IRS Form 8615 Instructions

How do I complete IRS Form 8615?

We’ll walk through this one-page tax form, step by step. There are 3 parts, not including the taxpayer information fields at the top of the form:

- Part I: Child’s Net Unearned Income

- Part II: Tentative Tax Based on the Tax Rate of the Parent

- Part III: Child’s Tax

Let’s start at the top with the taxpayer information fields.

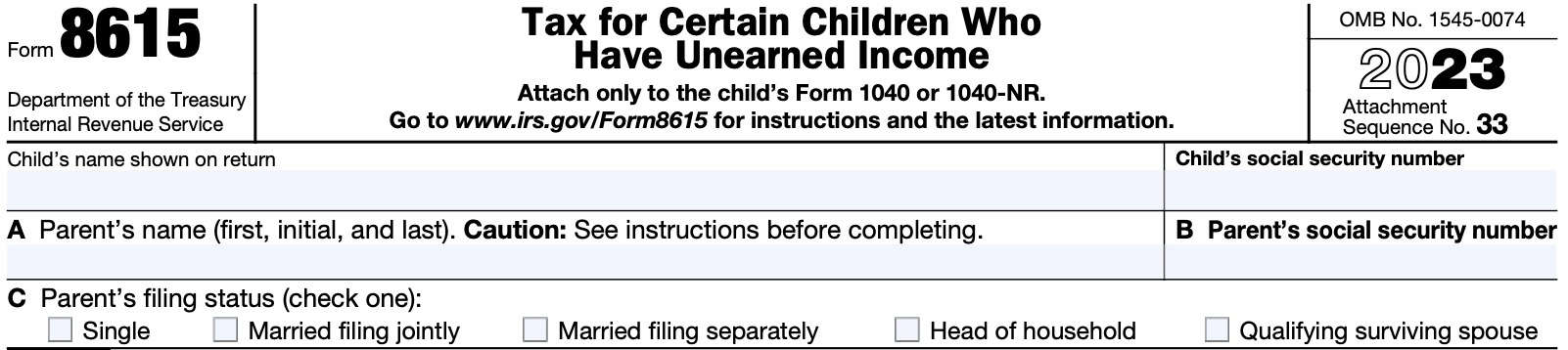

Taxpayer information

Before you begin, please note that IRS Publication 929, Tax Rules for Children and Dependents, has special considerations for people in the following situations:

- Either the child, parent, or other children in the household must use the Schedule D Tax Worksheet. You can find this worksheet on page D-16 of the Schedule D instructions.

- The child has income from farming or fishing

At the top of the tax form, enter the child’s name and Social Security number. This should match how the child’s information appears in the parent’s return.

For Lines A-C, please follow the instructions below.

Line A: Parent’s name

If the child’s parents are married and filing a joint return, enter the name and the SSN of the parent listed first on the joint Form 1040.

If the child’s parents are married and filing separate returns, enter the name and SSN of the parent with the higher taxable income.

For unmarried parents, enter the name and SSN of the parent with whom the child resided for the greater part of the calendar year. If the unmarried parents lived together, enter the name and SSN of the parent with the greater taxable income.

Line B: Parent’s Social Security Number

Enter the Social Security number belonging to the parent named in Line A.

Line C: Filing status

Select one of the following tax filing statuses:

- Single

- Married filing jointly

- Married filing separately

- Head of household

- Qualifying surviving spouse

Let’s proceed to Part I.

