IRS Form 8994 Instructions

In 2017, the Tax Cuts and Jobs Act provided a new tax credit for employers who pay for employees to take leave to attend to family and medical needs. Employers can file IRS Form 8994, Employer Credit for Paid Family and Medical Leave, to claim this tax credit.

In this article, we’ll walk through everything you need to know about IRS Form 8994, including:

- How to complete IRS Form 8994

- How to calculate the employer tax credit

- Frequently asked questions

Let’s start with step by step instructions on completing this tax form.

Table of contents

How do I complete IRS Form 8994?

This one-page tax form is relatively straightforward. Let’s begin at the top with the taxpayer information fields.

Taxpayer information

In this section, enter the taxpayer name (or names) as shown on your federal tax return. Additionally, enter the employer’s identifying number on the right side.

Questions

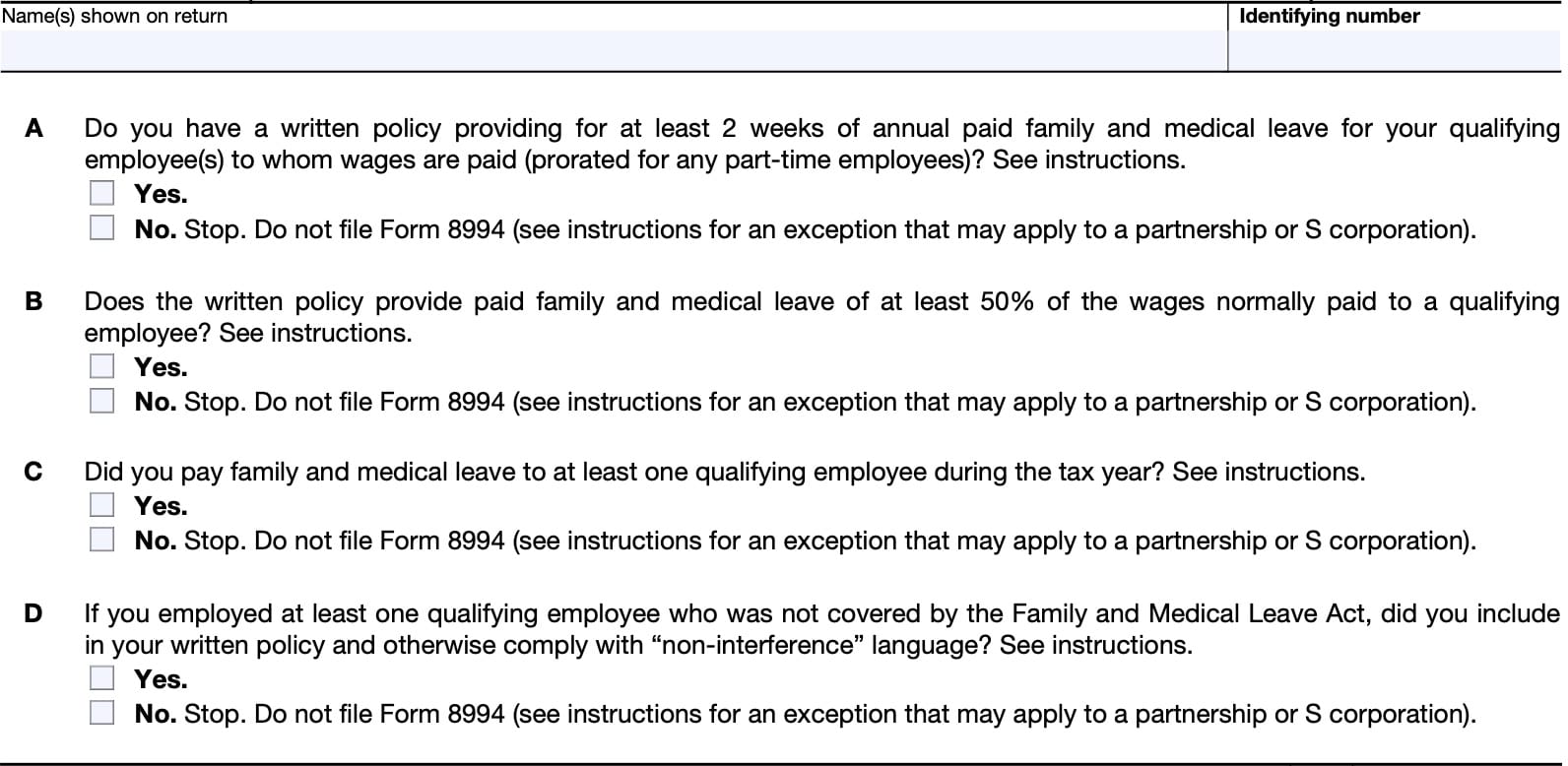

Before calculating any tax credit, you must answer four questions to determine if you are eligible for the employer credit in the first place. These questions help ensure that you meet the criteria for claiming this credit.

Line A

Do you have a written policy providing for at least 2 weeks of annual paid family and medical leave for your qualifying employee(s) to whom wages are paid?

If Yes, proceed to the next line. If No, then stop here. You cannot complete IRS Form 8994 unless you are filing this form for a partnership or S corporation that received a tax credit from another entity. You must report that tax credit on Line 2.

Minimum period of leave requirement

An employer’s written policy must provide qualifying full-time employees with at least 2 weeks of family and medical leave and must provide at least a proportionate amount of annual paid family and medical leave to qualified employees who are part-time employees.

For part-time employees, the paid leave ratio must be at least equal to the ratio of the expected weekly hours worked by a qualifying employee who is a part-time employee to the expected weekly hours worked by an equivalent qualifying employee who isn’t a part-time employee.

In determining the amount of paid family and medical leave benefit provided by the employer, any leave paid by state or local governments or required by state or local law isn’t taken into account.

Qualifying employees

A qualifying employee is an employee (as defined in Section 3(e) of the Fair Labor Standards Act of 1938 (FLSA), as amended) who:

- Has been employed by the employer for one year or longer, and

