IRS Form 8978 Instructions

If you’re a partner in a non-passthrough entity that has elected to push out certain tax adjustments, you may be required to file IRS Form 8978. In this article, we’ll walk through this tax form. Specifically, we’ll discuss:

- How to complete IRS Form 8978

- Who must file IRS Form 8978

- When is IRS Form 8978 due?

- Frequently asked questions

Let’s begin by walking through IRS Form 8978, step by step.

Table of contents

How do I complete IRS Form 8978?

Although this form is only one page, it can be complicated. There are 3 parts to this form (4 parts, including the Schedule A attachment):

- Part I: Computation of Additional Reporting Year Tax

- Part II: Penalties

- Part III: Interest

- Schedule A: Schedule of Adjustments

We’ll go through this, step by step, so you can better understand how this form works.

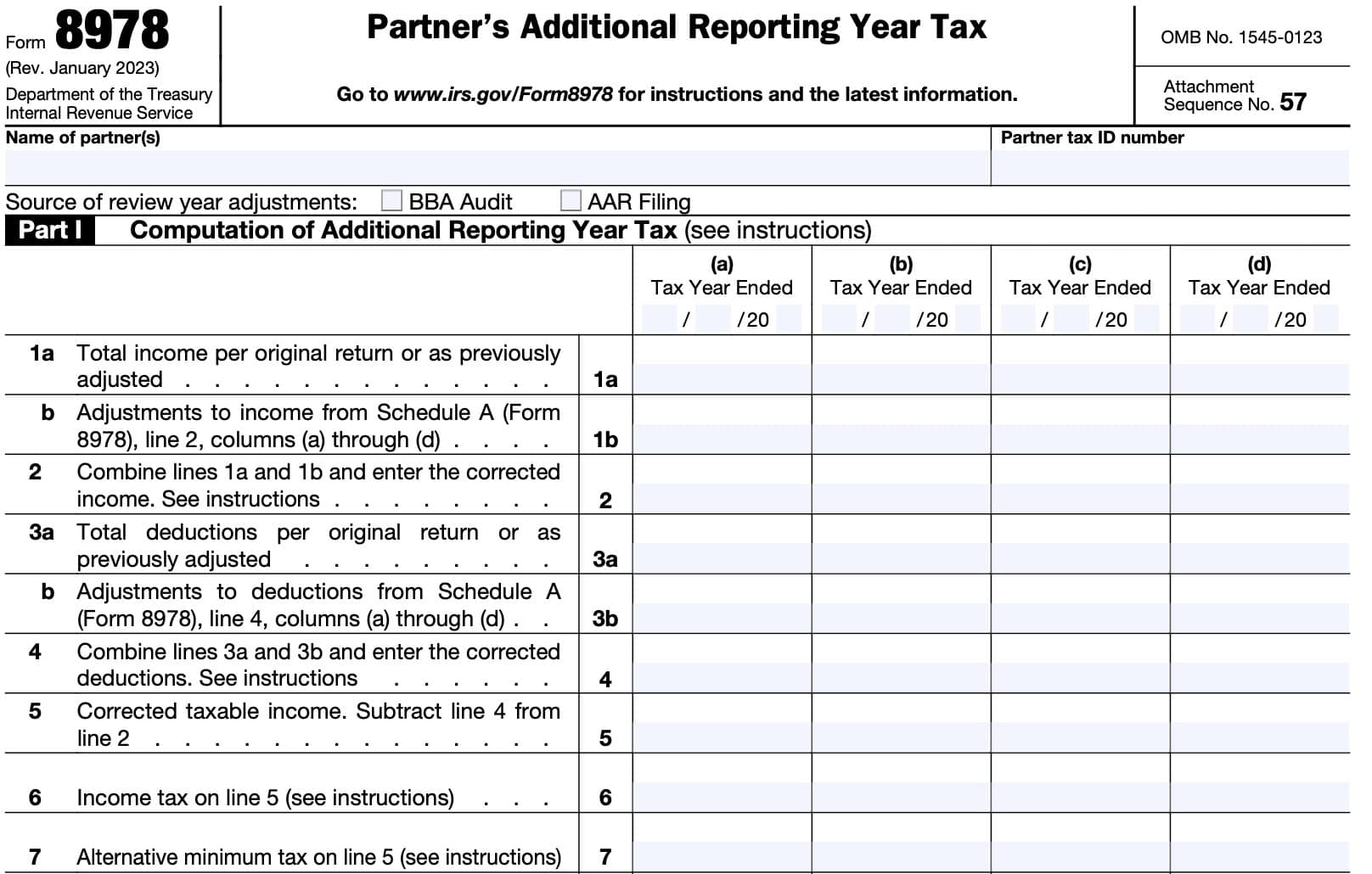

Part I: Computation of Additional Reporting Year Tax

Part I contains 4 columns, which can support up to 4 adjustment years.

If your affected year is the only year requiring an adjustment, use only column (a). In situations where there are one or more intervening years (years after the adjustment), then use the number of columns you need.

If there are more than 4 applicable years, then you’ll need to complete multiple versions of Form 8978. Each Form 8978 should have all lines completed and the total of all the Line 14 amounts should be reported on the appropriate line of the partner’s return. Include a Schedule A for each Form 8978.

Source of review year adjustments

Check the appropriate box for the type of reviewed year adjustments pertaining to this Form 8978:

- BBA Audit

- AAR Filing

Multiple filings

In some situations, you may receive multiple 8986 forms, relating to both AAR adjustments and BBA adjustments for partnership returns.

If this occurs, the IRS instructions state that the Form 8978 related to AAR adjustments should be completed first. After that, the numbers would be included on the subsequent Form 8978, and included in the ‘as previously reported’ numbers related to the audit adjustments.

