IRS Form 8611 Instructions

The Internal Revenue Code allows certain tax credits for people and businesses who invest in low-income housing projects. However, if you take the credit and sell the property before the end of its recapture period, then you may need to calculate the recapture amount on IRS Form 8611, Recapture of Low-Income Housing Credit.

In this article, we’ll walk you through IRS Form 8611, including:

- How to complete the tax form

- How the recapture tax works

- Other frequently asked questions

Let’s begin by going over this form, step by step.

Table of contents

How do I complete IRS Form 8611?

This one-page tax form is fairly simple to complete. But before beginning the form, it’s important to make sure you’ve got everything that you need.

Before you begin IRS Form 8611

You will need certain information from other tax forms you may have previously filed. Make sure you have access to the following forms that you might have filed in prior years:

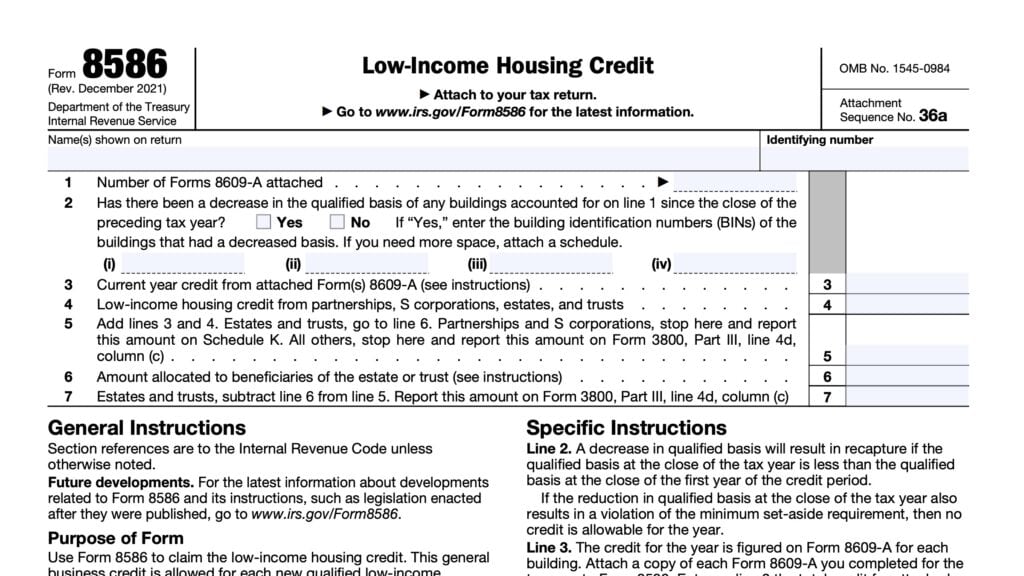

- IRS Form 8586, Low-Income Housing Credit

- IRS Form 3800, General Business Credit

- IRS Form 8609, Low-Income Housing Credit Allocation

- Previously known as Low-Income Housing Credit Allocation Certification

- IRS Form 8609-A, Annual Statement for Low-Income Housing Credit

- Previously known as Schedule A on IRS Form 8609

- IRS Form 8611 from previous years

Additional note

Please note: you will have to file IRS Form 8611 for each low-income building for which you are calculating a recapture amount.