- Whose compensation for the preceding year does not exceed 60% of the highly compensated employee threshold for that year under Internal Revenue Code Section 414(q)(1)(B)(i).

Part-time employees

A part-time employee is an employee who is customarily employed for fewer than 30 hours per week.

Until the federal government issues further guidance, an employer may use any reasonable method to determine how many hours an employee customarily works per week for the employer.

Line B

Does the written policy provide paid family and medical leave of at least 50% of the wages normally paid to a qualifying employee?

If Yes, proceed to the next line. If No, then stop here. You cannot complete IRS Form 8994 unless you are filing this form for a partnership or S corporation that received a tax credit from another entity. You must report that tax credit on Line 2.

Family and medical leave

Family and medical leave generally means leave for any one or more FMLA purposes, as defined below. However, if an employer provides paid leave as vacation leave, personal leave, or medical or sick leave (other than leave specifically for one or more of the FMLA purposes), you cannot consider that paid leave to be part of the federal family and medical leave program.

FMLA purposes

The following reasons are FMLA purposes for which paid family and medical leave may be provided to a qualifying employee:

- The birth of a son or daughter of the employee and in order to care for the son or daughter.

- The placement of a child with the employee for adoption or foster care.

- Caring for the spouse, or a son, daughter, or parent of the employee, if the spouse, son, daughter, or parent has a serious health condition.

- A serious health condition that makes the employee unable to perform the functions of the employee’s position.

- Any qualifying exigency (as the Secretary of Labor shall, by regulation, determine) arising out of the fact that the spouse, or a son, daughter, or parent of the employee is a member of the U.S. Armed Forces (including the National Guard and Reserves) who is on covered active duty (or has been notified of an impending call or order to covered active duty).

- Caring for a service member with a serious injury or illness if the employee is the spouse, son, daughter, parent, or next of kin of the service member.

Minimum rate of payment requirement

The employer’s written policy must provide that each qualifying employee who is on paid family and medical leave will receive at least 50% of the wages normally paid to the employee for services performed for the employer.

In determining the rate of payment under the policy, leave paid by a state or local government or required under state or local law isn’t taken into account.