Each Form 8978 should have applicable lines completed, and the passthrough partner should add all the additional amounts on Line 14 (total increase/decrease to tax) from all the Forms 8978 and report the sum on the appropriate line of the tax return.

Line 1a: Total income per original return or as previously adjusted

Enter the total income amount as shown on your original or amended return, or as adjusted by the IRS. Enter net negative adjustment amounts in parentheses.

Line 1b: Adjustments to income From Schedule A, Line 2, columns (a) through (d)

Enter the total amount of all lines from Schedule A, Line 2, Adjustments to Income.

Line 2

Combine Line 1a and Line 1b. This represents your corrected income.

Line 3a: Total deductions per original return or as previously adjusted

Enter the total amount of deductions as shown on your original or amended tax return, or as adjusted by the IRS. Enter negative amounts in parentheses.

Line 3b: Adjustments to deductions From Schedule A, Line 4, columns (a) through (d)

Enter the total amount from Schedule A, Line 4, Adjustments to Deductions.

Line 4

Combine Lines 3a and 3b. This represents your corrected deductions.

Line 5: Corrected taxable income

Subtract Line 4 from Line 2, then enter the result. This is your corrected taxable income.

If, because of changes in tax attributes, the corrected taxable income is different from the difference between Line 4 and Line 2, you must include a separate statement. This statement should show how you calculated the corrected taxable income.

Line 6: Income tax on Line 5

Include a separate statement that explains how you calculated your new income tax liability. Enter the new income tax on Line 6.

Line 7: Alternative minimum tax on Line 5

If your tax situation is subject to alternative minimum tax (AMT), enter your new AMT amount here. Also include a statement that outlines your AMT calculation based upon the audit adjustments.

Line 8: Total corrected income tax

Add Lines 6 and 7. This represents your total corrected income tax.

