IRS Form 6781 Instructions

Taxpayers use IRS Form 6781 to report gains and losses from Section 1256 contracts and straddle positions.

In this article, we’ll show you what you need to know about IRS Form 6781, specifically:

- How to complete IRS Form 6781

- How Section 1256 contracts and straddles work

- Frequently asked questions

Let’s start by walking through this tax form.

Table of contents

How do I complete IRS Form 6781?

There are three parts to this one-page tax form:

- Part I: Section 1256 Contracts Marked to Market

- Part II: Gains and Losses from Straddles

- Part III: Unrecognized Gains From Positions Held on Last Day of Tax Year

Let’s start at the top of this IRS tax form.

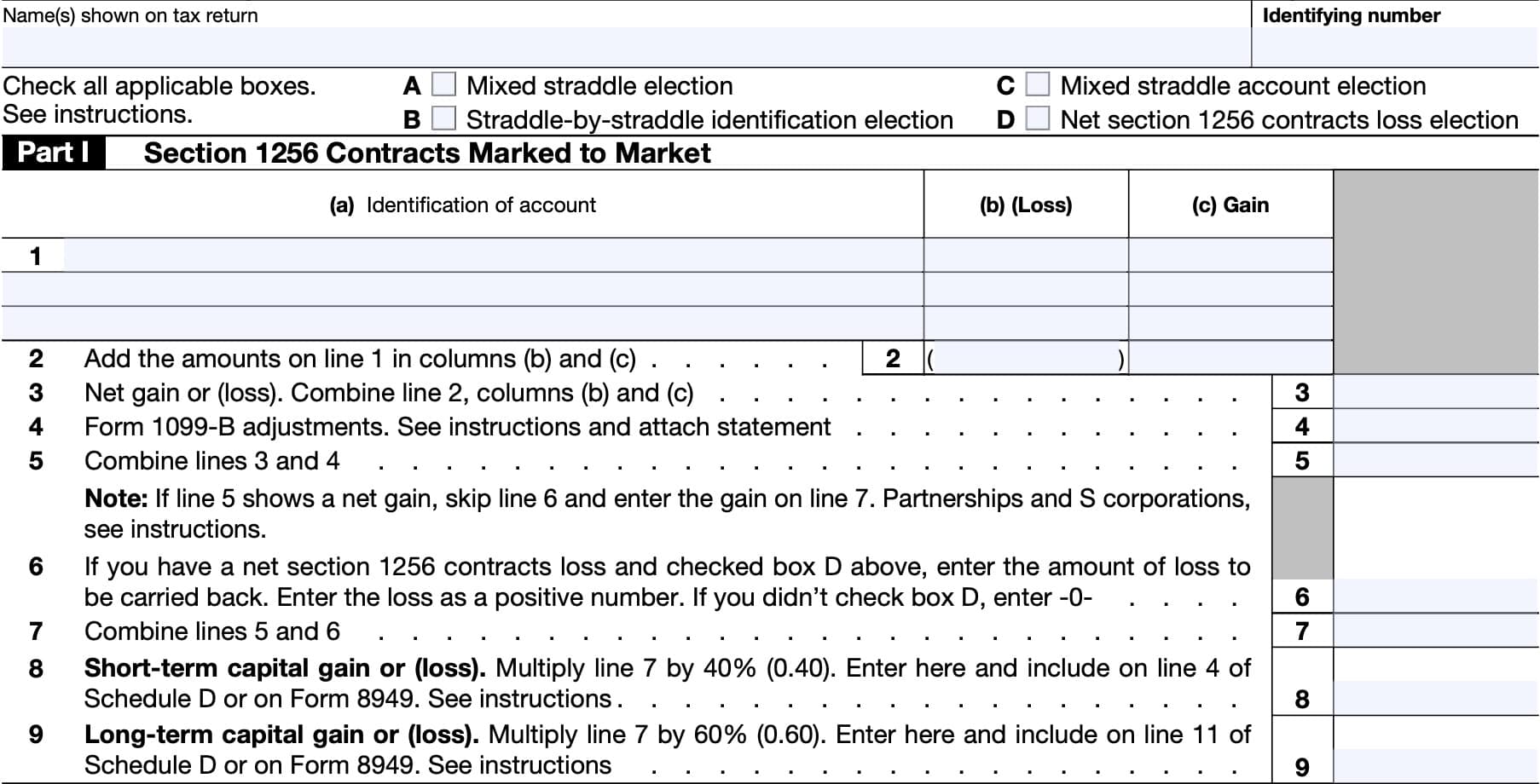

Part I: Section 1256 Contracts Marked to Market

Just before Part I, you’ll need to ensure that the taxpayer name and identifying number fields match the information in your tax return.

For individual tax filers, your identifying number will likely be your Social Security number. For estates and trusts, this will be the employer identification number.

Just below the taxpayer information fields, you’ll need to check one or more of the following boxes:

- Box A: Mixed straddle election

- Box B: Straddle-by-straddle identification election

- Box C: Mixed straddle account election

- Box D: Net Section 1256 contracts loss election

Let’s go over each in a little more detail.

Box A: Mixed straddle election

Under Internal Revenue Code Section 1256(d), you can elect to have the mark-to-market rules not apply to Section 1256 contracts that are part of a mixed straddle.

A mixed straddle is any straddle in which at least one but not all of the positions is a Section 1256 contract. On the day the first section 1256 contract forming part of the straddle is acquired, you must identify each position forming part of the straddle as being part of this straddle.

If you make this election, it will apply for all later years. You cannot revoke a previously made mixed straddle election without IRS consent.

If you are making or have previously made this election, check box A and report the Section 1256 contract component in Part II instead of in Part I.

Box B: Straddle-by-straddle identification election

