IRS Form 8801 Instructions

For certain high-income earners, the Internal Revenue Service will enforce an alternative tax calculation, known as alternative minimum tax, or AMT. However, if you’ve paid AMT in previous tax years, the tax code also allows you to take a tax deduction. You can calculate the amount of the credit on IRS Form 8801, Credit for Prior Year Minimum Tax — Individuals, Estates, and Trusts.

In this article, we’ll walk you through what you need to know about this tax form, including:

- How to complete IRS Form 8801

- When you need to file IRS Form 8801

- Frequently asked questions

Let’s start with a step by step walkthrough.

Table of contents

How do I complete IRS Form 8801?

There are three parts to this four-page tax form:

- Part I: Net Minimum Tax on Exclusion Items

- Part II: Minimum Tax Credit and Carryforward to 2023

- Part III: Tax Computation Using Maximum Capital Gains Rates

Let’s start at the top with Part I.

CAUTION: If you are not familiar with AMT rules, then you should leave this form to tax professionals, such as an enrolled agent or a certified public accountant. The following information is for educational purposes only. Nothing here should be considered tax advice.

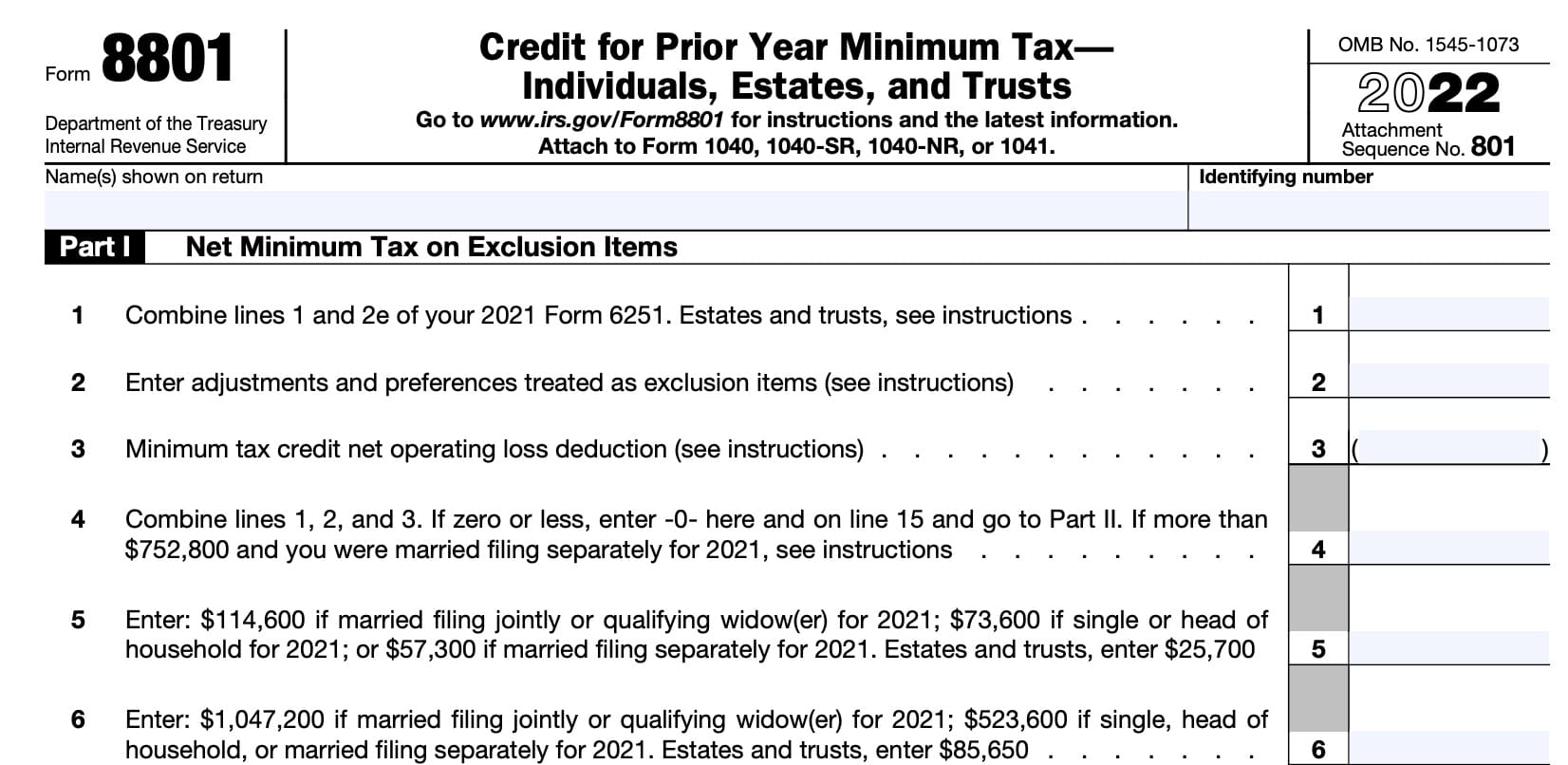

Part I: Net Minimum Tax on Exclusion Items

Before starting Line 1, be sure to include the taxpayer information as it appears on the income tax return. This should include the taxpayer’s full name and identifying number.

An identifying number can be any of the following:

- Social Security number

- Individual taxpayer identification number (ITIN)

- Employer identification number (EIN)

Line 1

For most taxpayers, combine Lines 1 and 2e of your previous year’s IRS Form 6251, then enter the total in Line 1. These lines represent the following items, respectively:

- Line 1: Taxable income from IRS Form 1040

- Line 2e: Net operating loss deduction from IRS Schedule 1

For estates and trusts

If you are filing on behalf of an estate or trust, skip Lines 1 through 3 of Form 8801, and go directly to Line 4.