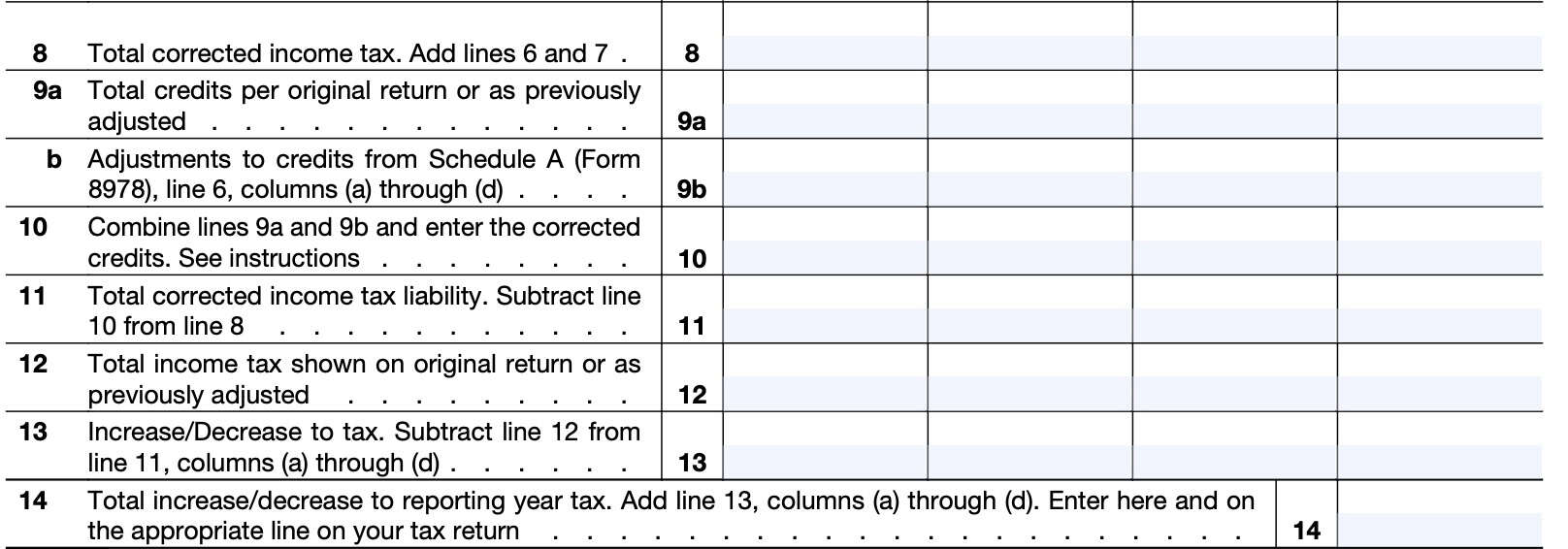

Line 9a: Total credits per original return or as previously adjusted

Enter the total amount of tax credits reflected on your original tax return. This should reflect both refundable and nonrefundable credits.

Line 9b: Adjustments to credits From Schedule A, Line 6, columns (a) through (d)

Enter the amount from Schedule A, Line 6, Total adjustments to credits.

Line 10

Combine all credits from Line 9a and Line 9b. This represents your total corrected credits.

Line 11: Total corrected income tax liability

Subtract Line 10 from Line 8. This should reflect your total corrected income tax liability.

If the actual total corrected tax liability is different from the calculation, you must attach a statement addressing the difference.

Line 12: Total income tax shown on original return, or as previously adjusted

Enter the original income tax shown on your original or amended tax return.

Line 13: Increase/Decrease to tax

Subtract Line 12 from Line 11. A positive adjustment amount indicates a tax increase, while a negative amount shows a decrease in your tax bill.

Line 14: Total increase/decrease to reporting year tax

Add the total of columns 13(a) through 13(d). If only reporting for one tax year, this sum should be the same as Line 13.

Part II: Penalties

If applicable, the IRS may impose additional penalties, which should be reflected on the IRS Form 8986. Form 8986 will list applicable penalties, if any, and which line items are affected.

Line 15: Penalties

If penalties apply, include a statement showing how the penalties were figured. Enter this amount in the applicable column(s) of Form 8978.

Penalties for each applicable tax year should be reported on Line 15, columns (a) through (d).

Line 16: Total penalties

Add the total of all penalties in Line 15. This represents your total penalties for all applicable tax years.

Part III: Interest

Interest on any increase in income tax is figured from the original due date of your income tax return for each tax year to which an increase in tax is attributable. Section 6226(b)(3) applies.

Line 17: Interest

Calculate interest at the underpayment rate under Section 6621(a)(2). However, substitute “five percentage points” for “three percentage points” for purposes of section 6621(a)(2)(B).