Make this election for mixed straddles according to Temporary Regulations section 1.1092(b)-3T(d). To do this, clearly identify each position by the earlier of:

- The close of the business day in which the identified mixed straddle is established, or

- The time that you dispose of the position

No straddle-by-straddle identification election can be made for any straddle where a mixed straddle election was previously made, or if at least one position is includible in the mixed straddle account.

If you have previously made this election, check Box B.

Box C: Mixed straddle account election

According to Temporary Regulations section 1.1092(b)-4T(f), you will check Box C to establish one or more mixed straddle accounts for the upcoming tax year by the tax return’s due date (without extensions). Additionally, you’ll need to attach a statement required by the Temporary Regulations.

Report the annual account net gain or loss from a mixed straddle account in Part II and identify the

election. Temporary Regulations Section 1.1092(b)-4T(c)(4) contains additional information regarding limits on the total annual account net gain or loss

Box D: Net Section 1256 contracts loss election

If you have a net Section 1256 contracts loss for the tax year, you can elect to carry it back 3 prior years. However, corporations, partnerships, estates, and trusts are not eligible to make this election.

Your net Section 1256 contracts loss is the

smaller of:

- The excess of your losses from Section 1256 contracts over the total of

- (a) Your gains from section 1256 contracts plus

- (b) $3,000 ($1,500 if married filing separately), or

- The total you would calculate as your short-term and long-term capital loss

carryovers to the subsequent tax year if Line 6 were zero.- Use a separate Schedule D and capital loss carryover worksheet from IRS Publication 550 to calculate the total amount.

The amount that you can carry back to a prior tax year is the smaller of:

- Any gain that you would report on Line 16 of Schedule D for that carryback year if only gains and losses from Section 1256 contracts were considered, or

- The actual gain, if any, reported on Line 16 of Schedule D for that carryback year

Once you’ve checked the appropriate box(es), let’s go to Line 1.

