IRS Form 8453-CORP Instructions

If you’re a corporate officer who is electronically signing the corporation’s income tax return, you may be required to complete and sign IRS Form 8453-CORP, E-file Declaration for Corporations.

This article will walk you through what you should know about this tax form, including:

- What is IRS Form 8453-CORP

- How to complete this form and when you should file it

- Other versions of IRS Form 8453

- Filing considerations

Let’s start with discussing how to complete IRS Form 8453-CORP.

How do I complete IRS Form 8453-CORP?

There are three parts to this tax form, which we’ll go through, step by step:

- Part I: Information (Whole dollars only)

- Part II: Declaration of Officer

- Part III: Declaration of Electronic Return Originator (ERO) and Paid Preparer

However, let’s start at the very top of the form, above Part I. There, in the taxpayer information fields, enter the corporation’s name and employer identification number.

Let’s start with Part I.

Part I: Tax Return Information

Part I is relatively straightforward, as it only contains the total income amount from one of the following:

- IRS Form 1120, U.S. Corporation Income Tax Return

- IRS Form 1120-F, U.S. Income Tax Return of a Foreign Corporation, or

- IRS Form 1120-S, U.S. Income Tax Return for an S Corporation

You should only complete one line in Part I, depending on the type of income tax return your corporation is filing. Regardless of which line you complete, be sure to use whole dollars only.

Line 1: Total income (Form 1120, Line 11)

If you are filing an income tax return on behalf of a U.S. corporation, enter the total income amount from Line 11 on IRS Form 1120.

Line 2: Total income (Form 1120-F, Section II, Line 11)

International taxpayers filing on behalf of a foreign corporation will enter the total income figure from IRS Form 1120-F, Section II, Line 11.

Line 3: Total income (loss) (Form 1120-S, Line 6)

S corporations should report the total income as reported on Line 6 of IRS Form 1120-S. If the figure is a loss amount, enter this as a negative number.