This means the sum of the federal short-term rate plus five percentage points, instead of three percentage points.

For additional reporting year tax reported as a result of a Form 8986 from an AAR, this substitution is not made. Report interest for each applicable tax year on Line 17, columns (a) through (d).

Interest on penalties is calculated in the same manner as the interest on income tax. However, the interest calculation on penalties starts from the due date of the partner’s tax return, or extended due date, if applicable.

Line 18: Total Interest

Add the totals of interest (Line 17) across all four columns. This should be the total interest you owe.

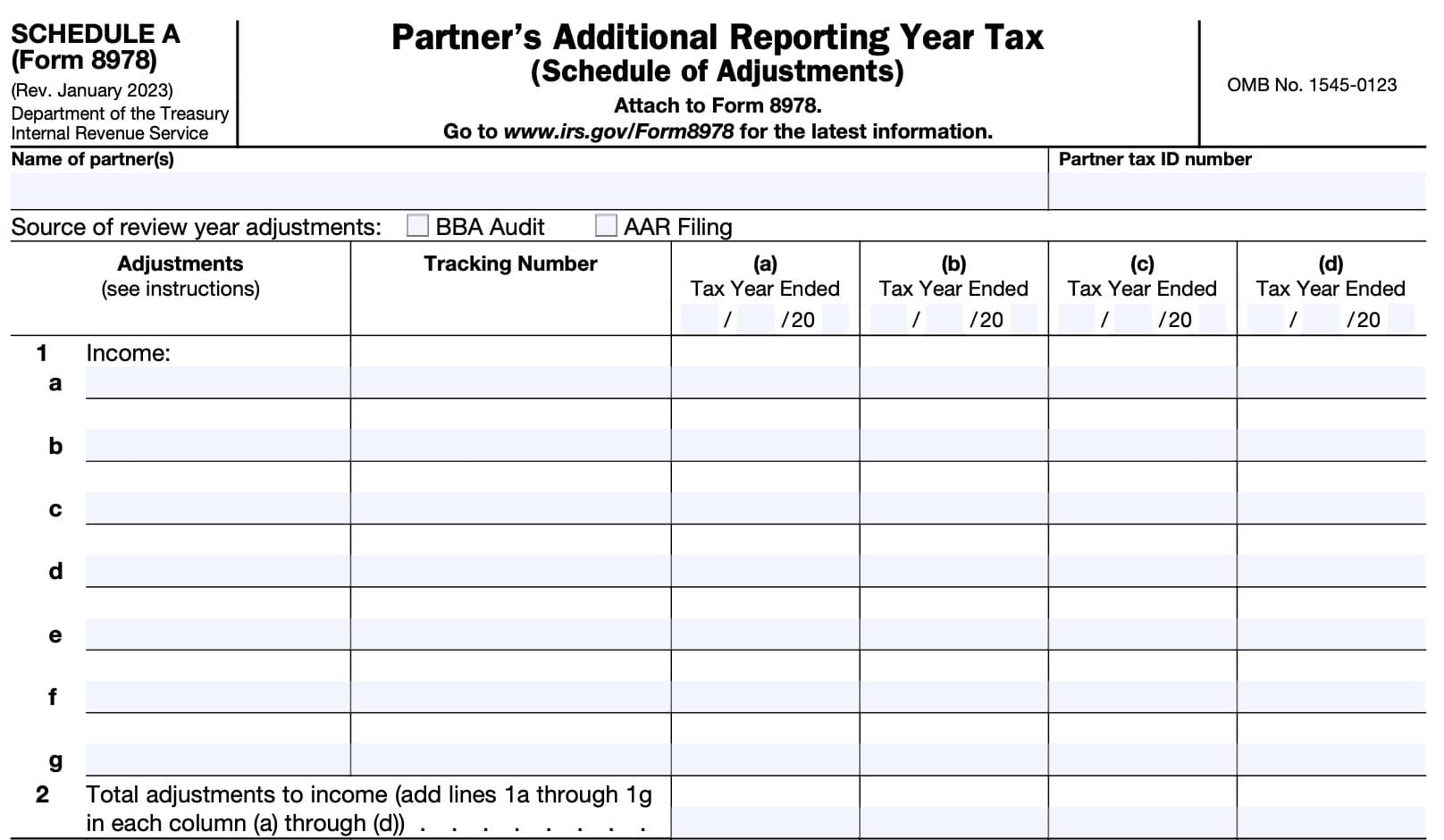

IRS Form 8978 Schedule A, Schedule of Adjustments

Use the Schedule A form to determine the amount of adjustments that go into IRS Form 8978, specifically:

Top of Schedule A

At the top of Schedule A, you’ll see fields for taxpayer name and tax ID number. This should be the same as on Form 8978.

Just below the name, check the source of the review year adjustments:

- BBA Audit

- AAR filing

Adjustments to income

Line 1

Enter all the adjustments individually from Form 8986, Part V, that affect taxable income. Generally, this may include adjustments to the following:

- Ordinary income

- Rental income

- Interest and dividend income

- Royalty income

- Capital gains and losses

- Other income

Also include related amounts and adjustments not on Form 8986 that result from changes to partner-level tax attributes and other items as a result of adjustments from Form 8986.

Line 2

Enter the total of all adjustments from Line 1. Carry the total of each column to the corresponding column on Form 8978, Line 1b.

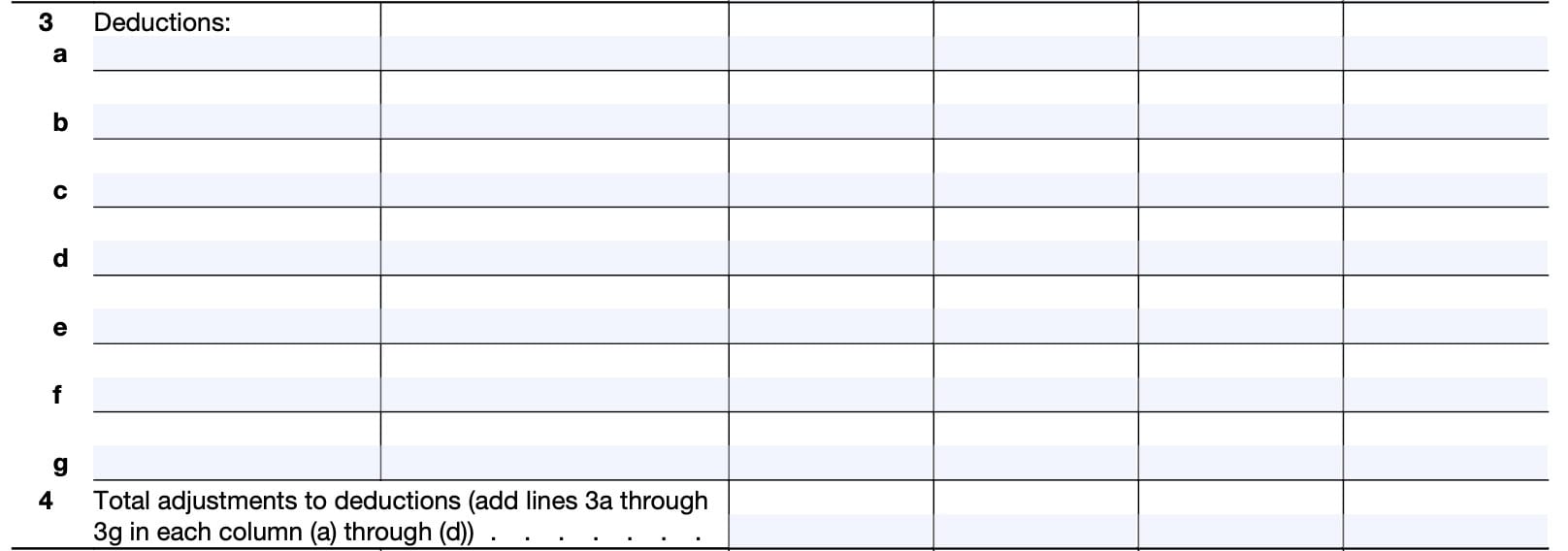

Adjustments to deductions

Line 3

Enter all the adjustments individually from Form 8986, Part V, that affect deductions from income. Generally, this includes adjustments to separately stated items such as a Section 179 deduction.