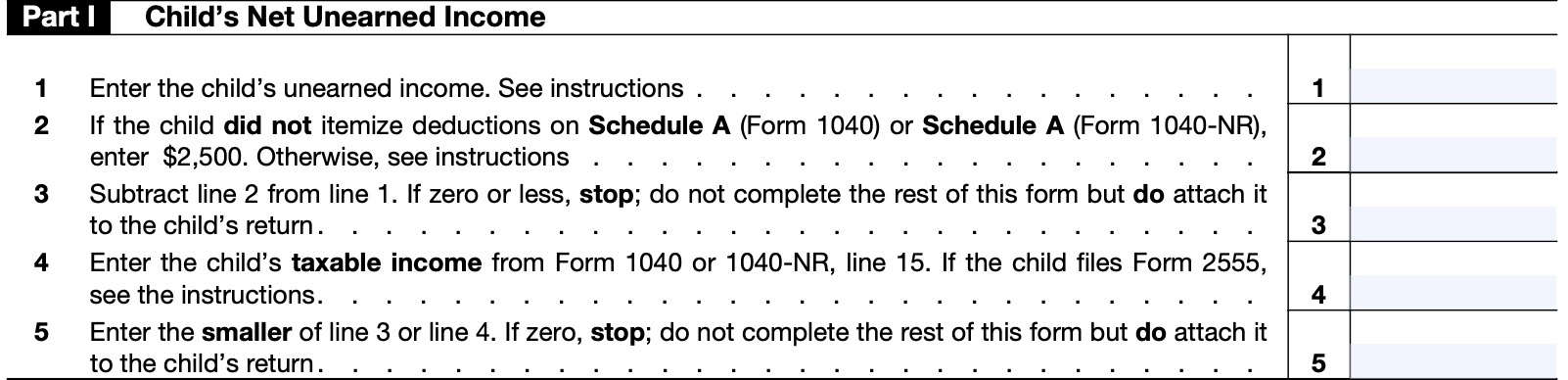

Part I: Child’s Net Unearned Income

In Part I, we’ll calculate the child’s net unearned income.

Line 1

Enter the child’s unearned income during the tax year. If the child had no earned income, enter the amount from Line 11 of the Form 1040 or Form 1040-NR.

Child’s unearned income worksheet

If the child had earned income, you may need to use the child’s unearned income worksheet (see below) to calculate the amount to enter on Line 1. This worksheet will help you arrive at unearned income by subtracting earned income from total income.

Refer to Publication 929 instead of the worksheet to figure the amount to enter on Line 1 if the child:

- Files IRS Form 2555, Foreign Earned Income

- Has a net loss from self-employment, or

- Claims a net operating loss deduction

Line 2

The amount that you enter into Line 2 depends on whether itemizes tax deductions on Schedule A.

If the child did not itemize deductions using Schedule A, enter $2,500.

If the child did itemize deductions on Schedule A, then enter the larger of:

- $2,500; or

- $1,250 plus the portion of the total itemized deductions directly connected with producing the unearned income reported on Line 1. You’ll find this on either:

- Schedule A (Form 1040), Line 17, or

- Schedule A (Form 1040-NR), Line 8

Line 3

Subtract Line 2 from Line 1 and enter the total. If this is zero or a negative number, do not continue. Attach the form to the child’s tax return.

If this result is positive, continue to Line 4.

Line 4

Enter the child’s taxable income. You’ll find this on Line 15 of Form 1040 or Form 1040-NR.

If the child files IRS Form 2555, enter the amount from Line 3 of the child’s Foreign Earned Income Tax Worksheet, instead. You’ll find this worksheet in the IRS Form 1040 or Form 1040-NR instructions.

Line 5

Enter the smaller of either Line 3 or Line 4. If zero, stop.

Attach the form to the child’s return, but do not continue.

If positive, continue to Part II.