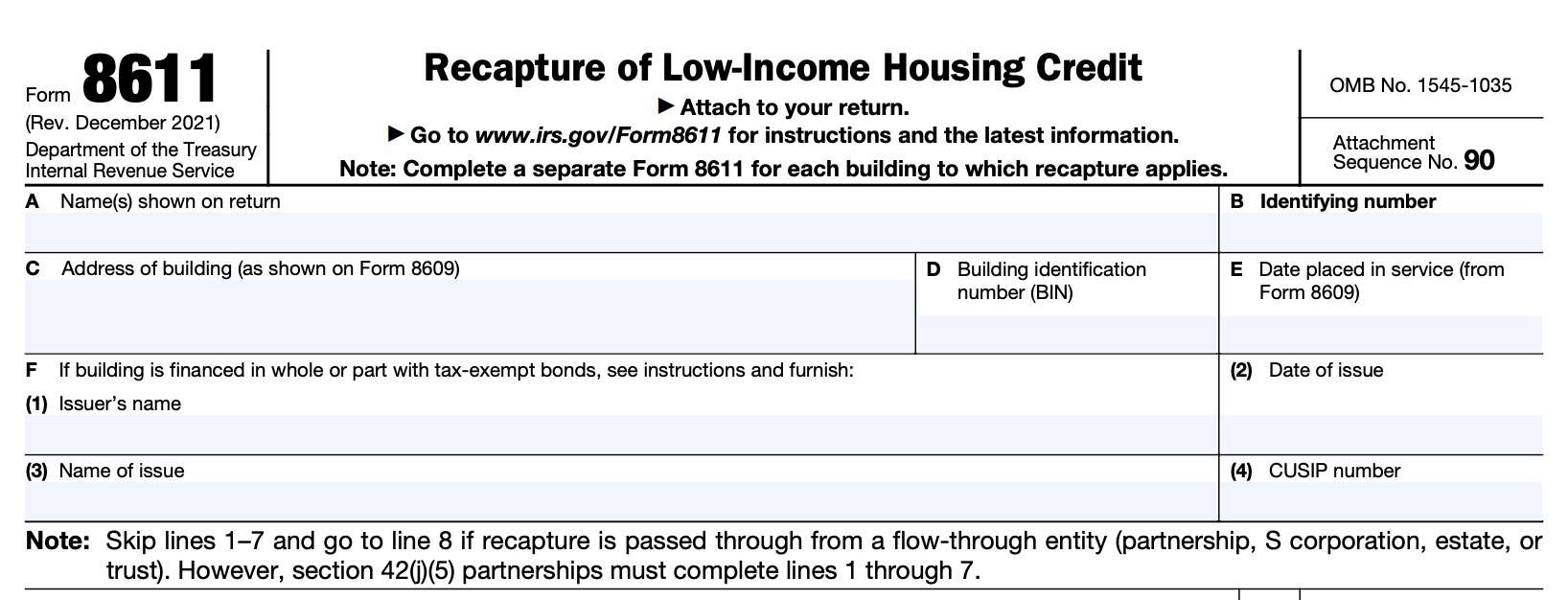

Now that we have the required tax forms, let’s start at the top of IRS Form 8611 with Item A.

Item A: Name(s) shown on return

Enter the taxpayer name (or names, for married taxpayers filing a joint return) as shown on the income tax return.

Item B: Identifying number

Enter the identifying number as shown on the tax return. For individual taxpayers, this will probably be a Social Security number.

For corporate entities, estates, and trusts, this will be the employer identification number (EIN).

Item C: Address of building

Enter the address of the low-income building that this form applies to. This should match the address of the building as shown on the copy of IRS Form 8609 that you previously submitted.

Item D: Building identification number

Enter the building identification number (BIN) as assigned by the appropriate housing credit agency.

Item E: Date placed in service

Enter the date that the low-income building was placed into service, as documented in the previously filed Form 8609.

Item F

If the building was not financed with tax-exempt bonds, then skip this section and go to Line 1, below.

Otherwise, enter the following information in the corresponding numbered line:

- Name of the entity that issued the bond

- Do not enter the name of the entity receiving the financing benefit

- Date of issue

- This generally is the first date where there is a physical exchange of the bonds for the purchase price