Wages normally paid to the employee

Wages normally paid to an employee means the wages normally paid to the employee for services performed for the employer. This does not include overtime or discretionary bonuses.

Line C

Did you pay family and medical leave to at least one qualifying employee during the tax year?

If Yes, proceed to the next line. If No, then stop here. You cannot complete IRS Form 8994 unless you are filing this form for a partnership or S corporation that received a tax credit from another entity. You must report that tax credit on Line 2.

Line D

If you employed at least one qualifying employee who was not covered by the Family and Medical Leave Act, did you include in your written policy and otherwise comply with non-interference language?

Answer Yes if you either:

- Did not employ any employees who weren’t covered by the FMLA, or

- Employed at least one employee who wasn’t covered by the FMLA and you included in your written policy and otherwise complied with “non-interference” language

If Yes, proceed to the next line. If No, then stop here. You cannot complete IRS Form 8994 unless you are filing this form for a partnership or S corporation that received a tax credit from another entity. You must report that tax credit on Line 2.

Non-interference language

If an employer employs at least one qualifying employee who isn’t covered by title I of the FMLA (including any employee who isn’t covered by title I of the FMLA because he or she works less than 1,250 hours per year), the employer must include “non-interference” language in its written policy and comply with this language to be an eligible employer. This

requirement applies to:

- An employer subject to title I of the FMLA that has at least one qualifying employee who isn’t covered by title I of the FMLA, and

- An employer not subject to title I of the FMLA (that has no employees covered by title I of the FMLA).

The “non-interference” language must ensure that the employer:

- Will not interfere with, restrain, or deny the exercise of, or the attempt to exercise, any right provided under the policy, and

- Will not discharge, or in any other manner discriminate against any individual for opposing any practice prohibited by the policy.

Example

The following is an example of a written provision that would satisfy this requirement

[Employer] will not interfere with, restrain, or deny the exercise of, or the attempt to exercise, any right provided under this policy. [Employer] will not discharge, or in any other manner discriminate against, any individual for opposing any practice prohibited by this policy.

Calculating the tax credit

In Lines 1 through 3, we’ll calculate the amount of credit that you can claim in the taxable year.