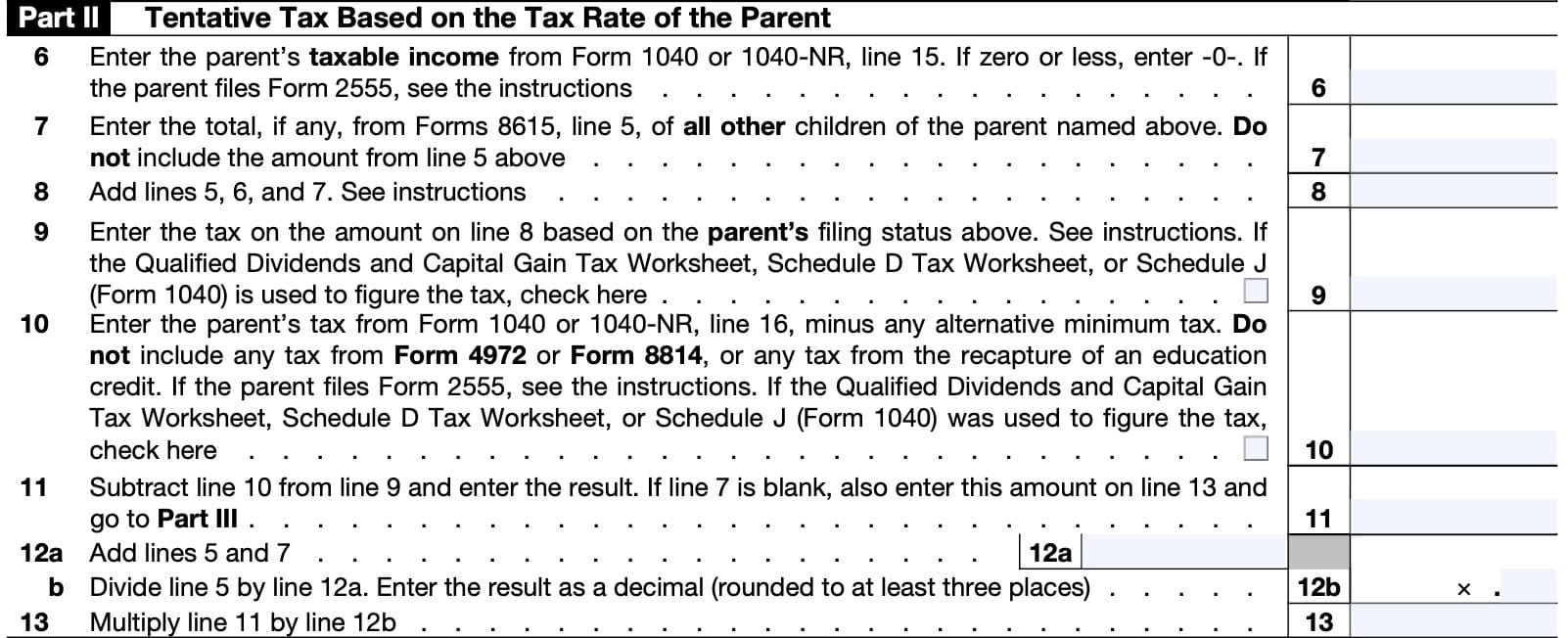

Part II: Tentative Tax Based on the Tax Rate of the Parent

In Part II, we’ll calculate the tentative tax based upon the parent’s tax rate.

Line 6

Enter the parent’s taxable income. You’ll find this on IRS Form 1040 or 1040-NR, Line 15.

If zero or less, enter ‘0.’ If the parent filed a joint return, enter the taxable income shown on that return even if the parent’s spouse isn’t the child’s parent.

If the parent filed IRS Form 2555, enter the amount from Line 3 of the parent’s Foreign Earned Income Tax Worksheet, instead of the parent’s taxable income.

Line 7

Enter the total of Forms 8615 for all other children of the parent listed above. Do not include the amount from Line 5 of this Form 8615.

Line 8

Add Lines 5, 6, and 7.

However, you’ll need to determine the amount of qualified dividends and net capital gains included on Line 8 before calculating the tax on Line 9 below.

If you believe qualified dividends or net capital gains apply, special instructions may apply.

Net capital gain and qualified dividends on Line 8

No net capital gain: If neither the child, nor the parent, nor any other child has net capital gain, the net capital gain on Line 8 is zero.

Zero qualified dividends: If neither the child, nor the parent, nor any other child has qualified dividends, the amount of qualified dividends on Line 8 is zero.

Net capital gain: If the child, the parent, or any other child has net capital gain, figure the amount of net capital gain included on Line 8 by adding together the net capital gain amounts included on Lines 5, 6, and 7.

Qualified dividends: If the child, the parent, or any other child has qualified dividends, figure the amount of qualified dividends included on Line 8 by adding together the qualified dividend amounts included on Lines 5, 6, and 7.

You can use the following guidelines to determine these amounts.