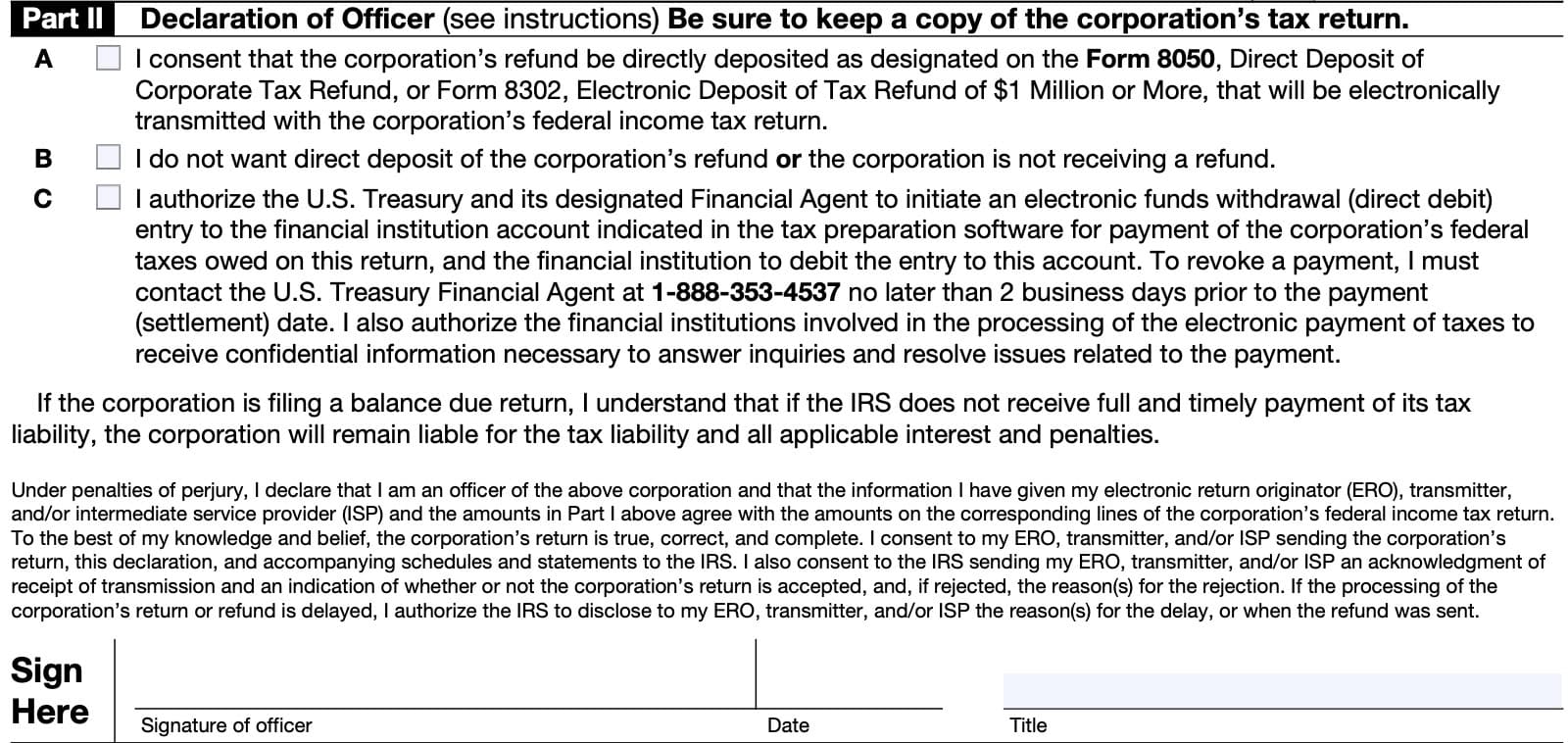

Part II: Declaration of Officer

In Part II, a corporate officer authorized by the corporation will sign, under penalty of perjury, that:

- The amounts listed above match the amounts shown on the associated tax return.

- The submitted information is true, correct, and complete, to the best of their knowledge

Additionally, this section contains the authorization for the U.S. Treasury to withdraw funds from the corporation’s bank account to pay any outstanding federal taxes.

The corporate officer must check all applicable boxes. Let’s take a closer look at each box.

Box A

By checking Box A, the corporation’s officer consents for any tax refund to be directly deposited as outlined on of the following tax forms that should accompany the corporation’s federal income tax return:

- IRS Form 8050, Direct Deposit of Corporate Tax Refund

- IRS Form 8302, Electronic Deposit of Tax Refund of $1 Million or More

Box B

By checking Box B, the corporate officer is stating either of the following:

- The corporation does not expect to receive a tax refund, or

- The corporation does not want the IRS to send the tax refund by direct deposit

Box C

If the officer checks Box C, this means the following:

- The corporation expects to owe income taxes for the current year, and

- Authorizes the U.S. Treasury to initiate the electronic funds withdrawal (known as direct debit) to the financial institution account indicated on the corporate tax return

If the corporate officer does not check Box C

In the case that the corporation has tax due and the officer did not check Box C, the corporation must make a timely payment using one of the authorized methods described in the tax return instructions.

If the corporate officer does check Box C

If the officer checks Box C to authorize a direct pay option, the officer must also ensure that the following

information relating to the financial institution account is provided in the tax preparation software:

- Routing number

- Account number

- Type of account

- Checking or savings

- Debit amount

- Debit date

Officer’s signature

At the bottom of Part II, the corporate officer must sign and date the form, and provide a title to indicate that he or she has the authority to make this tax declaration on the company’s behalf.

The IRS will not consider an electronically transmitted return to be considered complete unless either of the following occurs:

- IRS Form 8453-CORP is signed by a corporate officer, scanned into a PDF file, and transmitted with the corporate tax return; or

- The tax return is filed through an electronic return originator (ERO) and IRS Form 8879-CORP is used to select a PIN that is used to electronically sign the return.