Line 1

Enter the following information for each contract with open positions:

- Column (a): Identification of account

- If you received Form 1099-B, write ‘Form 1099-B’ and the broker’s name

- Separately list each transaction for which you either:

- Did not receive a Form 1099-B, or

- Received a Form 1099-B for a different tax year

- Column (b): Capital loss associated with the account

- Column (c): Capital gain associated with the account

Net Section 1256 contracts loss carryback

If you are completing an amended Form 6781 to carry back a net Section 1256 contracts loss from a future tax year, you’ll have to report the carryback here.

Simply enter “Net section 1256 contracts loss carried back from” and the applicable tax year in Column (a). Then enter the amount of the loss carried back to the current tax year in Column (b).

Line 2

Add the loss amounts in Column (b), and the gain amounts in Column (c). Enter the results in the respective column in Line 2.

Line 3

Combine the total gains and losses from Line 2. Enter any loss as a negative number.

Line 4: Form 1099-B adjustments

If the Form 1099-B you received includes a straddle or hedging transaction (as defined in IRC Section 1256(e)(2)), you may need to make certain adjustments.

To do this, attach a statement listing each of the following adjustments, then enter the total on Line 4:

- The Section 1256 contract part of a mixed straddle, if you made any of the mixed straddle elections

- The amount of the loss, if:

- You didn’t make any of the mixed straddle elections or

- If the straddle wasn’t identified as a mixed straddle and you had a loss on the Section 1256 contract part that was less than the unrecognized gain on the non-Section 1256 contract part.

- If the unrecognized gain is less than the loss, enter the unrecognized gain.

- Use Part I for a loss on the disposition of one or more positions that are part of a mixed straddle and that are non-Section 1256 positions if:

- No disposition of a non-Section 1256 position in the straddle would be a long term capital gain or loss, and

- The disposition of one or more section 1256 positions in the straddle would be a capital gain or loss.

- The Section 1256 contract part of a hedging transaction.

- The gain or loss on a hedging transaction is treated as ordinary income or loss.

Don’t use Line 4 to show the adjustment for a qualified opportunity fund (QOF) related deferral. Instead, see the instructions for IRS Form 8949 if you need information about how to elect to defer capital gain net income because you invested in a QOF.

Line 5

Combine Line 3 and Line 4, then enter the total here.

If Line 5 shows a net gain, then skip Line 6 and enter the net gain on Line 7.

Partnerships

Partnerships will enter the amount from Line 5 on IRS Form 1065, Schedule K, Line 11.

Leave Lines 6 through 9 blank. They do not apply to partnerships or S corporations.

S corporations

S corporations will enter the Line 5 amount on IRS form 1120-S, Schedule K, Line 10.

Leave Lines 6 through 9 blank. They do not apply to partnerships or S corporations.

Line 6

If you have a net Section 1256 contracts loss and checked box D above, enter the amount of loss to

be carried back, as a positive number. Otherwise, enter ‘0.’

Line 7

Add Line 5 and Line 6. Enter the total here.

Line 8: Short-term capital gain (or loss)

Multiply the Line 7 figure by 40% (0.40). This represents your short-term gains or short-term capital loss from your straddles.

Unless you’re deferring part of this as part of a QOF investment, you’ll enter this number on Line 4 of IRS Schedule D.