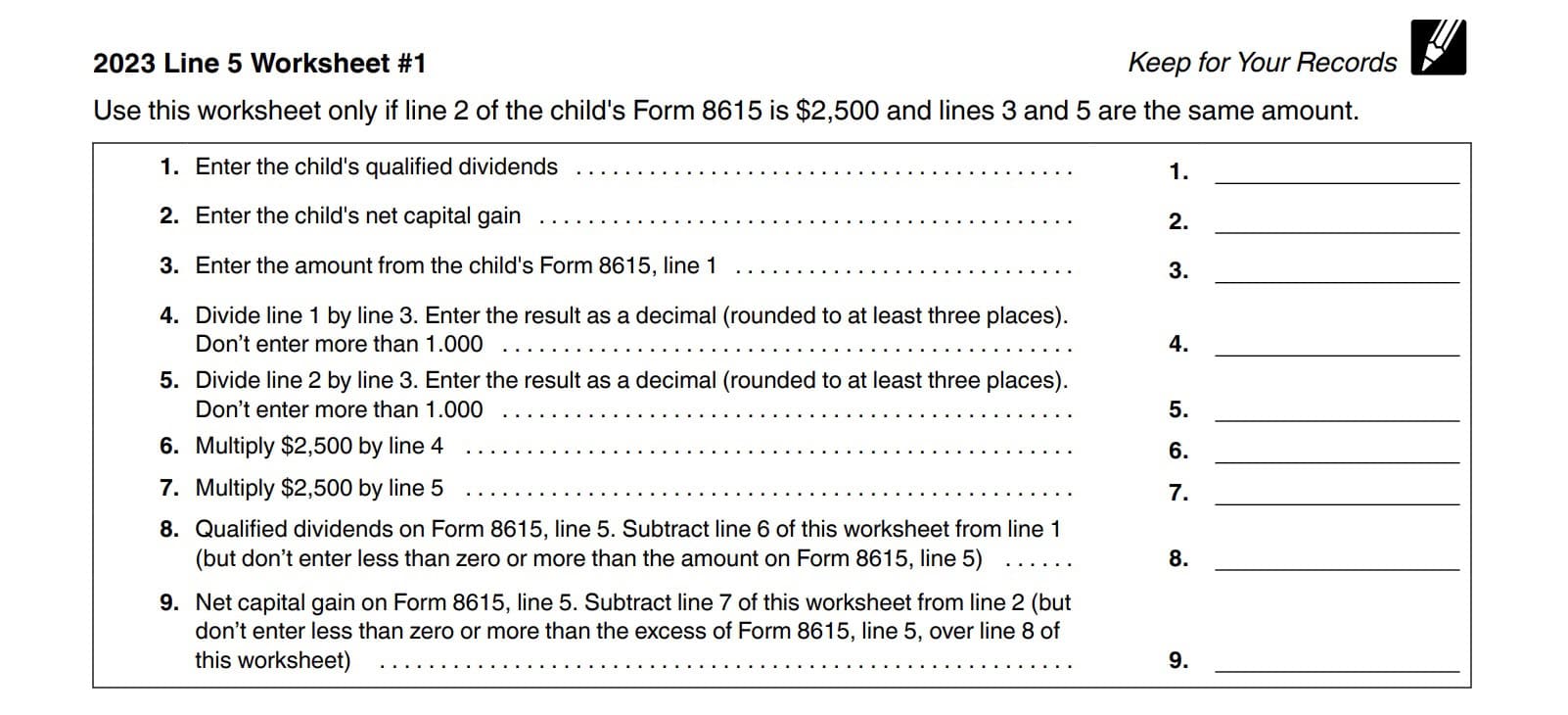

Net capital gain or qualified dividends on Line 5

If the child has a net capital gain or qualified dividends, use the appropriate Line 5 Worksheet in these instructions to find the amount included on Line 5.

Worksheet 1

Use Worksheet 1 to calculate the child’s Line 5 amount if:

- Line 2 on the child’s Form 8615 is $2,500, and

- Line 3 and Line 5 are the same amount

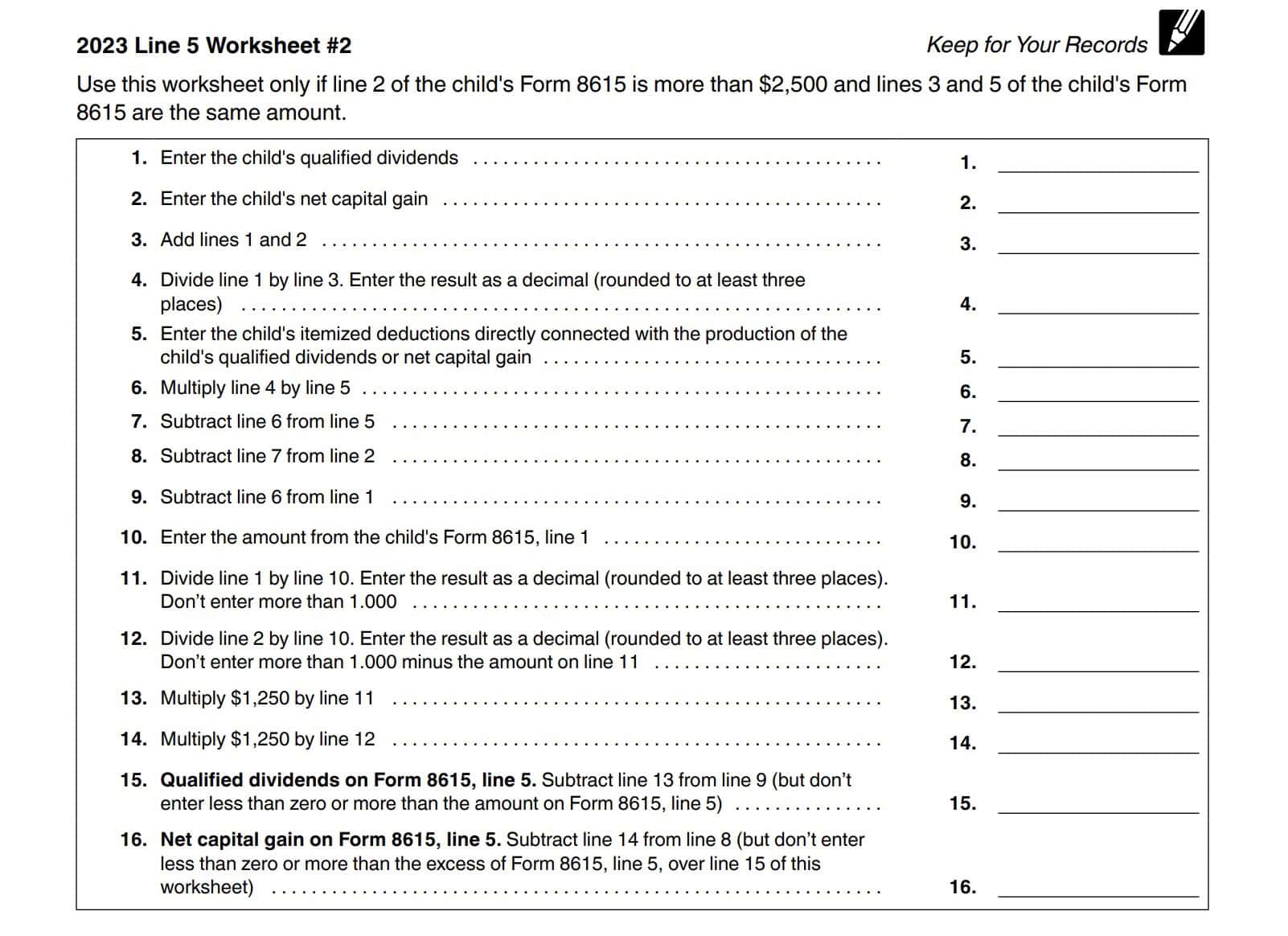

Worksheet 2

Use Worksheet 2 to calculate the child’s Line 5 amount if:

- Line 2 on the child’s Form 8615 is more than $2,500, and

- Line 3 and Line 5 are the same amount

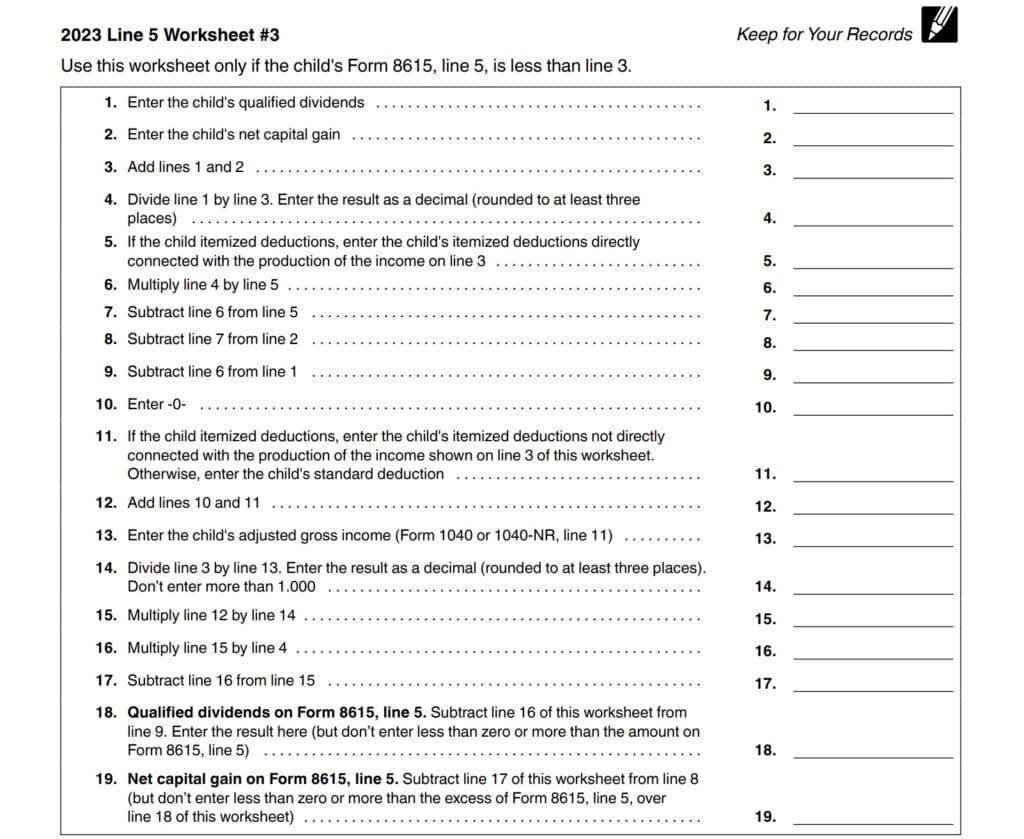

Worksheet 3

Use Worksheet 2 to calculate the child’s Line 5 amount if Line 5 is less than Line 3.

These worksheets will adjust the child’s net capital gain and qualified dividends by the appropriate allocated amount of the child’s deductions.

Net capital gain or qualified dividends on Line 6

If the parent has a net capital gain, its full amount is the net capital gain included on Line 6. If the parent has qualified dividends, the full amount is the amount of qualified dividends included on Line 6.

Net capital gain or qualified dividends on Line 7

The net capital gain included on line 7 is the total of the amounts of net capital gain included on line 5 of the other children’s Forms 8615.

Note: The amount of any net capital gain or qualified dividends isn’t separately reported on Line 8. It is needed, however, when figuring the tax on Line 9.

Line 9

Enter the tax on the Line 8 amount based upon the parent’s filing status. If you use any of the following, check the appropriate box under Line 9:

- Qualified Dividends and Capital Gain Tax Worksheet

- Schedule D Tax Worksheet

- Schedule J

Line 10

Enter the amount from Line 16 on the parent’s Form 1040 or Form 1040-NR, minus any alternative minimum tax. If this is a joint return, use that number, even if the other spouse isn’t the child’s parent.

Do not include any tax from the following:

- IRS Form 4972, Lump-Sum Distributions

- IRS Form 8814, Parent’s Election to Report Child’s Interest and Dividends

- Recapture of an education credit calculated on IRS Form 8863

For parents filing Form 2555, use the number on Line 4 instead of the tax from the parent’s tax return. If you checked the box in Line 9, check the box in Line 10.

Line 11

Subtract Line 10 from Line 9.

If Line 7 is blank, then enter this amount on Line 13 as well, then proceed to Part III.

Line 12

In Line 12a, add Lines 5 and 7.

Under Line 12b, divide Line 5 by Line 12a. Enter this number as a decimal, rounded to three places.

Line 13

Multiply Line 11 by Line 12b. Proceed to Part III.