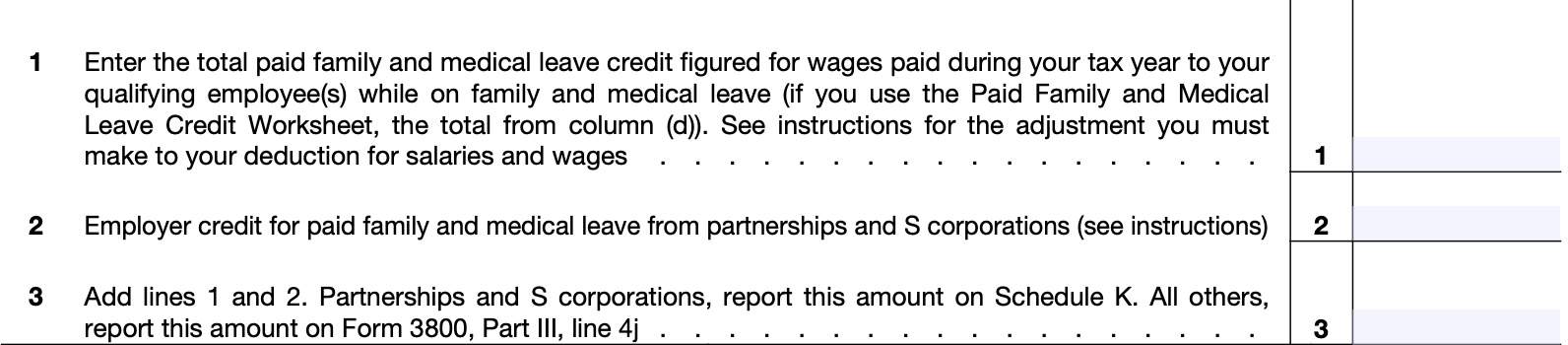

Line 1

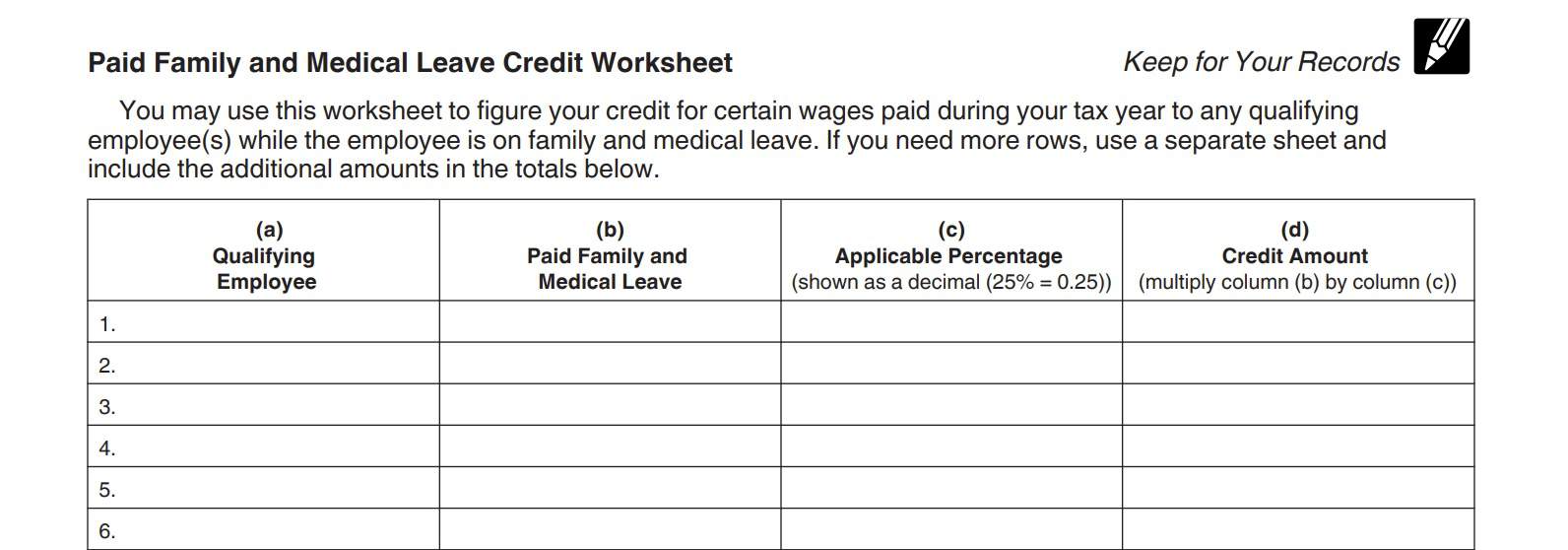

Enter the total paid family and medical leave credit calculated for the amount of wages paid during your tax year to your qualifying employee(s) while on family and medical leave. If you used the Paid Family and Medical Leave Credit Worksheet, this represents the amount from Column (d).

In general, you must reduce your deduction for salaries and wages by the amount on Line 1. You must make this reduction even if you can’t take the full credit this year and must:

- Carry it back to prior years

- Carry it forward to future tax years

If you capitalized any costs on which you figured the credit, reduce the amount capitalized by the credit attributable to these costs.

Paid Family and Medical Leave Credit Worksheet

You may need to use the paid family and medical leave credit worksheet to calculate the amount of tax credit for wages paid during the tax year. Let’s take a look at how to complete each column.

Column (a): Qualifying Employee

For each qualifying employee, the person’s name or other identifying information.

Column (b): Paid Family and Medical Leave

In this column, enter the total family and medical leave wages paid during the year for each employee in Column (a).