To figure the amount to enter on Line 4 of Form 8801, complete Parts I and II of another 2021 Form 1041, Schedule I, as a worksheet.

After you have completed Lines 1 and 6 of Schedule I, complete the rest of Part I of Schedule I by taking into account only exclusion items. Exclusion items are the amounts included on:

- Lines 2-5

- Lines 7-8

- Other adjustments related to exclusion items included on Line 21 of Schedule I

On Line 22 of Schedule I, use the minimum tax credit net operating loss deduction, known as MTCNOLD. However, don’t limit the MTCNOLD to 90% of the total of lines 1 through 21 of Schedule I.

In Part II of Schedule I, complete Lines 33 and 34 without taking into account any basis adjustments arising from deferral items.

If the amount on Schedule I, line 27, is zero or less, enter -0- on Line 4.

Otherwise, enter on Line 4, the amount from Schedule I, Line 27, adjusted for exclusion items that were allocated to the beneficiary.

Line 2

In Line 2, enter the adjustments and preferences treated as exclusion items.

Exclusion items are only the following AMT adjustments and preference items:

- Certain itemized deductions

- Includes investment interest expense reported on Schedule E

- Certain tax-exempt interest

- Depletion

- Section 1202 exclusion

- Standard deduction

- If you did not file a Schedule A in the previous tax year, include your standard deduction

- Other adjustments related to exclusion items

Combine the following lines from your 2021 Form 6251:

- Line 2a: State and local taxes paid from IRS Schedule A, Line 7

- Line 2b: Tax refund from IRS Schedule 1

- Line 2c: Investment interest expense

- Line 2d: Depletion

- Line 2g: Interest from specified private activity bonds exempt from the regular tax

- Line 2h: Qualified small business stock

Don’t include any amount from Line 2j of the 2021 Form 6251. Instead, include the exclusion item amount from the Schedule(s) K-1 (Form 1041) you received for 2021. That amount is shown in Box 12 with code J.

If you included any adjustments related to exclusion items on Line 3 of the 2021 Form 6251, also include those adjustments in the amount you enter on Line 2. Enter the total on Line 2.

Line 3: Minimum tax credit net operating loss deduction

This is the total of the minimum tax credit net operating loss (MTCNOL) carryovers and carrybacks to 2021. Your MTCNOL is figured as follows.

Your MTCNOL is the excess of the deductions allowed when computing alternative minimum taxable income (AMTI) for 2021 (excluding the MTCNOLD) over the income used to figure AMTI taking into account only exclusion items for both.

Figure this excess with the modifications in Internal Revenue Code Section 172(d) taking into account only exclusion items.

For more details about how to calculate the MTCNOLD, see the form instructions.

Line 4

Combine Lines 1, 2, and 3, then enter the result in Line 4. If the result is zero or less, enter ‘0’ here and on Line 15. Then proceed directly to Part II.

For married taxpayers filing separate tax returns

You must include an additional amount on Line 4 if:

- Your tax filing status was married filing separately for 2021, and

- Line 4 is more than $752,800

If Line 4 is $982,000 or more, then include an additional $57,300. Otherwise, include 25% of the excess of the Line 4 amount over $752,800.

Line 5

Enter one of the following numbers in Line 5, based upon filing status:

- $114,600: Married filing jointly or qualifying widow(er) for 2021

- $73,600: Single or head of household

- $57,300: Married filing separately

- $25,700: Estates and trusts

Line 6

Enter one of the following numbers in Line 5, based upon filing status:

- $1,047,200: Married filing jointly or qualifying widow(er) for 2021

- $523,600: Single filers, head of household, or married filing separately

- $85,650: Estates and trusts

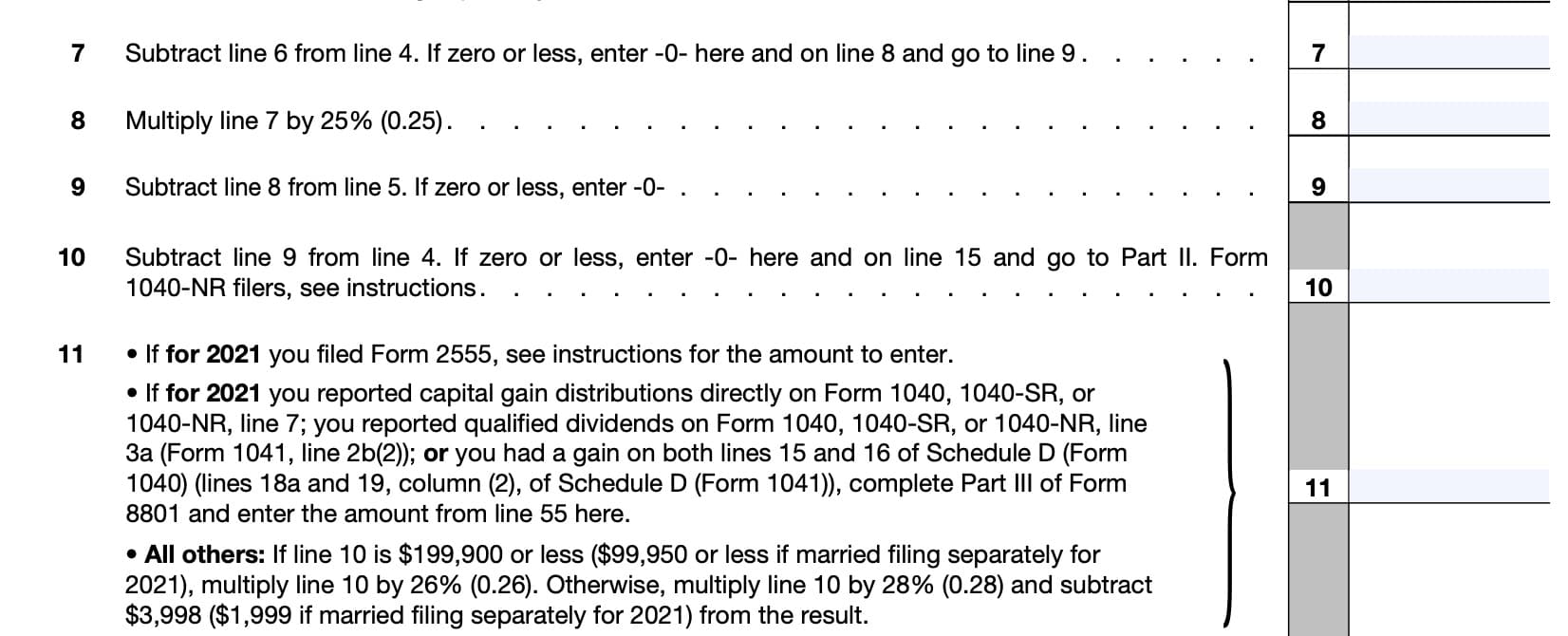

Line 7

Subtract the number in Line 6 from Line 4 and enter the result in Line 7.

If the result is zero or a negative number, enter ‘0’ here and on Line 8. Then proceed directly to Line 9.

Line 8

Multiply the Line 7 amount by 25%. Enter the result here.

Line 9

For Line 9, subtract the Line 8 number from Line 5. If zero or a negative number, enter ‘0.’

Line 10

Subtract the Line 9 amount from Line 4. If zero or less, enter ‘0’ here and on Line 15. Then go to Part II.

Form 1040-NR filers

If you filed Form 1040-NR for 2021 and had a net gain on the disposition of U.S. real property interests, then Line 10 can’t be less than the smaller of:

- The net gain on the disposition of U.S. real property interests, or

- Line 4

Line 11

There are three different situations in Line 11 that might apply to taxpayers:

- Foreign earned income

- Capital gains, qualified distributions, or capital gains distributions

- All other taxpayers

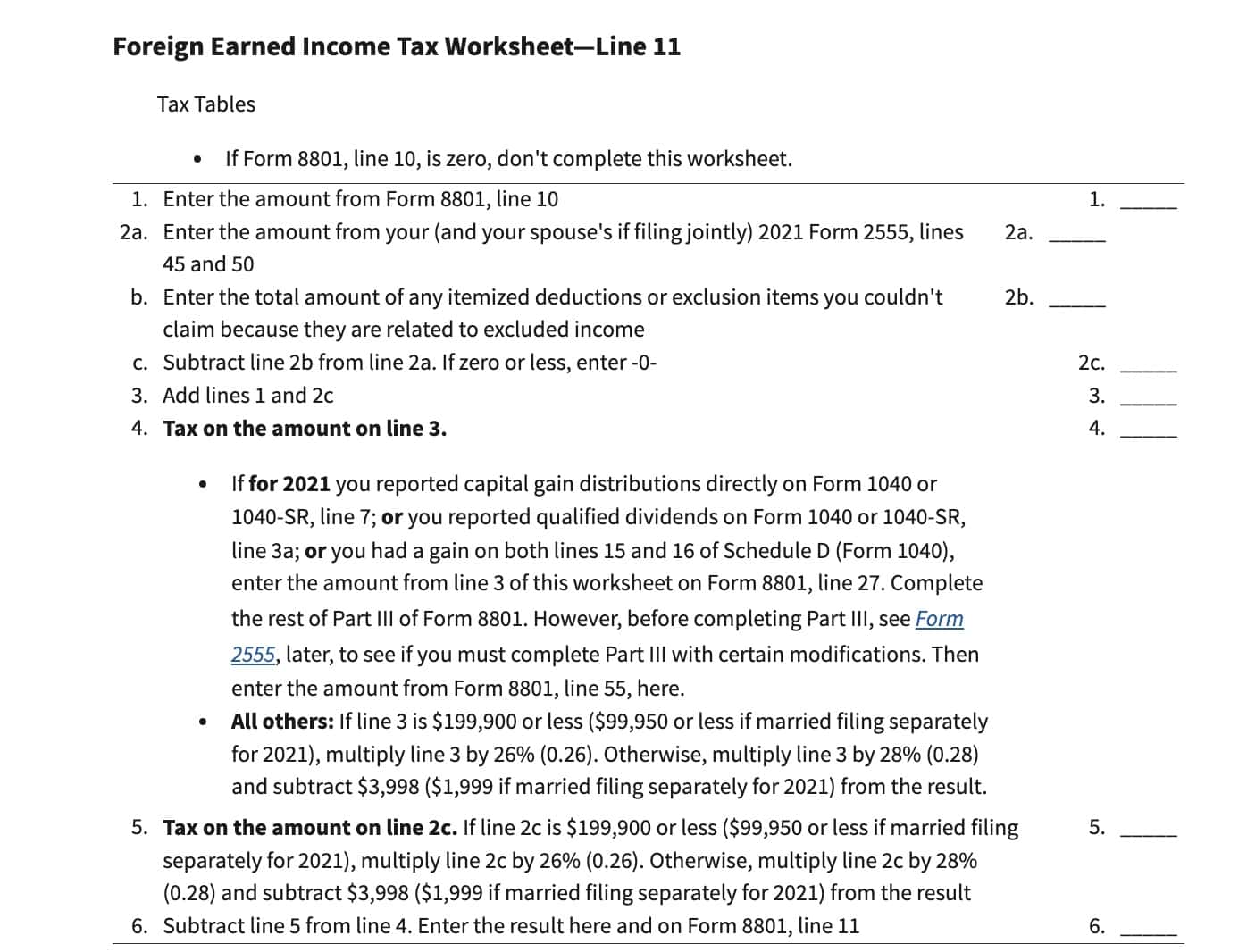

Foreign earned income

If you filed IRS Form 2555 for 2021, then you must complete the foreign earned income tax worksheet below to determine what to enter for Line 11.