Authorized disclosure

The officer’s signature allows the IRS to disclose to the ERO, transmitter, and/or ISP the following information:

- An acknowledgement that the IRS has accepted the corporation’s

electronically filed return, and - The reason(s) for any delay in processing the return or refund.

Additional corporate officer requirements

The declaration of officer must be signed and dated by:

- The president, vice president, treasurer, assistant treasurer, or chief accounting officer; or

- Another corporate officer authorized to sign the corporation’s income tax return

- Such as a tax officer

If the ERO makes changes to the electronic return after Form 8453-CORP has been signed by the officer, the ERO must have the officer complete and sign a corrected Form 8453-CORP if either of the following occurs:

- Total income differs from the amount on the electronic return by more than $150, or

- Taxable income differs from the amount on the electronic return by more than $100

This requirement applies whether it was before the tax return was transmitted or if the return was rejected after transmission.

Part III: Declaration of Electronic Return Originator (ERO) and Paid Preparer

In Part III, the ERO and paid tax return preparer declare that the submitted information is complete and correct, under penalty of perjury.

Difference between the ERO and paid preparer

There is a difference between an electronic return originator (ERO) and a paid preparer.

Paid preparer

A paid tax return preparer is anyone who is paid to prepare the estate’s or trust’s tax return. A paid preparer must enter their preparer tax identification number (PTIN) in the paid preparer only portion of Part III.

To receive a PTIN, a paid preparer must complete and submit IRS Form W-12, IRS Paid Preparer Tax Identification Number Application and Renewal to the Internal Revenue Service.

Electronic return originator (ERO)

The ERO is one who deals directly with the fiduciary and either prepares tax returns or collects prepared tax returns, including Forms 8453-FE, for fiduciaries who wish to have the return of the estate or trust electronically filed. The ERO’s signature is required by the IRS.

However, the ERO is not responsible for reviewing the return. The ERO is only responsible for ensuring that the information on Form 8453-FE matches the information on the tax return itself. Additionally, the ERO will give the fiduciary a copy of all forms and information submitted to the IRS.

If also the paid preparer, then the ERO is responsible for reviewing the return. If there is a separate paid tax return preparer, he or she must sign below.

ERO’s use only:

In this section, the ERO will provide:

- Signature & date

- Check if also the paid preparer

- ERO does not need to complete the paid preparer use only section, below

- Check if self-employed

- Social Security number or preparer tax identification number (PTIN)

- Firm’s name or ERO’s name, if self-employed

- Employer identification number (EIN)

- Phone number

Paid preparer use only:

In this section, the paid preparer will provide:

- Name

- Signature & date

- Check if self-employed

- PTIN

- Firm’s name

- Firm’s EIN

- Address

- Phone number

When complete, IRS Form 8453-CORP should accompany the corporate tax return.

Video walkthrough

Watch this video for a step-by-step walkthrough of IRS Form 8453-CORP.

Frequently asked questions

Taxpayers use IRS Form 8453-CORP to accompany a corporation’s electronically filed income

tax return, when filed by an intermediate service provider (ISP) or electronic return originator (ERO). Taxpayers also use this form to authorize electronic funds transfer for tax payments or refunds.

IRS Form 8453-CORP is used to submit an electronic corporate tax return through an intermediate service provider (ISP) without using an electronic return originator (ERO). IRS Form 8879-CORP allows the ERO to sign the return with an identity protection PIN number (IP PIN). An ERO may use either form.

Are you using the correct Form 8453?

According to the Internal Revenue Service website, there are 12 different versions of IRS Form 8453, including IRS Form 8453-CORP. Below is a brief summary of each of the 11 other IRS forms, and what each form does.

IRS Form 8453, U.S. Individual Income Tax Transmittal for an IRS e-file Return

Taxpayers use IRS Form 8453 to send required paper forms or supporting documentation that cannot be submitted to the Internal Revenue Service via electronic means.