- Name of the issue, or other identification of the issue

- CUSIP number of the tax-free bond with the latest maturity date

- Enter ‘None’ if the issue does not have a CUSIP number

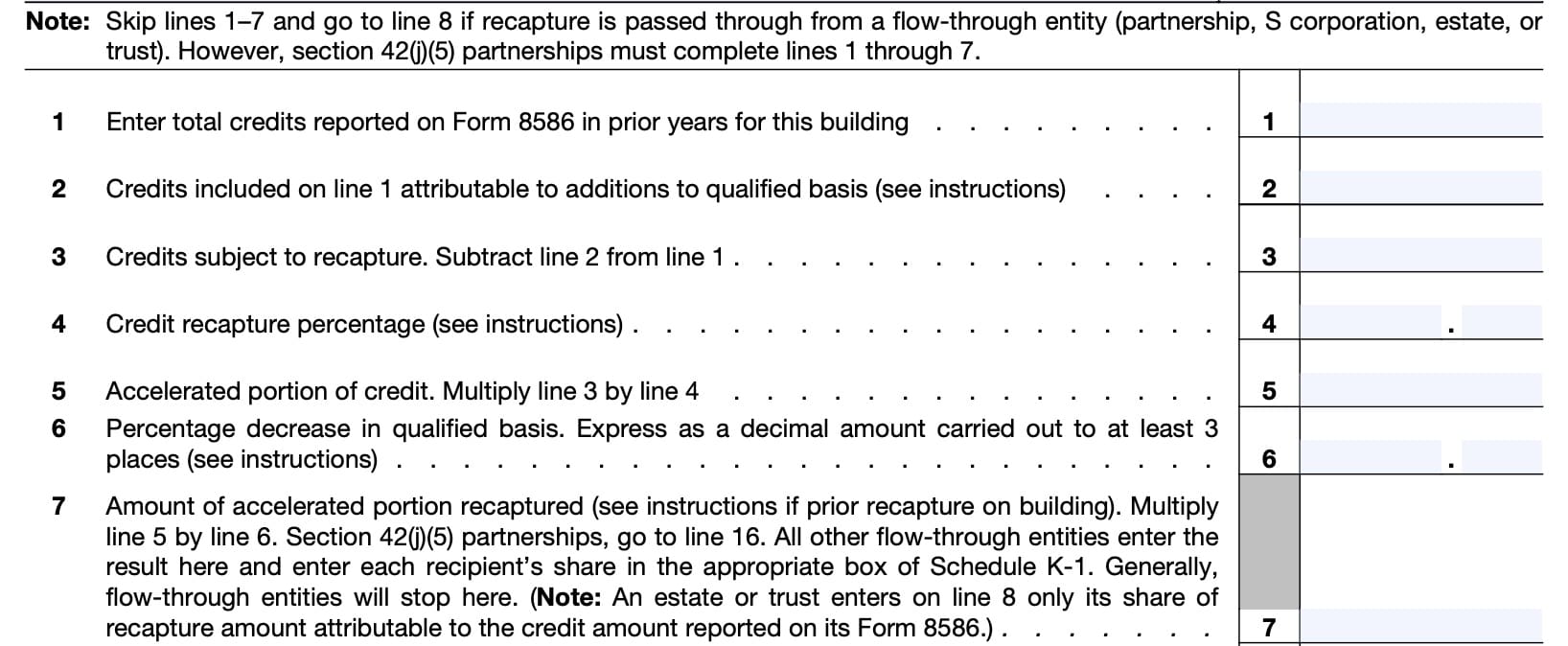

If the recapture is from a pass-through entity, such as a partnership, S corporation, estate, or trust, then skip Lines 1 through 7 and start on Line 8.

The primary exception is Section 42(j)(5) partnerships, which are treated as the taxpayer for recapture purposes. Section 42(j)(5) partnerships must begin on Line 1.

Other taxpayers, such as individual taxpayers and non pass-through entities, can begin on Line 1, below.

Line 1

In Line 1, enter the total tax credits claimed on the building for all prior years from all Forms 8586 that you have filed, before reduction due to the tax liability limit.

Do not include tax credits that were claimed by a previous owner.