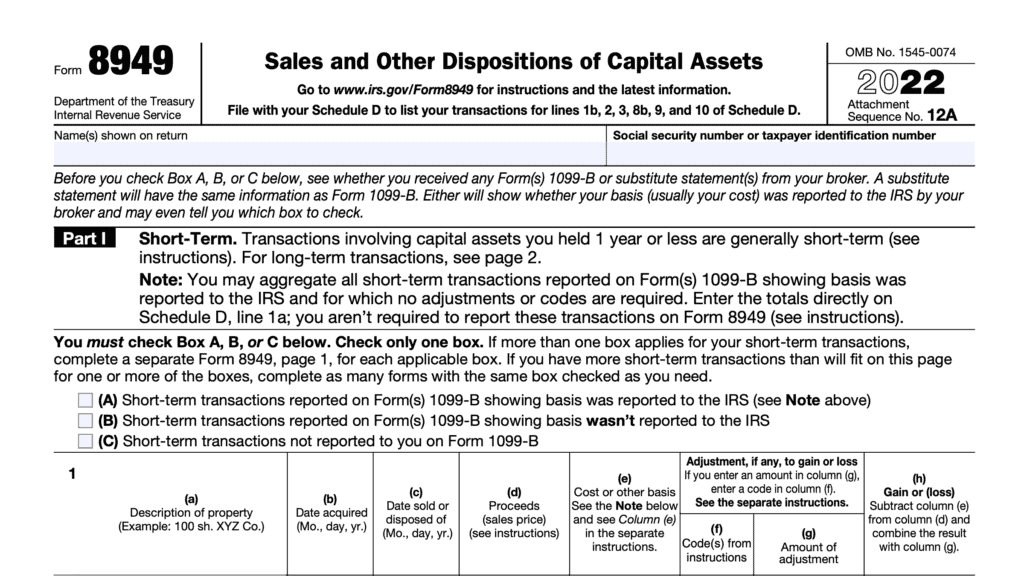

QOF investment

If deferring part of a gain, enter the gain in Part I of IRS Form 8949.

Check Box B and enter every Line 1 transaction for which you received a 1099-B form or substitute statement.

Check Box C for transactions where you cannot check Box B. You may need to complete multiple versions of Form 8949 if you have Box B transactions and Box C transactions.

For each transaction, enter the following information:

- Column (a): “Form 6781, Part I

- Column (h): Amount of gain or loss

Leave all other columns blank.

Line 9: Long-term capital gain (or loss)

Multiply the Line 7 figure by 60% (0.60). This represents your long-term gains or long-term capital loss from straddle positions.

Unless you’re deferring part of this as part of a QOF investment, you’ll enter this number on Line 11 of IRS Schedule D.

QOF Investment

If deferring part of a gain, enter the gain in Part II of IRS Form 8949.

Check Box E and enter every Line 1 transaction for which you received a 1099-B form or substitute statement.

Check Box F for transactions where you cannot check Box B. You may need to complete multiple versions of Form 8949 if you have Box E transactions and Box F transactions.

For each transaction, enter the following information:

- Column (a): “Form 6781, Part I

- Column (h): Amount of gain or loss

Leave all other columns blank.