Capital gains treatment

If you reported any of the following during 2021, then you must complete Part III of IRS Form 8801, then enter the Line 55 amount here:

- Capital gain distributions directly on Form 1040, 1040-SR, or 1040-NR, Line 7

- Qualified dividends on Form 1040, 1040-SR, or 1040-NR, line 3a (Form 1041, line 2b(2))

- A gain on both:

- IRS Form 1040: Lines 15 and 16 of Schedule D

- IRS Form 1041: Lines 18a and 19, column (2), of Schedule D

All other taxpayers

If Line 10 is $199,900 or less ($99,950 or less if married filing separately for 2021), multiply Line 10 by 26% (0.26).

Otherwise, multiply Line 10 by 28% (0.28) and subtract $3,998 ($1,999 if married filing separately for 2021) from the result.

Line 12: Minimum tax foreign tax credit on exclusion items

If you made an election to claim the foreign tax credit on your 2021 Form 1040, 1040-SR, or 1040-NR without filing IRS Form 1116, your minimum tax foreign tax credit on exclusion items (MTFTCE) is the same as the foreign tax credit on your 2021 Schedule 3 (Form 1040), Line 1. Enter that amount on Line 12.

Otherwise, your MTFTCE is your 2021 AMT foreign tax credit (AMTFTC) refigured using only exclusion items. If necessary, the form instructions contain step by step guidance on how to perform this calculation.

Line 13: Tentative minimum tax on exclusion items

Subtract Line 12 from Line 11. This represents the the tentative AMT amount based on exclusion items.

Line 14

Enter either of the following, whichever one applies, from tax year 2021:

- IRS Form 6251, Line 10

- IRS Form 1041, Schedule I, Line 53

Line 15: Net minimum tax on exclusion items

Subtract the Line 14 amount from Line 13. If the result is zero or a negative number, enter ‘0.’

This represents the net minimum tax on exclusion items.

Let’s move on to Part II.

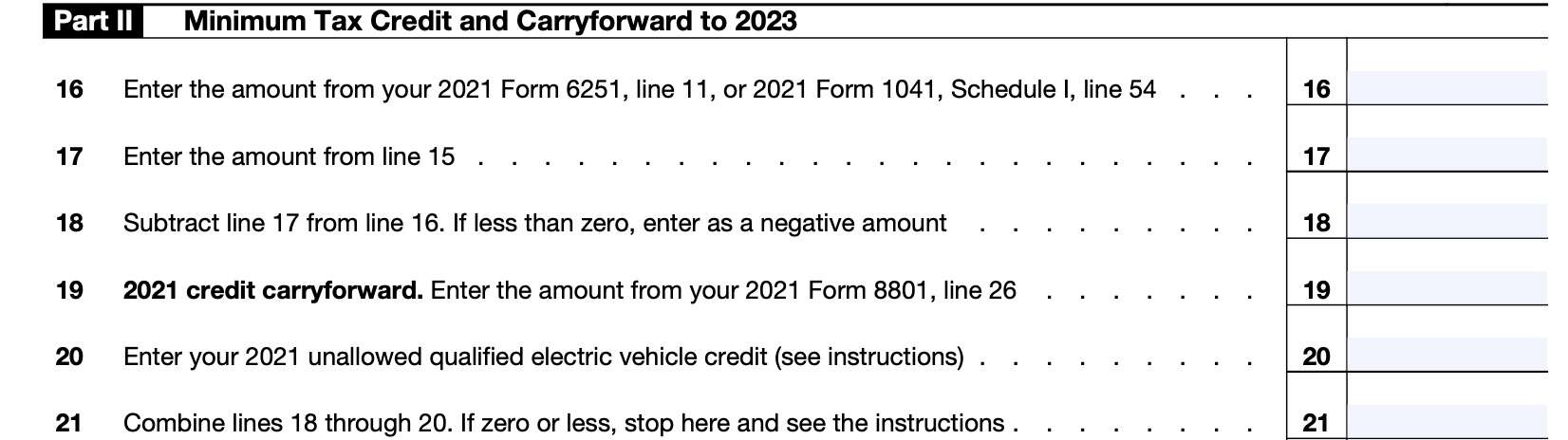

Part II: Minimum Tax Credit and Carryforward to 2023

Line 16

In Line 16, enter your alternative minimum tax from the prior year. Your AMT is one of the following, as applicable:

- IRS Form 6251, Line 11

- IRS Form 1041, Schedule I, Line 54

Line 17

Carry down the net minimum tax on exclusion items from Line 15.

Line 18

Subtract the Line 17 amount from the Line 16 number. If the result is less than zero, enter as a negative number.

Line 19: 2021 Credit carryforward

Enter the amount from last year’s IRS Form 8801, Line 26.

Line 20

In Line 20, enter the unallowed qualified electric vehicle credit from last year.

Specifically, enter any qualified electric vehicle credit not allowed for 2021 solely because of the limitation under IRC Section 30(b)(3)(B).

Line 21

Combine Lines 18 through 20, then enter the result in Line 21.