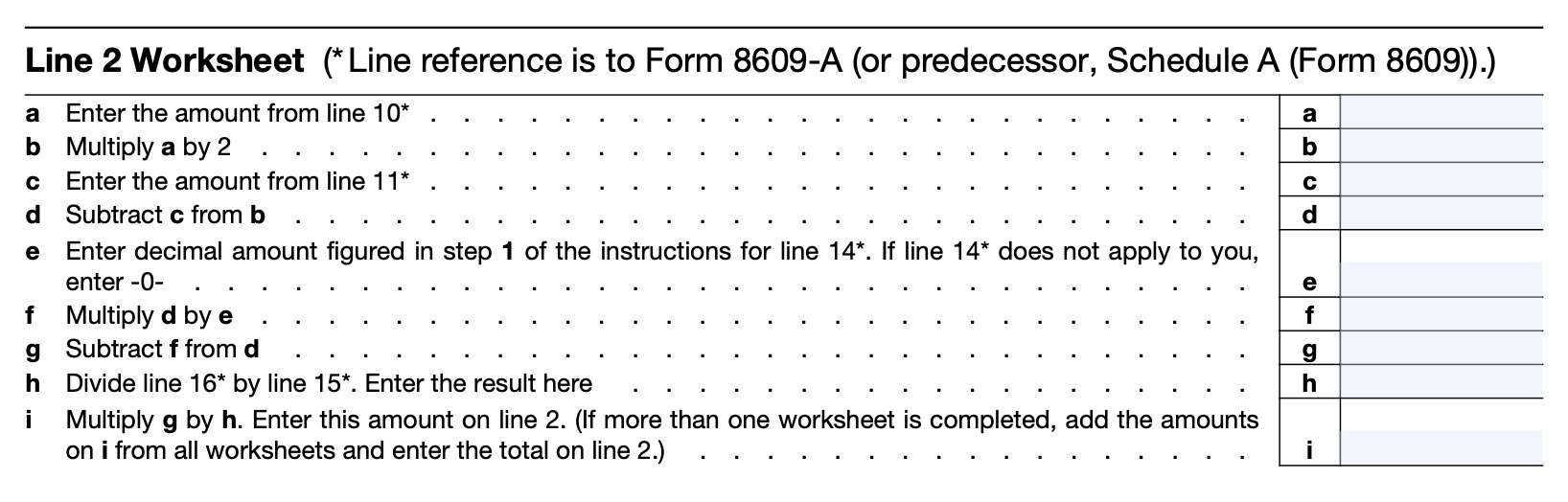

Line 2

Enter the Line 1 credits that were attributable to additions to the building’s qualified basis. To calculate this amount, you’ll need to complete a separate version of the Line 2 worksheet (see below) for each prior year in which IRS Form 8609-A or IRS Form 8609, Schedule A were completed.

Line 3: Credits subject to recapture.

Subtract Line 2 from Line 1, then enter the result here.

This represents the portion of the credit subject to recapture.

Line 4: Credit recapture percentage

Enter the applicable credit recapture percentage, from the table below.

| If the recapture event occurs in | Then enter the following on Line 4 |

| Years 2 through 11 | .333 |

| Year 12 | .267 |

| Year 13 | .200 |

| Year 14 | .133 |

| Year 15 | .067 |

Line 5: Accelerated portion of credit

Multiply Line 3 by the credit recapture percentage in Line 4. Enter the result in Line 5.

Line 6: Percentage decrease in qualified basis

For this purpose, figure qualified basis without regard to any additions to qualified basis after the first year of the credit period.

Compare any decrease in qualified basis first to additions to qualified basis. Recapture applies only if the decrease in qualified basis exceeds additions to qualified basis after the first year of the credit period.

If you disposed of the building or an ownership interest in it and did not satisfy the requirements for avoiding recapture as outlined below under Building Dispositions, you must recapture all of the accelerated portion shown on Line 5.

Enter 1.000 on Line 6.

Minimum set-aside requirements

If the decrease causes the qualified basis to fall below the minimum set-aside requirements of Internal Revenue Code Section 42(g)(1), then the entire credit amount shown in Line 5 must be recaptured.

These set aside requirements can be any of the following:

- 20-50 Test: At least 20 percent of the residential units in the project must be both rent-restricted and occupied by tenants whose gross income is 50 percent or less of the area median gross income (AMGI)

- 40-60 Test: At least 40 percent of the residential units in the project must be both rent-restricted and occupied by tenants whose gross income is 60 percent or less of AMGI

- Average income test: A project meets the minimum requirements of the average income test if 40 percent or more of the residential units in the project are both rent-restricted and occupied by tenants whose income does not exceed the imputed income limitation designated by the taxpayer with respect to the specific unit.

If you elected the 40-60 test for this building and the decrease causes you to fall below 40%, you cannot switch to the 20-50 test or the average income test to meet the set-aside requirements.

Enter 1.000 on Line 6 if the qualified basis of the building falls below the minimum set-aside requirements.

Building dispositions

Disposing of a building or an interest therein will generate a credit recapture, unless you reasonably expect that the new owner will continue to operate the building as a qualified low-income building for the remainder of the building’s 15-year compliance period.