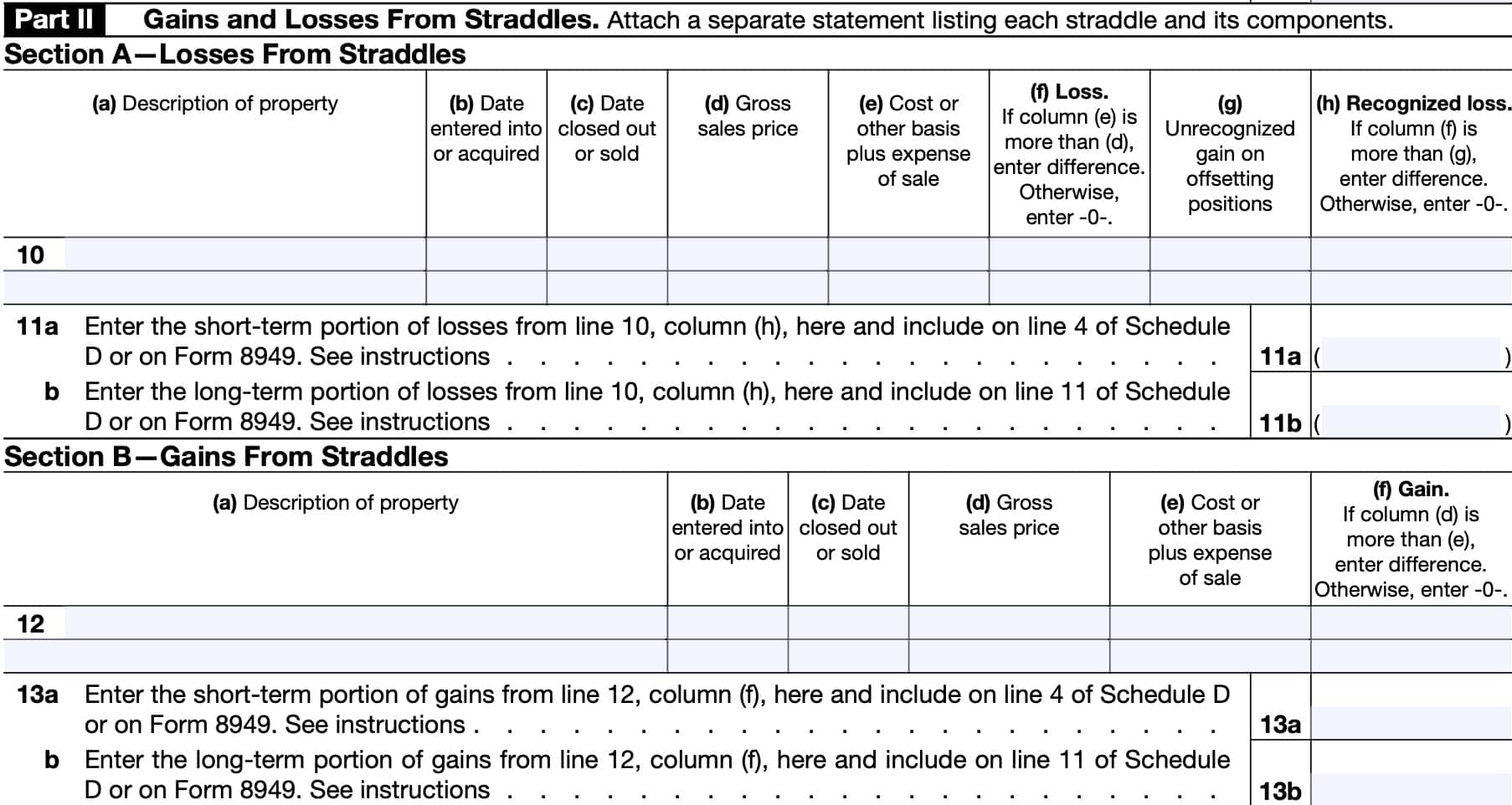

Part II: Gains and Losses from Straddles

There are two sections to Part II:

- Section A: Losses From Straddles (Lines 10 & 11)

- Section B: Gains From Straddles (Lines 12 & 13)

Use Section A for losses from positions that are part of a straddle. Afterwards, you will use Section B for gains from positions that are part of a straddle.

Allowable losses from positions that are part of a straddle

Generally, a loss is allowed to the extent it exceeds the unrecognized gain on offsetting

positions. The part of the loss not allowed is treated as if incurred in the following year and is allowed to the same extent.

However, a loss from a position established in an identified straddle after October 21, 2004, isn’t allowed.

Instead, the basis of each offsetting position in the identified straddle that has unrecognized gain is increased by the amount of the unallowed loss multiplied by the following ratio:

Unrecognized gain (if any) divided by

Total unrecognized gain on all positions that offset the loss position in the identified straddle

For example, if the unrecognized gain were $5,000, and the total unrecognized gain on all positions which offset the loss position was $10,000, then this fraction would be 1/2, or 0.50.

Dispositions to exclude

Don’t include in Part II a disposition of any of the following.

- A position that is part of a hedging transaction.

- A loss position included in an identified straddle established before October 22, 2004, unless you disposed of all of the positions making up the straddle.

- A loss position included in an identified straddle established after October 21, 2004.

- A position that is part of a straddle if all of the positions of the straddle are Section 1256 contracts.

Line 10

In Line 10, enter the following for each straddle disposition resulting in a loss:

- Column (a): Description of property

- Indicate whether this is a long position or short position

- Column (b): Date entered into position or date acquired

- Column (c): Date position closed out or sold

- Column (d): Gross sales price

- Column (e): Cost or other basis plus sales expense

- Include nondeductible interest and carrying charges allocable to personal property that is part of a straddle.