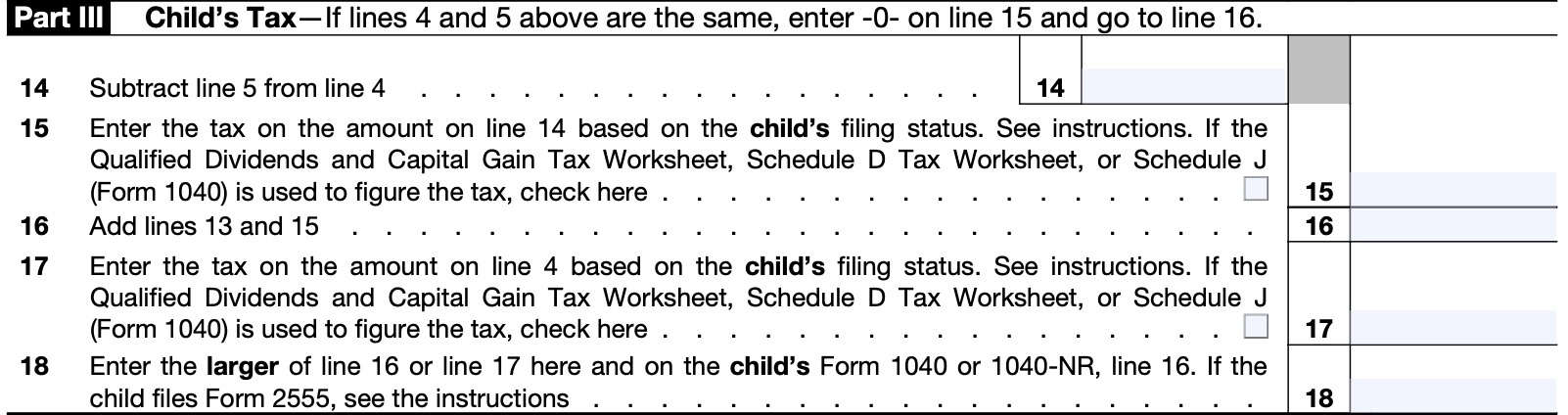

Part III: Child’s Tax

In Part III, we’ll calculate your child’s tax liability.

Line 14

Subtract Line 5 from Line 4 and enter the result. If Lines 4 and 5 are the same, enter ‘0’ on Line 15 and proceed to Line 16.

Line 15

Enter the tax on the Line 14 amount based upon the child’s tax filing status. Determine the tax by using one of the following, as applicable:

- Tax Table

- Tax Computation Worksheet

- Qualified Dividends and Capital Gain Tax Worksheet

- Schedule D Tax Worksheet, or

- Schedule J

If using one of the last three, check the box in Line 15 and see the form instructions.

Line 16

Add Lines 13 and 15.

If Lines 4 and 5 above were the same, and you entered ‘0’ on Line 15, simply bring down the value from Line 13.

Line 17

Enter the tax on the Line 4 amount based upon the child’s tax filing status. Determine the tax by using one of the following, as applicable:

- Tax Table

- Tax Computation Worksheet

- Qualified Dividends and Capital Gain Tax Worksheet

- Schedule D Tax Worksheet, or

- Schedule J

If using one of the last three, check the box in Line 17 and see the form instructions.

Line 18

Enter the larger of Line 16 or Line 17. Also enter this amount on the Form 1040 or 1040-NR, Line 16.

If the child files Form 2555, don’t enter the amount from Form 8615, Line 18, on the child’s Form 1040, Line 16. Instead, enter the amount from Form 8615, Line 18, on Line 4 of the child’s Foreign Earned Income Tax Worksheet (in the Instructions for IRS Form 1040 and Form 1040-SR).

Filing considerations

Below are some filing considerations about IRS Form 8615. First, let’s go over the concept of kiddie tax.

What is kiddie tax?

The kiddie tax is a set of special tax rules designed to prevent parents from sheltering certain income-producing property in their children’s name and taking advantage of their children’s lower tax brackets.

Below is how the kiddie tax rules work:

- First $1,250 of unearned income is tax free for the child, under the child’s standard deduction

- Second $1,250 is taxed at the child’s tax rate

- Additional unearned income is taxed at the parents’ rate

Is the kiddie tax charged at the parent’s tax rate?

Yes. Originally, the kiddie tax applied the parent’s tax rate to children’s unearned income above a certain threshold. The Tax Cuts and Jobs Act of 2017 (TCJA) changed the tax rates to that of trust tax rates.

Because that tax law change caused the unearned income of children to be taxed at a higher rate than their parents, Congress reverted back to the old rules when passing the Setting Every Community Up For Retirement Enhancement (SECURE) Act in 2019.

This means that the maximum tax rate on unearned income for children is their parent’s rate. However, the IRS rules specify the difference between earned income and unearned income for kiddie tax purposes.

What is unearned income?