Line 7: Amount of accelerated portion recaptured

Multiply Line 5 by Line 6. Section 42(j)(5) partnerships will go to Line 16 at the bottom of this form.

All other flow-through entities enter the result here, then enter each recipient’s share in the appropriate box of Schedule K-1.

Generally, flow-through entities will stop here. However, an estate or trust may need to complete Line 8 to report its share of recapture amount attributable to the credit amount reported on its previously filed Form 8586.

If there was a prior recapture of accelerated credits on the building, do not recapture that amount again as the result of the current reduction in qualified basis.

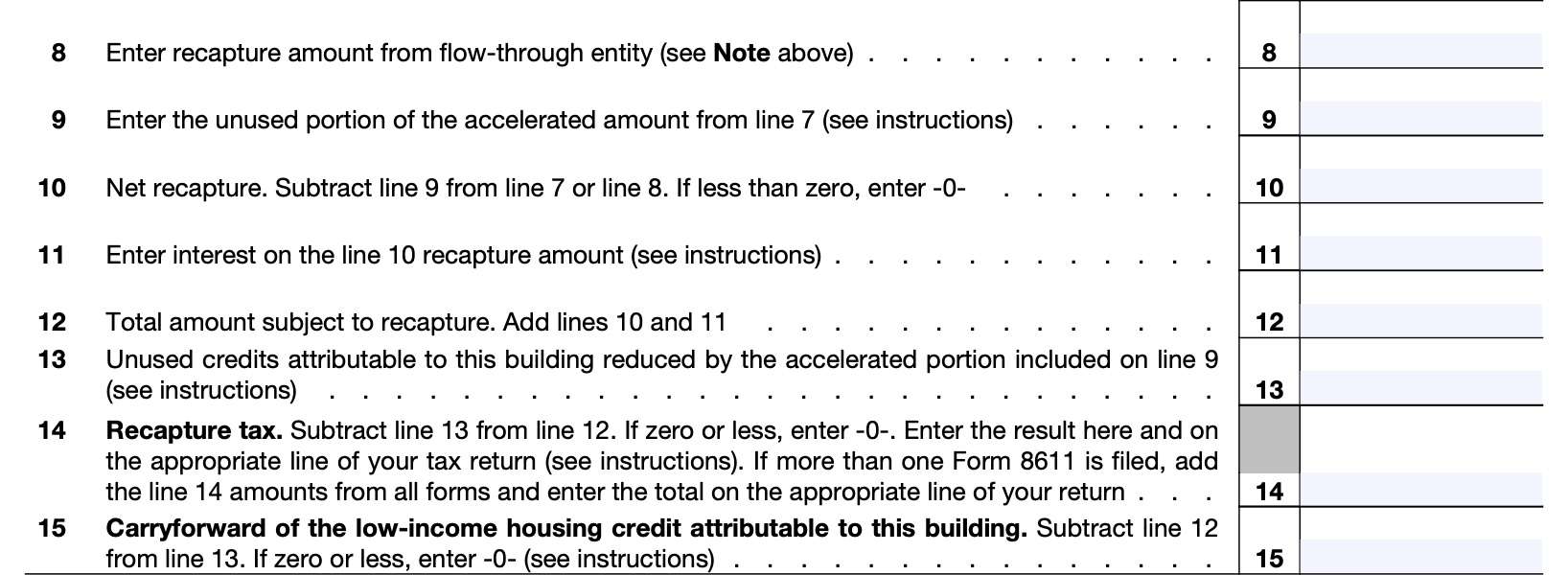

Line 8: Recapture amount from flow-through entity

Estates and trusts enter any recapture amount attributable to the rehabilitation credit previously claimed on IRS Form 8586.

Line 9: Unused portion of Line 7 accelerated amount

To calculate the unused portion of the Line 7 accelerated amount, follow these steps:

- Total the credits attributable to the building that you could not use in prior tax years

- Usually, this is the amount of credit reported on Line 1 of this Form 8611 reduced by the total low income housing credits allowed on IRS Form 8586 or IRS Form 3800 for each taxable year

- Reduce this amount by any unused credits attributable to additions to qualified basis

- Multiply this amount by the Line 4 decimal amount

- Multiply the result by the Line 6 amount

- Enter this number into Line 9

Line 10: Net recapture

Subtract Line 9 from either Line 7 or Line 8. If this results in zero or a negative number, enter ‘0.’