- If an unallowed loss from an offsetting position increased basis, include that amount

- Column (f): Loss

- If column (e) is more than (d), enter the difference. If not, enter ‘0.’

- Include any loss not allowed in the previous year to the extent of the unrecognized gain

- Column (g): Unrecognized gain on offsetting positions

- Column (h): Recognized loss

- If column (f) exceeds (g), enter the difference. Otherwise, enter ‘0.’

Line 11

There are two parts to Line 11:

- Line 11a: Short-term portion of losses

- Line 11b: Long-term portion of losses

Line 11a

Report any short-term losses here and on Line 4 of Schedule D, or on IRS Form 8949.

Line 11b

Report any long-term losses here and on Line 11 of Schedule D, or on IRS Form 8949.

Line 12

In Line 12, enter the following for each straddle disposition resulting in a gain:

- Column (a): Description of property

- Indicate whether this is a long position or short position

- Column (b): Date entered into position or date acquired

- Column (c): Date position closed out or sold

- Column (d): Gross sales price

- Column (e): Cost or other basis plus sales expense

- Include nondeductible interest and carrying charges allocable to personal property that is part of a straddle.

- If an unallowed loss from an offsetting position increased basis, include that amount

- Column (f): Gain

- If column (e) is more than (d), enter the difference. If not, enter ‘0.’

- Include any loss not allowed in the prior year to the extent of the unrecognized gain

Line 13

There are two parts to Line 13:

- Line 13a: Short-term portion of straddle gains

- Line 13b: Long-term portion of straddle gains

Line 13a

If you are not deferring any of this amount due to an investment in a QOF, report any short-term gains here and on Line 4 of Schedule D, or on IRS Form 8949.

If you are deferring any part of this amount due to a QOF investment, enter it in Part I of a Form 8949 with box C checked. Enter “Form 6781, Part II” on Line 1 in column (a). Enter the gain in column (h). Leave all other columns blank.

Line 13b

If you are not deferring any of this amount due to an investment in a QOF, report any long-term gains here and on Line 11 of Schedule D, or on IRS Form 8949.

If you are deferring any part of this amount due to a QOF investment, enter it in Part I of a Form 8949 with box F checked. Enter “Form 6781, Part II” on Line 1 in column (a). Enter the gain in column (h). Leave all other columns blank.

Collectibles

A collectibles gain or (loss) is any long-term gain or deductible long-term loss from the sale or exchange of a collectible that is a capital asset.

Collectibles include the following:

- Works of art

- Rugs

- Antiques

- Precious metals, such as gold, silver, and platinum

- Gems

- Stamps

- Coins

- Alcoholic beverages, and

- Certain other tangible property

If any of the gain or loss you reported in Part II is a collectibles gain or (loss), you’ll need to follow the instructions below, based on the form that you file.

IRS Form 1040 or Form 1040-SR

If you checked ‘Yes’ on Line 17 of Schedule D (Form 1040), include the collectibles gain (or loss) from Part II on Line 3 of the 28% Rate Gain Worksheet in the Schedule D instructions.

IRS Form 1041

If you must complete the 28% Rate Gain Worksheet in the Instructions for Schedule D (Form 1041), include the collectibles gain or (loss) from Part II on Line 3 of that worksheet.