If line 21 is zero or less, you don’t have a minimum tax credit or a tax credit carryforward. Don’t complete the rest of IRS Form 8801 and don’t file it.

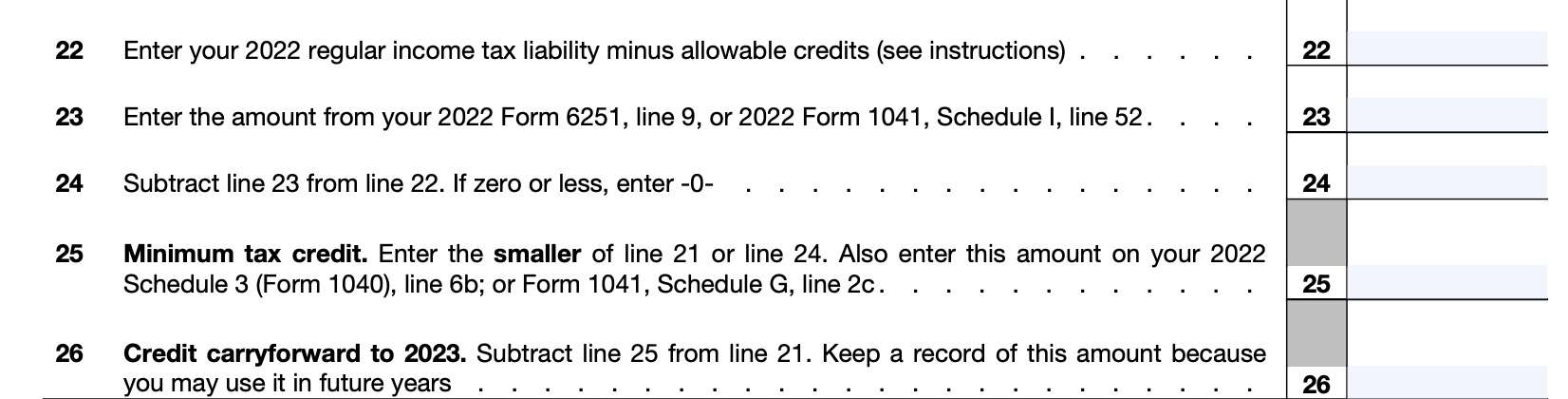

Line 22

In Line 22, enter your current year regular income tax liability, minus allowable credits.

Individuals Form 1040, 1040-SR, or 1040-NR filers

Add the following amounts:

- Line 16 from Form 1040, 1040-SR or 1040-NR: This is your federal income tax bill

- Line 2 from Schedule 2

from Line 16 of your individual income tax return and Schedule 2 (Form 1040), line 2.

Subtract the following tax credits:

- Child tax credit or credit for other dependents from Schedule 8812

- IRS Schedule 3, Lines 1 through 6z

- Do not include the prior-year minimum tax credit on Line 6b

- Do not include any credit claimed on IRS Form 8912

If the result is zero or a negative number, enter ‘0.’

Estates & trusts

From Form 1041, Schedule G, add the credits on Lines 2a and 2b, plus any write-in credits on Line 2e.

Subtract the result from the total of Lines 1a and 1b, plus any IRS Form 8978 amount included on Line 1d.

Enter the result. If the result is zero or less, enter ‘0.’

Line 23: tentative minimum tax

Enter the tentative minimum tax from either of the following:

- IRS Form 6251, Line 9

- IRS Form 1041, Schedule I, Line 52

Line 24

Subtract Line 23 from Line 22. Enter the result in Line 24.

If the answer is zero or a negative number, enter ‘0.’

Line 25: Minimum tax credit

Enter the smaller of the following:

Enter this amount on either of the following tax return forms for the current given year:

- Schedule 3, Line 6b

- Form 1041, Schedule G, Line 2c

Line 26: Credit carryforward to future tax years

Subtract Line 25 from Line 21. This represents your unused minimum tax credit from the current given year that you can carry forward to the following year or subsequent years.

Part III: Tax Computation Using Maximum Capital Gains Rates

Do not complete Part III unless you were directed to do so by Line 11 instructions or the foreign earned income tax worksheet.

Line 27

In Line 27, enter the Line 10 amount. If you filed IRS Form 2555 for the previous calendar year, then you should enter the amount from Line 3 of the Foreign Earned Income Tax Worksheet.

If your 2021 taxable income was zero or less, enter -0- on Line 35. You must also complete one of the following, whichever is applicable, before completing lines 28, 29, and 30 of Part III:

- Lines 2 through 4 of the Qualified Dividends and Capital Gain Tax Worksheet in the 2021 Instructions for Form 1040.

- Lines 2 through 13 of the Schedule D Tax Worksheet in the 2021 Instructions for the Schedule D that applies to your income tax return

- Lines 2 through 4 of the Qualified Dividends Tax Worksheet in the 2021 Instructions for Form 1041.

- Lines 22 through 26 of the 2021 Schedule D (Form 1041).

To determine which worksheet or form above applies to you, refer to the 2021 Instructions for:

- IRS Form 1040, Line 16

- IRS Form 1040-NR, Line 16, or

- IRS Form 1041, Schedule G, Line 1a

Once complete, proceed to Line 28.

Line 28

For Line 28, enter one of the following, as applicable to your tax situation:

- Line 4, 2021 Qualified Dividends and Capital Gain Tax Worksheet

- Line 13, 2021 Schedule D Tax Worksheet

- Line 26, 2021 Schedule D (Form 1041)

Estates and trusts

If you filed IRS Form 1041, and did not use the Schedule D Tax Worksheet or Part V of Schedule D to calculate your tax, then do the following:

- Determine amount from Line 4 of the Qualified Dividends Tax Worksheet in the 2021 Form 1041 instructions

- Enter this amount on Line 28 and Line 30, below

- Skip Line 29, below

- Enter the amount from Line 5 on the Qualified Dividends Tax Worksheet on both Line 35 and Line 42, below

IRS Form 2555 filers

If you filed IRS Form 2555 and have an AMT capital gain excess, then you must make some modifications to Part III as you complete it.