Line 11

You’ll have to separately calculate the interest for each prior tax year for which you are recapturing a tax credit. You must use the overpayment rate determined under IRC Section 6621(a)(1), and compound the interest daily from the original tax return due date until the earlier of:

- The due date, not including extensions, of the tax return for the recapture year, or

- The date that you file the return for the recapture year and pay the income tax due in full

The interest rates in effect through December 31, 2019, were published by the Internal Revenue Service in Rev. Rul. 2019-21, 2019-38 I.R.B. 708. For periods after December 31, 2019, use the overpayment rates that the IRS publishes quarterly in the Internal Revenue Bulletin.

Section 42(j)(5) Partnership

If the Line 8 recapture amount is from a Section 42(j)(5) partnership, the partnership will figure the interest and include it in the recapture amount reported to you.

In this situation, enter ‘0’ on Line 11, then write “Section 42(j)(5)” to the left of the Line 11 entry space.

Line 12: Total amount subject to recapture

Add Line 10 and Line 11. The result is the amount of rehabilitation credit subject to recapture.

Line 13

Subtract the Line 9 amount from the total of all prior year unused credits attributable to the building, located on Step 1 of the Line 9 instruction above. Enter the result here.

Line 14: Recapture tax

Subtract Line 13 from Line 12. If this results in a negative number, enter ‘0.’

This represents the amount of recapture tax you owe. Enter this amount on Line 14 and on the appropriate line of your income tax return.

If you filed more than one Form 8611, add the Line 14 amounts from all completed forms. Enter the total amount on the appropriate line of your tax return.

Form 1040, 1040-SR, and 1040-NR filers

Report the recapture tax on IRS Schedule 2 (Form 1040), Line 16.

Form 1120 filers

Report the recapture tax on IRS Form 1120, Schedule J, Line 9b.

Line 15: Carryforward of the low-income housing credit attributable to this building

If you don’t have a recapture tax, you might have a tax credit carryforward.

Carry forward the low-income housing credit attributable to this building to the next tax year on IRS Form 3800. See the Instructions for Form 3800 to learn more about how to report the carryforward of unused credits.

If you are a Section 42(j)(5) partnership, you need to complete Lines 16 and 17, below. Otherwise, you have completed IRS Form 8611.

Line 16

Using the Line 11 instructions, calculate the total interest on Line 16.

The partnership must attach IRS Form 8611 to its tax return, then allocate this amount to each partner on Schedule K-1 in the same manner that the partnership allocates taxable income to each partner.

Line 17

Add Line 7 and Line 16, then enter the result here.

This represents the total recapture for a Section 42(j)(5) partnership.

When recapture does not apply

According to the Internal Revenue Service, recapture does not apply in any of the following situations:

- You disposed of the building or an ownership interest in the building and you satisfy the requirements for avoiding recapture;

- You disposed of an ownership interest in a building you held through a partnership to which IRC Section 42(j)(5) applies;

- Recapture occurs at the partnership level

- The decrease in qualified basis does not exceed the additions to qualified basis for which credits were allowable in years after the first year of the credit period; or

- The qualified basis is reduced because of a casualty loss, provided the property is restored or replaced within a reasonable period.

Video walkthrough

Watch this informative video to learn step by step instructions on how to calculate the recapture of your low-income housing credit on IRS Form 8611.

Frequently asked questions

Taxpayers use this form if you must recapture part of the low-income housing credit claimed in previous years because the qualified basis decreased or the taxpayer disposed of a building, or their interest in a building, and they did not follow the procedures that would have prevented recapture of the credit.

Generally, there is a 15-year compliance period for the rehabilitation tax credit.

Where can I find IRS Form 8611?

You can find IRS Form 8611 on the IRS website. For your convenience, we’ve attached the latest version of this tax form to this article.

Related tax articles

This tax form is one of the fillable tax forms provided by the Internal Revenue Service, to help taxpayers reduce their tax preparation costs. To see more forms like this, visit our free fillable tax forms page, where you’ll also find articles like this.

Unlike the IRS, our articles contain step by step instructions for each tax form, as well as video walkthroughs. You can also check out all of our videos by subscribing to our YouTube channel!