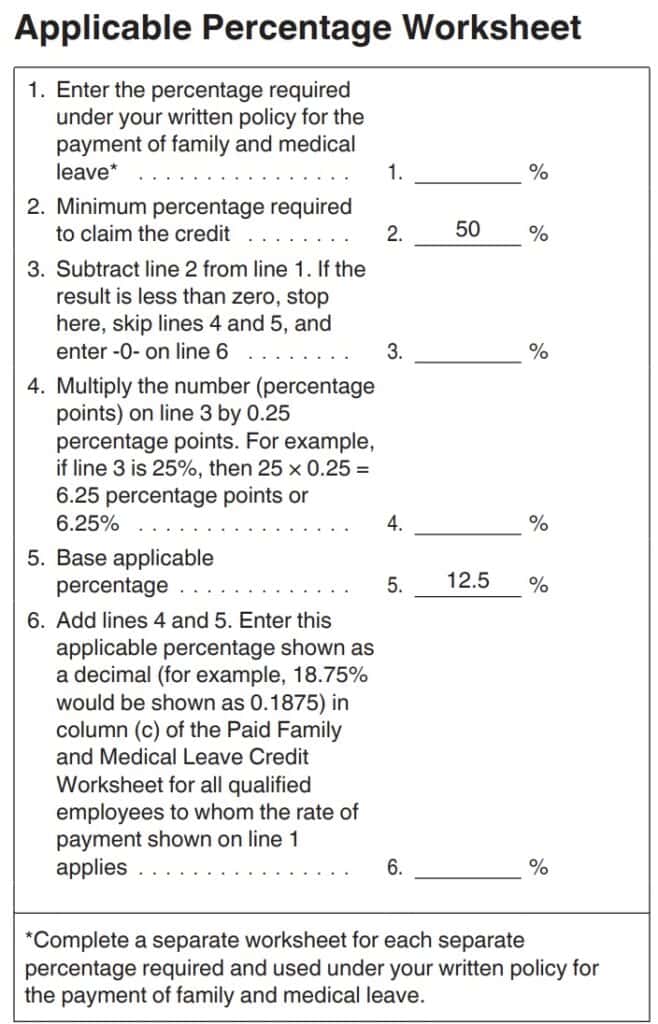

Column (c): Applicable Percentage

Enter the applicable percentage.

The applicable percentage is based on the rate of payment for the leave under the employer’s policy.

The base applicable percentage of 12.5% applies if the rate of payment is 50%. If the rate of payment under the policy is greater than 50%, the applicable percentage increases by 0.25 percentage points for each percentage point. The maximum applicable percentage is 25%.

You can either calculate the applicable percentage manually or by using this applicable percentage worksheet.

Note: If you have more than one applicable percentage used under your written policy, you may need to complete a separate worksheet for each percentage used.

Column (d): Credit Amount

Multiply column (b) by column (c). This is the credit amount for that particular employee.

Line 2

In Line 2, enter the total paid family and medical leave credits from either of the following federal tax returns:

- IRS Form 1065, Schedule K-1, Box 15, Code P, or

- IRS Form 1120-S, Box 13, Code P

Partnerships and S corporations should report these credits on Line 2. Additionally, other filers calculating a separate credit on Line 1, above should report those credits on Line 2.

Other taxpayers not using Line 1 must report this as part of the general business credit on IRS Form 3800, Part III, Line 4j.

Line 3

Add Line 1 and Line 2.

Partnerships and S corporations should report this amount on Schedule K. All other taxpayers report this on IRS Form 3800, Part III, Line 4j.

Video walkthrough

Watch this instructional video to learn more about using Form 8994 to claim an employer credit for paid family and medical leave.

Do you use TurboTax?

If you don’t, is it because the choices are overwhelming to you?

If so, you should check out our TurboTax review page, where we discuss each TurboTax software product in depth. That way, you can make an informed decision on which TurboTax offering is the best one for you!

Click here to learn more about which TurboTax option is best for you!

Frequently asked questions

Eligible employers use IRS Form 8994 to calculate the amount of tax credit that may be claimed on an employer’s annual federal tax return for providing paid family and medical leave to qualifying employees.

The Taxpayer Certainty and Disaster Tax Relief Act of 2020 extended the paid family and medical leave tax credit to cover tax years beginning in 2021 through 2025.

Where can I find IRS Form 8994?

As with other federal income tax forms, you can find IRS Form 8994 on the IRS website. For your convenience, we’ve included the most recently updated Form 8994 here, in our article.