Tax forms covered by IRS Form 8453

These include the following tax forms:

- IRS Form 1098-C, Contributions of Motor Vehicles, Boats, and Airplanes

- or equivalent contemporaneous written acknowledgement from the charitable organization

- IRS Form 2848, Power of Attorney and Declaration of Representative

- POA that states the agent is granted authority to sign the return

- IRS Form 3115, Application for Change in Accounting Method

- IRS Form 3468, Investment Credit

- Along with supporting documentation for historic preservation, such as NPS Form 10-168, Historic Preservation Certification Application or other certification as historic structure

- IRS Form 4136, Credit For Federal Tax Paid On Fuels

- Including appropriate certificates and appropriate reseller statements for biodiesel, renewable diesel, and sustainable aviation fuel claims (if applicable)

- IRS Form 5713, International Boycott Report

- IRS Form 8283, Noncash Charitable Contributions

- Section A-If any statement or qualified appraisal is required

- Section B-Donated Property, and any related attachments (including any qualified appraisal or partnership Form 8283)

- IRS Form 8332, Release/Revocation of Release of Claim to Exemption for Child by Custodial Parent

- Or certain pages from a divorce decree or separation agreement that went into effect after 1984 and before 2009

- IRS Form 8858, Information Return of U.S. Persons With Respect to Foreign Disregarded Entities (FDEs) and Foreign Branches (FBs)

- IRS Form 8864, Biodiesel and Renewable Diesel, or Sustainable Aviation Fuels Credit

- Including appropriate certificates and appropriate reseller statements for biodiesel, renewable diesel, and sustainable aviation fuel claims (if applicable)

- IRS Form 8949, Sales and Other Dispositions of Capital Assets

- If you elect not to report your transactions electronically on Form 8949

IRS Form 8453, U.S. Individual Income Tax Transmittal for an IRS e-file Return (Spanish)

Spanish version of the individual income tax transmittal tax form described above.

IRS Form 8453-EMP, Employment Tax Declaration for an IRS e-file Return

Taxpayers use IRS Form 8453-EMP to:

- Authenticate an electronic version of:

- IRS Form 940, Employer’s Annual Federal Unemployment (FUTA) Tax Return

- IRS Form 940-PR, Employer’s Annual Federal Unemployment (FUTA) Tax Return (Puerto Rico Version)

- IRS Form 941, Employer’s Quarterly Federal Tax Return

- IRS Form 941-PR, Employer’s Quarterly Federal Tax Return (Puerto Rico Version)

- IRS Form 941-SS, Employer’s Quarterly Federal Tax Return – American Samoa, Guam, the Commonwealth of the Northern Mariana Islands, and the U.S. Virgin Islands

- IRS Form 943, Employer’s Annual Federal Tax Return for Agricultural Employees

- IRS Form 943-PR, Employer’s Annual Federal Tax Return for Agricultural Employees (Puerto Rico Version)

- IRS Form 944, Employer’s Annual Federal Tax Return, or

- IRS Form 945, Annual Return of Withheld Federal Income Tax

- Authorize the ERO, if any, to transmit via a third-party transmitter

- Authorize the intermediate service provider (ISP) to transmit via a third-party transmitter if filing online without using an ERO, and

- Provide taxpayer’s consent to authorize an electronic funds transfer for payment of federal taxes owed

IRS Form 8453-FE, Estate/Trust Declaration for IRS e-file Return

Taxpayers use IRS Form 8453-FE to:

- Authenticate the electronic Form 1041, U.S. Income Tax Return for Estates and Trusts;

- Authorize the electronic filer to transmit via a third-party transmitter; and

- Authorize an electronic funds withdrawal for payment of federal taxes owed.

