- Schedule A and Schedule C (not covered in this article), or

- Schedule B and Schedule C

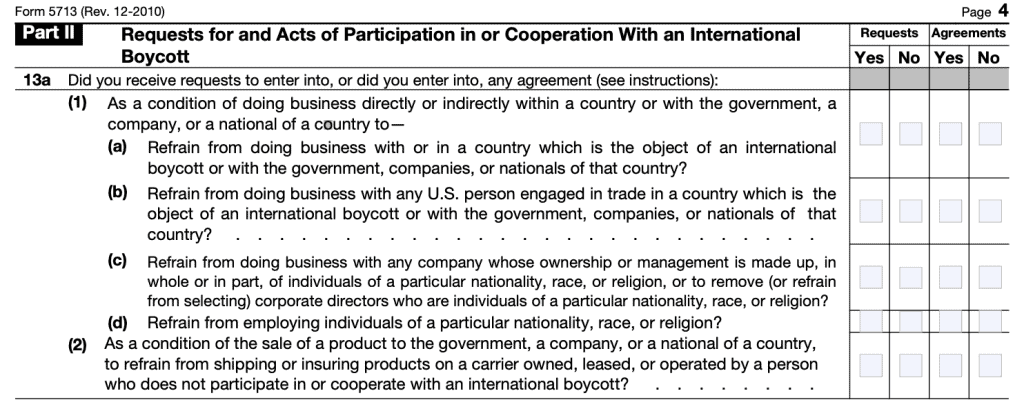

Part II: Requests for and Acts of Participation in or Cooperation With an International Boycott

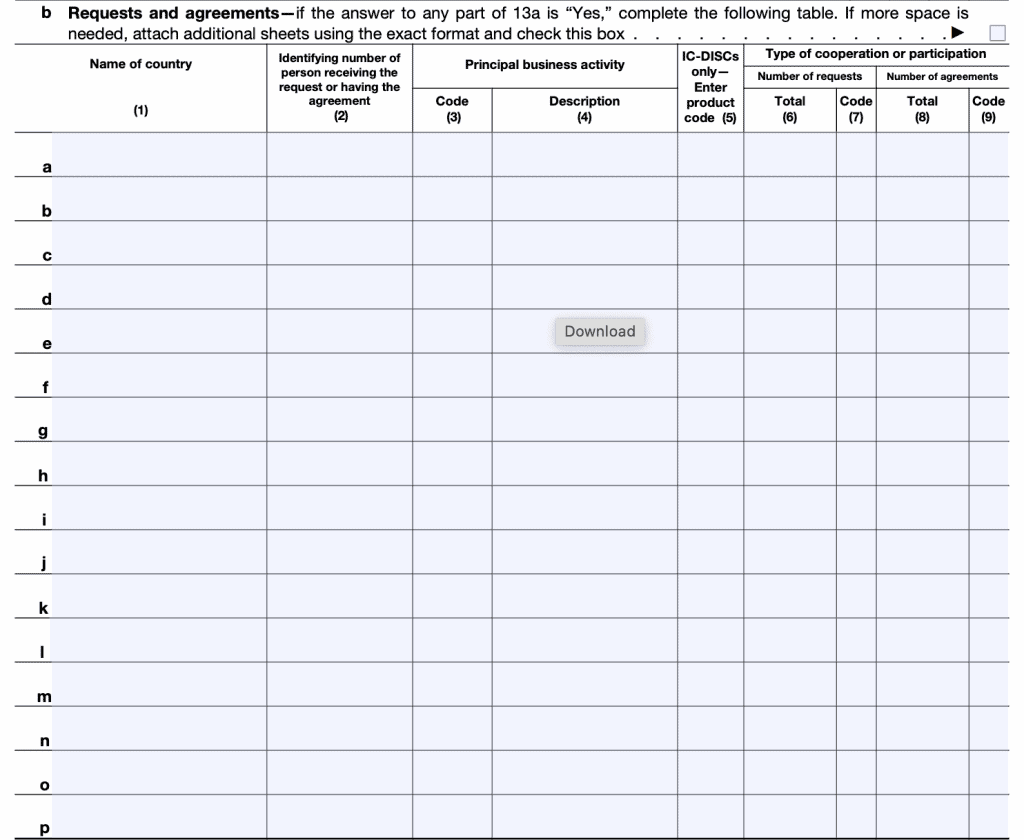

Line 13a

Answer the Yes/No, as stated. If you did not receive a reportable boycott request and no agreements were entered into or in effect, enter “No.”

Line 13b

If the answer to any part of Line 13a is “Yes,” complete the table below. For columns (7) and (9), refer to the table located in the form instructions.

What is the International Boycott Factor?

The international boycott factor helps calculate the tax effect of the international boycott provisions. The taxpayer calculates the boycott factor using Schedule A.

From there, the taxpayer can do one of the following:

- Apply the international boycott factor

- Mandatory for figuring the reduction to foreign trade income qualifying for the extraterritorial income exclusion

- Optional for determining loss of tax benefits elsewhere

- Determine attributable taxes and allocation of income directly related to boycott operations using Schedule B

From there, the taxpayer will calculate how much in additional taxes they must pay for their participation.

Where can I find a copy of IRS Form 5713?

You may pick up a copy of this tax form from the IRS website or by downloading the file below.