For purposes of determining kiddie tax, unearned income is all taxable income that is not otherwise earned income. This includes:

- Taxable interest

- Ordinary dividends

- Capital gains (to include capital gain distributions)

- Rental income

- Royalty income

- Taxable Social Security benefits

- Pension income

- Annuity income

- Taxable scholarship and fellowship grants not reported on Form W-2

- Unemployment compensation

- Alimony

- Income received as trust beneficiary

Earned income includes:

- Wage compensation

- Tips and other compensation received for services performed

- Earnings from self-employment

- Taxable distributions from a qualified disability trust

Treatment of self-employment earnings depends on whether capital is an income-producing factor or not.

If capital is not an income-producing factor for self-employment, then earned income is generally the amounts reported on one of the following:

- Form 1040, Line 1;

- Schedule 1 (Form 1040), Lines 3 and 6; or

- IRS Form 1040-NR, Line 1a

Before we move on, let’s go back and discuss what a qualified disability trust is.

Who must file IRS Form 8615?

According to the IRS form instructions, parents must file IRS Form 8615 under the following conditions:

- The child had more than $2,500 of unearned income.

- The child is required to file a tax return

- The child either:

- Was under age 18 at the end of the tax year

- Was age 18 at the end of the tax year and didn’t have earned income that exceeded half of the child’s total support, or

- Was between age 19 and 24, a full-time student, and didn’t have earned income that exceeded half of the child’s total support

- At least one of the child’s parents was alive at the end of the tax year.

- The child doesn’t file a joint return for the tax year.

What is support?

Your support includes all amounts spent to provide the child with:

- Food

- Lodging

- Clothing

- Education

- Medical and dental care

- Recreation

- Transportation

- Other necessities

To figure your child’s support, count support provided by you, your child, and others. However, a scholarship received by your child isn’t considered support if your child is a full-time student. IRS Publication 501, Standard Deduction, and Filing Information contains additional details.

When is IRS Form 8615 due?

If the child does not file their own tax return, parents must file IRS Form 8615 to report their child’s income when they file their own tax return. If required, filing an extension on the parents’ return will automatically extend the deadline for this form as well.

Any extensions to file a tax return do not include an extension on unpaid tax liabilities. For taxes paid after the original tax filing deadline, the IRS will apply penalties and interest to the unpaid tax amount.

Video walkthrough

Watch this instructional video for step by step guidance on completing Form 8615.

Do you use TurboTax?

If you don’t, is it because the choices are overwhelming to you?

If so, you should check out our TurboTax review page, where we discuss each TurboTax software product in depth. That way, you can make an informed decision on which TurboTax offering is the best one for you!

Click here to learn more about which TurboTax option is best for you!

Frequently asked questions

Below are some frequently asked questions about IRS Form 8615.

IRS Form 8615, Tax for Certain Children Who Have Unearned Income, is the tax form that parents may use to report their child’s unearned income on their federal income tax return.

If your child uses Form 8615 to calculate tax, he or she may owe alternative minimum tax. For details, see IRS Form 6251, Alternative Minimum Tax—Individuals, and its instructions.

If your child uses Form 8615 to calculate tax, he or she may be subject to net investment income tax (NIIT). Learn more by reading about IRS Form 8960, Net Investment Income Tax.

Most likely, you will. If the parents’ income changes after the child’s return is filed, they must recalculate the child’s tax using the adjusted amounts on their amended return. Parents may also have to refigure the child’s tax if there are changes to the net unearned income of other children for whom the parent must file a Form 8615.

No. According to the IRS, a parent can elect to report the child’s interest, ordinary dividends, and capital gain distributions on their own return. If the parent makes this election, the child won’t have to file a federal income tax return or IRS Form 8615. However, the federal income tax on the child’s income, including qualified dividends and capital gain distributions, may be higher if the parent makes this election.

Where can I find a copy of IRS Form 8615?

You may download a copy from the IRS website or by selecting the file below.

Related Tax Forms

This tax form is one of the fillable tax forms provided by the Internal Revenue Service, to help taxpayers reduce their tax preparation costs. To see more forms like this, visit our free fillable tax forms page, where you’ll also find articles like this.

Unlike the IRS, our articles contain step by step instructions for each tax form, as well as video walkthroughs. You can also check out all of our videos by subscribing to our YouTube channel!