IRS Form 8453-EX, Excise Tax Declaration for an IRS e-file Return

Taxpayers use IRS Form 8453-EX to:

- Authenticate electronic versions of the following forms:

- IRS Form 720, Quarterly Federal Excise Tax Return

- IRS Form 2290, Heavy Highway Vehicle Use Tax Return

- IRS Form 8849, Claim for Refund of Excise Taxes

- Authorize the ERO, if any, to transmit via a third-party transmitter

- Authorize the ISP to transmit via a third-party transmitter if filing online without an ERO

- Provide taxpayer’s consent for electronic funds withdrawal to pay taxes owed

IRS Form 8453-PE, U.S. Partnership Declaration for an IRS e-file Return

Partnerships use this tax form to:

- Authenticate an electronic Form 1065, U.S. Return of Partnership Income, as part of return or administrative adjustment request (AAR)

- Authorize the ERO, if any, to transmit via a third-party transmitter

- Authorize the ISP to transmit via a third-party transmitter if filing online (not using an ERO).

IRS Form 8453-R Declaration and Signature for Electronic Filing of Form 8963

Taxpayers use IRS Form 8453-R to authenticate the electronic filing of IRS Form 8963, Report of Health Insurance Provider Information.

IRS Form 8453-S, U.S. S Corporation Income Tax Declaration for an IRS e-file Return

U.S. S-corporations use this tax form to:

- Authenticate an electronic Form 1120-S, U.S. Income Tax Return for an S-Corporation

- Authorize the ERO, if any, to transmit via a third-party transmitter

- Authorize the ISP to transmit via a third-party transmitter if filing online (not using an ERO)

- Provide the corporation’s consent to directly deposit any refund into a bank account and/or authorize a direct debit for payment of federal taxes owed

Tax years 2022 and beyond

For tax years 2022 and later, IRS Form 8453-CORP has replaced IRS Form 8453-S.

IRS Form 8453-TE, Tax Exempt Entity Declaration and Signature for Electronic Filing

Tax-exempt entities use this tax form to:

- Authenticate one of the following tax forms:

- IRS Form 990, Return of Organization Exempt From Income Tax

- IRS Form 990-EZ, Short Form Return of Organization Exempt From Income Tax

- IRS Form 990-PF, Return of Private Foundation

- IRS form 990-T, Exempt Organization Business Income Tax Return

- IRS Form 1120-POL, U.S. Income Tax Return for Certain Political Organizations

- IRS Form 4720, Return of Certain Taxes Under Chapters 41 and 42 of the Internal Revenue Code

- IRS Form 8868, Application for Automatic Extension of Time To File an Exempt Organization Return

- IRS form 5227, Split-Interest Trust Information Return

- IRS Form 5330, Return of Excise Taxes Related to Employee Benefit Plans, and

- IRS Form 8038-CP, Return for Credit Payments to Issuers of Qualified Bonds

- Authorize the ERO, if any, to transmit via a third-party transmitter

- Authorize the intermediate service provider (ISP) to transmit via a third-party transmitter if filing online without using an ERO

- Authorize an electronic funds withdrawal for payment of federal taxes owed as determined by one of the following:

- IRS Form 990-PF

- IRS Form 990-T

- IRS Form 1120-POL

- IRS Form 4720

- IRS Form 5330

- IRS Form 8868

IRS Form 8453-WH, Electronic Filing Declaration for Form 1042

Taxpayers use IRS Form 8453-WH to:

- Authenticate an electronic Form 1042, Annual Withholding Tax Return for U.S. Source Income of Foreign Persons;

- Provide consent to authorize an electronic funds withdrawal for payment of the balance due on IRS Form 1042

- Authorize the intermediate service provider (ISP) to transmit via a third-party transmitter if you are filing online (not using an ERO); and

- Authorize the ERO, if any, to transmit via a third-party transmitter

IRS Form 8453-X Political Organization Declaration for Electronic Filing of Notice of Section 527 Status

After electronically submitting IRS Form 8871, Political Organization Notice of Section 527 Status, an authorized official must sign, date, and send this form to the Internal Revenue Service.

This allows the political organization to:

- File an amended or final Form 8871, or

- To electronically file Form 8872, Political Organization Report of Contributions and Expenditures.

Where do I find a copy of IRS Form 8453-CORP?

You can find IRS forms, such as IRS Form 8453-CORP, on the Internal Revenue Service website. For your convenience, we’ve