How to determine whether you have an AMT capital gain excess

Subtract Line 10 from either of the following, as applicable:

- Line 4 of your 2021 Qualified Dividends & Capital Gain Tax Worksheet

- Line 10 of the 2021 Schedule D Tax Worksheet

If the result is greater than zero, that amount is known as AMT capital gain excess.

If you have an AMT capital gain excess, you must use the following modifications to calculate the Line 28, Line 29, and Line 30 amounts. These modifications only apply to these calculations.

- Reduce the following amount, as applicable, by your AMT capital gain excess:

- Line 3 of your 2021 Qualified Dividends and Capital Gain Tax Worksheet, or

- Line 9 of your 2021 Schedule D Tax Worksheet

- Do not reduce below zero

- Reduce the following amount, as applicable, by any unused AMT capital gain excess:

- Line 2 of your 2021 Qualified Dividends and Capital Gain Tax Worksheet, or

- Line 6 of your 2021 Schedule D Tax Worksheet

- Do not reduce below zero

- Reduce the amount on Line 18 of your 2021 Schedule D (Form 1040) by your AMT capital gain excess

- Do not reduce below zero

- Include your AMT capital gain excess as a Loss on Line 16 of your 2021 Unrecaptured Section 1250 Gain Worksheet in the 2021 Instructions for Schedule D (Form 1040).

Line 29

In Line 29, enter either of the following, as applicable:

- IRS Form 1040: Line 19 from Schedule D

- IRS Form 1041: Line 18b, Column (2), from Schedule D

Line 30

Enter the smaller of:

Line 31

In Line 31, enter the smaller of:

Line 32

Subtract Line 31 from Line 27. Enter the result here.

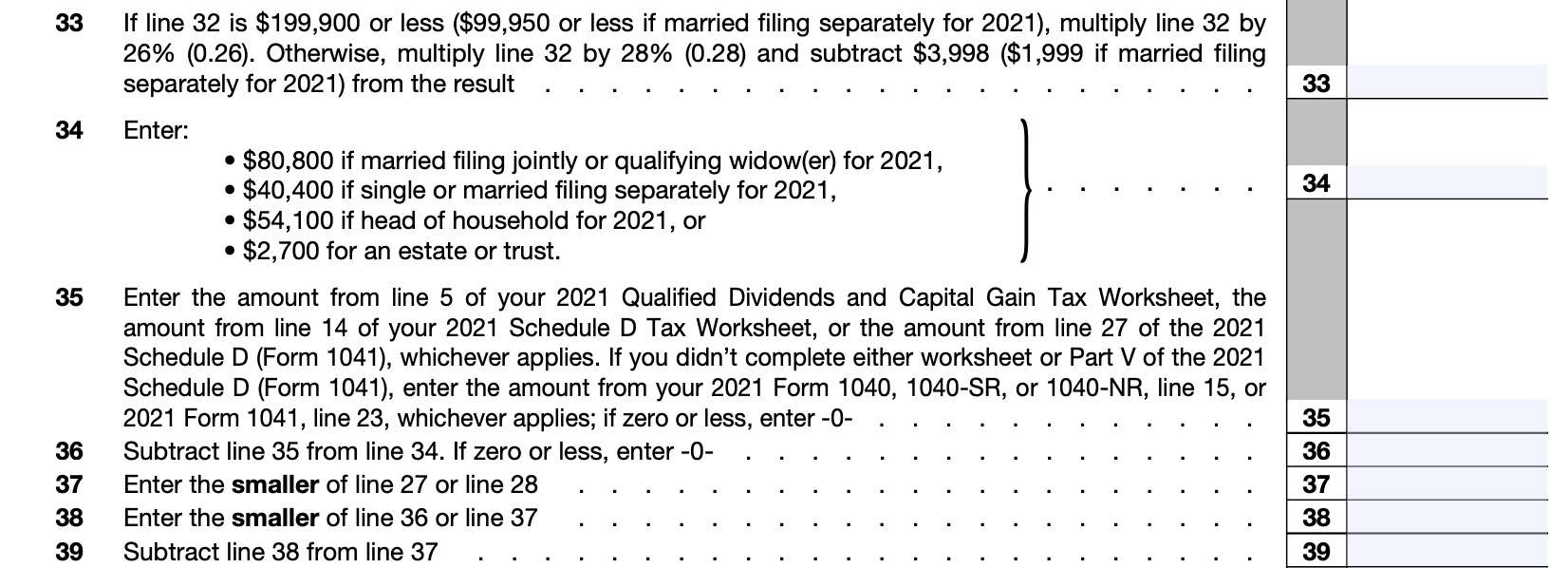

Line 33

If Line 32 is $199,900 or less ($99,950 if married filing separately for 2021), then multiply Line 32 by 26% (0.26).

Otherwise, multiply Line 32 by 28% (0.28), then subtract:

- $1,999 for married filing separately

- $3,998 for all other taxpayers

Enter the result in Line 33.

Line 34

Enter one of the following, as applicable to your 2021 tax filing status:

- Married filing jointly or qualifying widower(er): $80,800

- Single or married filing separately: $40,400

- Head of household: $54,100

- Estates and trusts: $2,700

Proceed to Line 35.