Also include related amounts and adjustments not on Form 8986 that result from changes to partner-level tax attributes as a result of adjustments from Form 8986.

Line 4

Enter the total of all adjustments from Line 3. Carry the total of each column to the corresponding column on Form 8978, Line 3b.

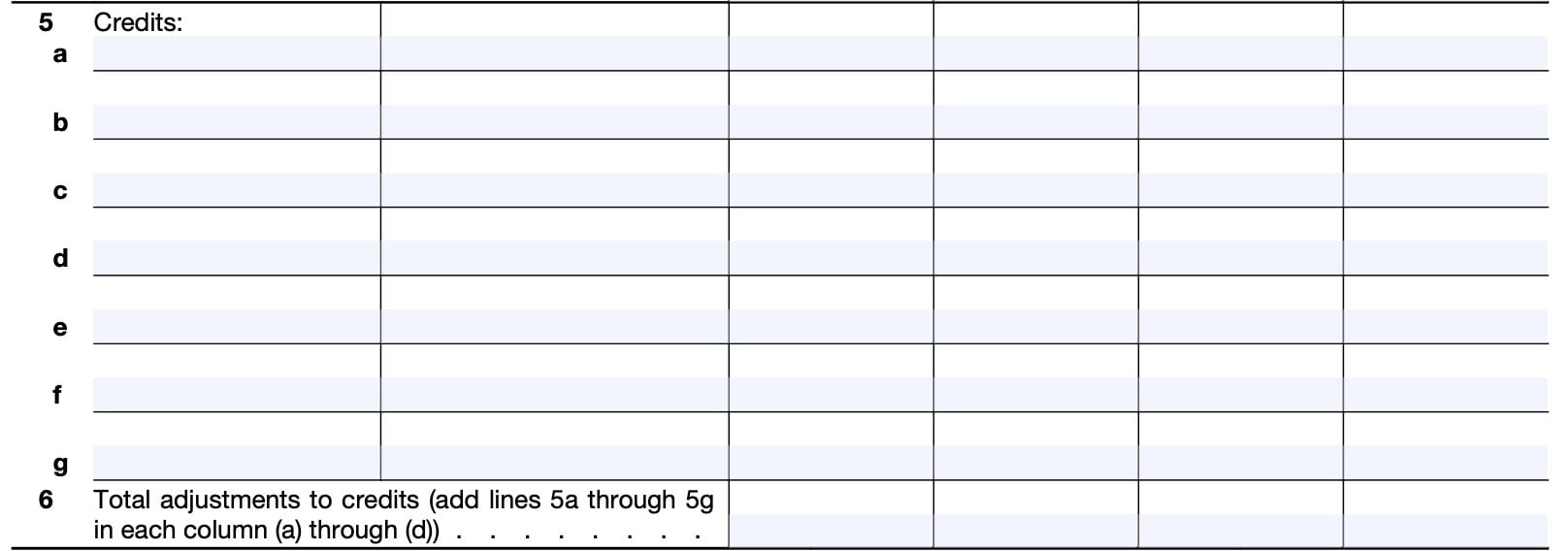

Adjustments to credits

Line 5

Enter all the adjustments individually from Form 8986, Part V, that affect tax credits.

Also include related amounts and adjustments not on Form 8986 that result from changes to partner-level tax attributes as a result of adjustments from Form 8986.

Line 6

Enter the total of all adjustments from Line 5. Carry the total of each column to the corresponding column on Form 8978, Line 9b.

What is IRS Form 8978?

IRS Form 8978, Partner’s Additional Reporting Year Tax, is used by non-pass-through partners to reflect partnership adjustments documented by their BBA partnership on IRS Form 8986. In turn, this depends on the elections the partnership may have made under Internal Revenue Code Sections 6226 and 6227 in an affected year.

This presents a few logical questions:

- What is IRS Form 8986?

- What is a BBA partnership?

- What are IRC Sections 6226 and 6227?