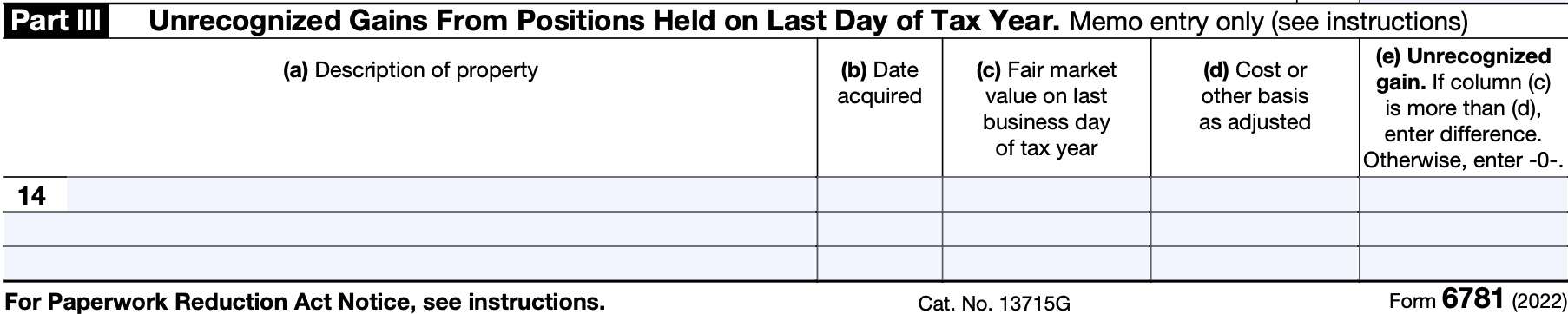

Part III: Unrecognized Gains From Positions Held on Last Day of Tax Year

Use Part III to list each position that you held on the last business day of the year, if the fair market value or market price of the position exceeds your cost basis or other basis as adjusted.

Do not include any of the following:

- Positions that are part of an identified straddle or hedging transaction

- Property that is stock in trade or inventory, or

- Property subject to depreciation that is used in a trade or business

Don’t complete Part III if you don’t have a recognized loss on any position, to include Section 1256 contracts.

Line 14

In Line 14, enter the following information for each position with unrecognized gains, whether or not it is part of a straddle:

- Column (a): Description of property

- Column (b): Date entered into position or date acquired

- Column (c): Market price or fair market value on the last business day of the tax year

- Column (d): Cost or other basis, as adjusted

- Column (e): Unrecognized gain

- If Column (c) exceeds Column (d), enter the difference. Otherwise, enter ‘0.’

Video walkthrough

Do you use TurboTax?

If you use TurboTax, and you’re completing this tax form for the first time, you might be ready to try TurboTax Federal Premium instead of the free or deluxe versions. TurboTax Federal Premium comes in two offerings, DIY or Live Assisted.

Do it yourself

To learn more about using TurboTax Federal Premium’s DIY option, click here.

Live Assisted

If you feel more comfortable having a tax expert guide you for the first time through this new form (or any other new forms), get started here.

Ready to hand the reins over to someone else completely? Go here to learn more about TurboTax’s Live Assisted Full Service offering!

Frequently asked questions

A Section 1256 contract can include any of the following: regulated futures contract, foreign currency contracts, nonequity option, dealer equity option, or dealer securities futures contracts.

A straddle position refers to offsetting positions of an actively traded security. For example, hedge funds may place both a call option and a put option on a traded security for loss protection purposes.

Taxpayers use IRS Form 6781 to report any capital gain or loss on Section 1256 contracts under the mark-to-market rules, and gains and losses under Section 1092 from straddle positions.

Under mark to market rules, each Section 1256 contract held at the end of the year is treated as if it were sold at fair market value (FMV) on the last business day of the tax year. The wash sales rules don’t apply for tax purposes. Gains and losses are treated as 40% short-term and 60% long-term, regardless of how long the contracts were actually held.

Where can I find IRS Form 6781?

You may find this IRS tax form on the Internal Revenue Service website. For your convenience, we’ve enclosed the latest version of IRS Form 6781 in this article.

Related tax articles

This tax form is one of the fillable tax forms provided by the Internal Revenue Service, to help taxpayers reduce their tax preparation costs. To see more forms like this, visit our free fillable tax forms page, where you’ll also find articles like this.

Unlike the IRS, our articles contain step by step instructions for each tax form, as well as video walkthroughs. You can also check out all of our videos by subscribing to our YouTube channel!