Line 35

Enter one of the following, whichever applies:

- Line 5 of from 2021 Qualified Dividends and Capital Gain Tax Worksheet

- Line 14 from 2021 Schedule D Tax Worksheet

- Line 27 from 2021 Schedule D (IRS Form 1041)

If you did not complete either worksheet or Part V of the 2021 Schedule D (Form 1041), then enter the taxable income figure that applies:

- Line 15 from IRS Form 1040

- Line 23 from IRS Form 1041

If taxable income is zero or less, enter ‘0.’

Line 36

Subtract Line 35 from Line 34. If this is zero or a negative number, enter ‘0.’

Line 37

Enter the smaller of the following:

Line 38

For Line 38, enter the smaller of:

Line 39

Subtract Line 38 from Line 37. Enter the difference here.

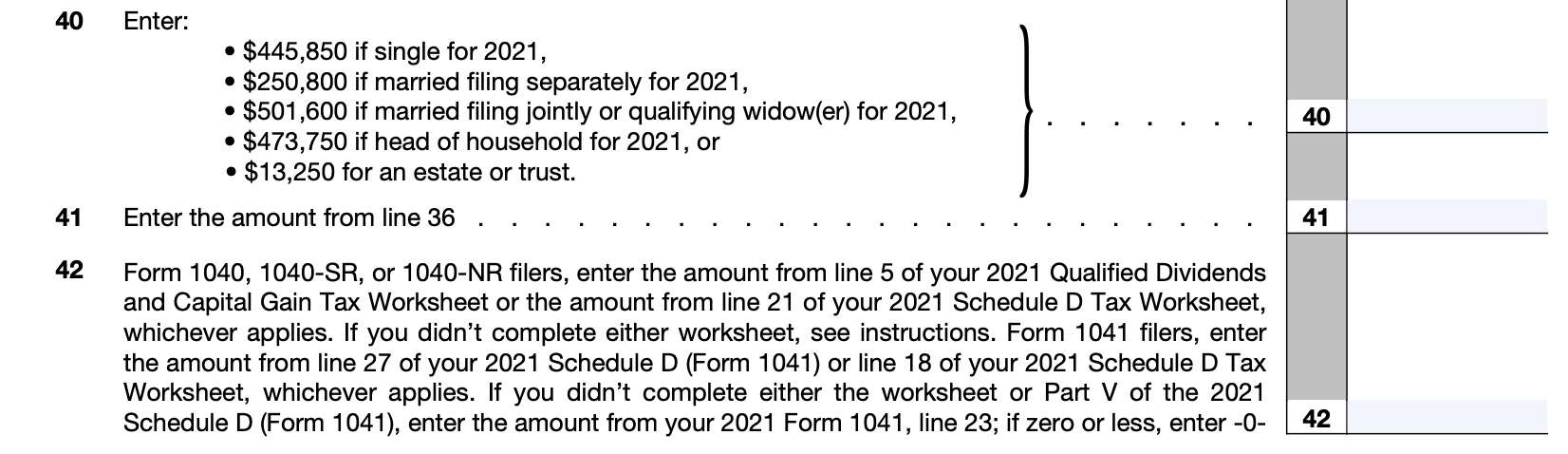

Line 40

In Line 40, enter one of the following, based upon your 2021 tax filing status:

- Single: $445,850

- Married filing separately: $250,800

- Married filing jointly or qualifying widow(er): $501,600

- Head of household: $473,750

- Estates & trusts: $13,250

Line 41

Enter the amount from Line 36.

Line 42

The amount you enter in Line 42 depends on your status as a taxable entity.

Individual taxpayers

For taxpayers filing an individual tax return, enter whichever applies to your situation:

- Line 5 from your 2021 Qualified Dividends and Capital Gain Tax Worksheet

- Line 21 from your 2021 Schedule D Tax Worksheet

- Line 15 from your tax return

- If zero or less, enter ‘0’

If you didn’t complete either 2021 worksheet and you filed a 2021 Form 2555, enter the amount from Line 3 of the Foreign Earned Income Tax Worksheet in the 2021 Form 1040 Instructions.

Estates & trusts

Enter one of the following, as applicable:

- Line 27 from your 2021 Schedule D

- Line 18 from Schedule D Tax Worksheet

If you did not complete either the worksheet or Part V from the Schedule D, then enter the amount from Line 23 on your 2021 Form 1041. This represents your taxable income. If zero or less, then enter ‘0.’

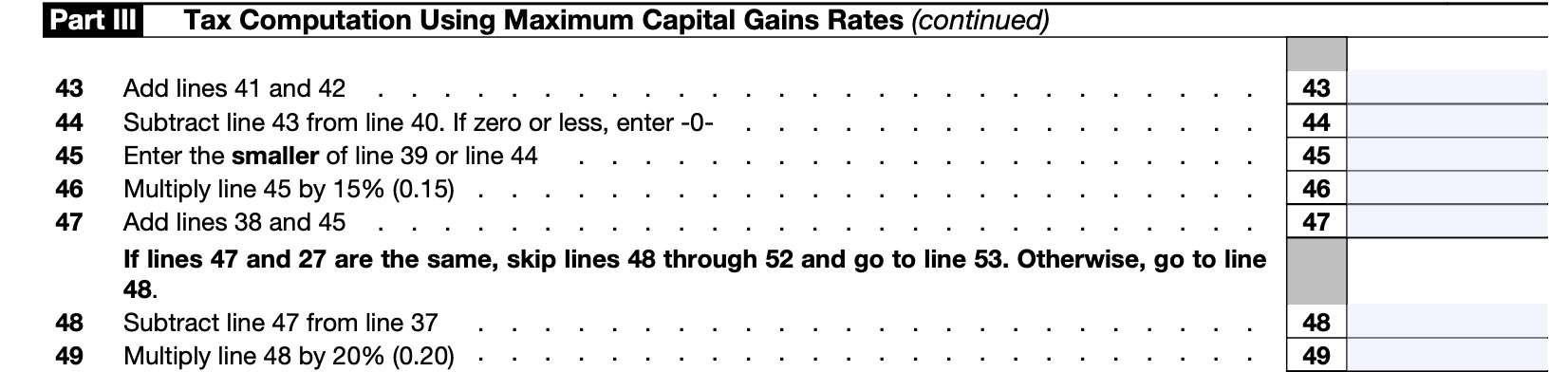

Line 43

Add Line 41 and Line 42. Enter the result here.