What is IRS Form 8986?

IRS Form 8986, Partner’s Share of Adjustment(s) to Partnership-Related Item(s) (Required Under Sections 6226 and 6227), is the IRS form that a BBA partnership may use to transmit each partner’s share of adjustments to partnership-related items.

The following entities should file IRS Form 8986:

- An audited partnership that has made an election under IRC Section 6226.

- Direct or indirect pass-through partners that receive a Form 8986 related to an audited partnership if they choose to furnish statements to their partners to further push out the adjustments

- Partnerships that file an administrative adjustment request (AAR) under IRC Section 6227 and either elect to:

- Push out the resulting adjustments to their partners, or

- Have adjustments that do not result in an imputed underpayment (IU)

- Direct or indirect passthrough partners that receive a Form 8986 related to an AAR partnership, if the direct or indirect pass-through partner chooses to furnish statements to its reviewed-year partners to further push out adjustments or have adjustments that do not result in an IU

And any partner that receives IRS Form 8986 should file Form 8978 to reflect those adjustments and any imputed underpayment amounts.

What is a BBA partnership?

A BBA partnership is one that is subject to the new centralized partnership audit regime enacted into law by the Bipartisan Budget Act of 2015.

Under the BBA, the IRS generally assesses and collects any understatement of tax at the partnership level. This understatement is called an imputed underpayment, or IU, at the partnership level. As of 2018, all partnerships must file under the new centralized audit regime unless they elect out in a timely filed partnership return.

Partnerships may request to modify the imputed underpayment amounts and may elect to push out the adjustments underlying the IU instead of paying. They do this by filing IRS Form 8986.

What is IRC Section 6226?

IRC Section 6226, Alternative to payment of imputed underpayment by partnership, is the part of the tax code that enables a partnership to avoid penalties for tax underpayment by making a push-out election and issuing partnership adjustments to each partner.

What is IRC Section 6227?

IRC Section 6227, Administrative adjustment request by partnership, is the code section that provides guidance on how to make appropriate adjustments.

Who must file IRS Form 8978?

Any partner who receives IRS Form 8986 must file Form 8978 to reflect the proper tax liabilities from the partnership election, and to pay any additional tax due.

Generally speaking, partners use Form 8978 and Schedule A (Form 8978) to report adjustments shown on Forms 8986 received from partnerships that have elected to push out adjustments to partnership-related items to their partners.

However, this requirement does not apply to pass-through entities, such as S corporations or partnerships.

The Schedule A (Form 8978) lists all the adjustments a partner receives on Form 8986. Schedule A is also used to report any related amounts and adjustments not reported on Form 8986 which may result from changes to partner-level tax attributes because of adjustments made on Form 8986.

This includes both net positive adjustments and negative adjustments.

When is IRS Form 8978 due?

According to the Internal Revenue Service, a reviewed year partner or affected partner must submit their completed Form 8978 with a federal income tax return for the partner’s tax year.

What is a reviewed year partner?

A reviewed year partner is any person that held an interest in the audited partnership at any time during the partnership’s reviewed year. Reviewed year partners may have terminated their partnership before the end of the calendar year in question.

What is an affected partner?

An affected partner is a partner that held an interest in a pass-through partner at any time during the applicable tax year of the pass-through partner to which the adjustments in the statement relate.

Video walkthrough

This instructional video will walk you through this tax form, step by step.

Frequently asked questions

If you are required to complete Form 8978, you must also complete Schedule A. Schedule A helps calculate adjustments that go into Form 8978.

Since Form 8978 only contains 4 columns, if there are more than 4 years of adjustments, you must use a second form to record the additional adjustments.

Adjustments may occur as a result of administrative adjustment requests (AARs) or as part of an audit under the centralized partnership audit regime of the Bipartisan Budget Act of 2015 (BBA). If you have adjustments from both sources, you must report them separately on separate Forms 8978. Each Form 8978 should be checked ‘AAR’ or ‘BBA’ based upon the source of adjustment.

Where can I find a copy of IRS Form 8978?

You may download the latest versions of IRS forms from the IRS website. For ease of use, you can select the appropriate file(s) below.