Line 44

Subtract Line 43 from Line 40. If this results in a negative number, enter ‘0.’

Line 45

In Line 45, enter the smaller of:

Line 46

Multiply the Line 45 amount by 15% (0.15). Enter the result here.

Line 47

Add Line 38 and Line 45. Enter the total in Line 47.

If Line 47 equals Line 27, then skip Lines 48 through 52 and go directly to Line 53. Otherwise, proceed to Line 48.

Line 48

Subtract Line 47 from Line 37. Enter the difference in Line 48.

Line 49

Multiply Line 48 by 20% (0.20).

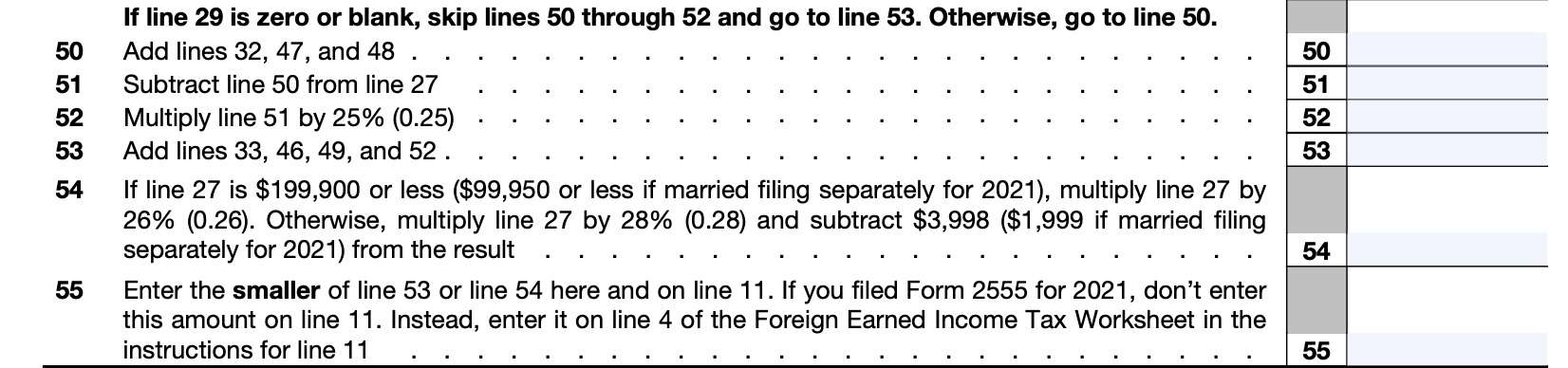

If Line 29 is zero or blank, skip Lines 50 through 52 and go to Line 53. Otherwise, go to Line 50.

Line 50

Add the following, and enter the total in Line 50:

Line 51

Subtract Line 50 from Line 27. Enter the difference in Line 51.

Line 52

Multiply the Line 51 amount by 25% (0.25). Enter the product here.

Line 53

Add the following, then put the result in Line 53:

Line 54

If Line 27 is $199,900 or less ($99,950 if married filing separately for 2021), then multiply Line 27 by 26% (0.26).

Otherwise, multiply Line 27 by 28% (0.28), then subtract:

- $1,999 for married filing separately in 2021

- $3,998 for all other taxpayers

Enter the result in Line 54.

Line 55

Enter the smaller of the following here and in Line 11:

If you filed IRS Form 2555 for 2021, then do not enter this amount on Line 11. Instead, enter it on Line 4 of the Foreign Earned Income Tax Worksheet.

Video walkthrough

Watch this instructional video to learn more about claiming a tax credit for prior year minimum tax with IRS Form 8801.

Do you use TurboTax?

If you don’t, is it because the choices are overwhelming to you?

If so, you should check out our TurboTax review page, where we discuss each TurboTax software product in depth. That way, you can make an informed decision on which TurboTax offering is the best one for you!

Click here to learn more about which TurboTax option is best for you!

Frequently asked questions

Use Form 8801 if you are an individual, estate, or trust to figure the amount of any credit for alternative minimum tax (AMT) you incurred in previous years and to figure any credit carryforward to next year or future years.

Any individual, estate, or trust should file IRS Form 8801 if they had an AMT liability and adjustments or preferences other than exclusion items, a credit carryforward to the current year, or an unallowed qualified electric vehicle credit.

Where can I find IRS Form 8801?

As with other tax forms, you may find IRS Form 8801 on the IRS website. For easier access and personal convenience, we’ve enclosed the latest version of IRS Form 8801 as a PDF file in this article.

Related tax articles

This tax form is one of the fillable tax forms provided by the Internal Revenue Service, to help taxpayers reduce their tax preparation costs. To see more forms like this, visit our free fillable tax forms page, where you’ll also find articles like this.

Unlike the IRS, our articles contain step by step instructions for each tax form, as well as video walkthroughs. You can also check out all of our videos by subscribing to our YouTube channel!