IRS Form W-12 Instructions

If you’re looking to register as a paid tax return preparer, then you may need to complete IRS Form W-12, IRS Paid Preparer Tax Identification Number (PTIN) Application and Renewal. In this article, we’ll cover everything you need to know about IRS Form W-12, including:

- How to complete IRS Form W-12

- Filing considerations

- Frequently asked questions

Let’s begin by breaking down this tax form, step by step.

Table of contents

How do I complete IRS Form W-12?

This three-page tax form appears to be pretty straightforward. Let’s start at the top of the first page.

Line 1: Name and PTIN

Enter your legal name. This entry should reflect your name as it appears on your tax return and as it will be entered on tax returns that you are paid to prepare.

If you are renewing your PTIN, enter the PTIN you received after you first filed Form W-12. Also, check the appropriate box:

- Initial application

- Renewal application

Voluntarily inactivate PTIN

An individual who does not expect to prepare federal tax returns for compensation for a

full calendar year may request to be placed in an inactive status.

You can inactivate your PTIN by:

- Accessing your online PTIN account

- Selecting the Inactivate PTIN function under the Manage My PTIN Account section

Tax preparers can reactivate their PTIN within 3 years by selecting the Reactivate PTIN function within their online PTIN account.

If you do not have an online IRS account

If you do not have an online account, you can call the IRS telephone number as listed below:

- Calling from the United States: (877) 613-PTIN (7846)

- TTY/TDD assistance: (877) 613-3686

- Internationally: +1 (915) 342-5655 (not a toll-free number)

You may contact the Internal Revenue Service for assistance Monday through Friday, between 8:00 AM and 5:00 PM, Central Time.

Enrolled agents

Enrolled agents (EAs) must maintain a current PTIN in order to maintain their EA credential. EAs should not inactivate their PTIN unless they retire.

Line 2: Year of application/renewal

Enter the year of your application or renewal in Line 2.

If you are applying for a new PTIN after October 1, you must indicate whether you want your PTIN to be valid for the current calendar year or the next calendar year.

When selecting the current calendar year, your PTIN is valid until December 31 of the current year. If you select the following year, your PTIN will not be valid until January 1 of the next calendar year.

Note: If you do not select any calendar year, then the IRS will process your PTIN application for the current year.

Prior-year renewals

If you checked the “Renewal application” box in Line 1 and need to renew for a prior calendar year, then indicate this by:

- Entering the year (in YYYY format) in the ‘Prior Year’ box, and

- Listing each prior year in the space(s) provided

Complete a single Form W-12 for multiple calendar years, for which you are applying for a prior-year PTIN.

If your PTIN has been in an expired status for more than 1 full calendar year, you must renew for each previously expired year unless you were inactive during any one of those calendar years.

Inactive status

If you were inactive during any one of those prior calendar years but did not place your PTIN into voluntary inactive status, you can retroactively do so by following the instructions under Voluntarily Inactivate PTIN, earlier.

If your PTIN has been inactive or expired for more than 3 consecutive years, you must submit a new registration application to obtain an active PTIN.

Line 3: SSN and Date of Birth

Enter your social security number (SSN) and date of birth in Line 3. First-time PTIN applicants must be at least 18 years of age to apply.

Applying without an SSN

If you do not have an SSN because you are either a U.S. citizen who is a conscientious religious objector or a foreign individual, you will need to complete and submit additional information either online or by mail in order to obtain a PTIN.

U.S. citizen who is a conscientious religious objector

If you are a U.S. citizen who does not have an SSN because you have a conscientious religious objection to having an SSN, you must complete IRS Form 8945, PTIN Supplemental Application For U.S. Citizens Without a Social Security Number Due To Conscientious Religious Objection.

On IRS Form 8945, you will verify information about your identity, citizenship, and conscientious religious objection.

Foreign persons

If you are a foreign person who does not have an SSN, you must provide additional identity documents as part of the PTIN application process.

A foreign person is an individual who:

- Does not have and is not eligible to obtain an SSN, and

- Is neither a citizen of the United States nor a resident alien of the United States as defined in Internal Revenue Code Section 7701(b) (1)(A).

You can apply online or complete Form 8946, PTIN Supplemental Application For Foreign Persons Without a Social Security Number. On IRS Form 8946, you will verify information about your foreign status and identity.

You must enter your SSN if you have been assigned one since obtaining your PTIN. If you still do not have an SSN, check the N/A box.

Line 4: Personal mailing address and phone number

Enter your complete personal mailing address and telephone number.

Your address must be outside the United States if you obtained your PTIN using Form 8946 and you still do not have a SSN.

If the Postal Service will not deliver mail to your address

If the U.S. Postal Service will not deliver mail to your physical location, enter the U.S. Postal Service post office box number for your mailing address.

Contact your local U.S. Post Office for more information. DO NOT use a post office box owned by a private firm or company.

Most PTIN correspondence will be sent to your email address. However, any paper PTIN correspondence will be sent to the personal mailing address listed on Line 4.

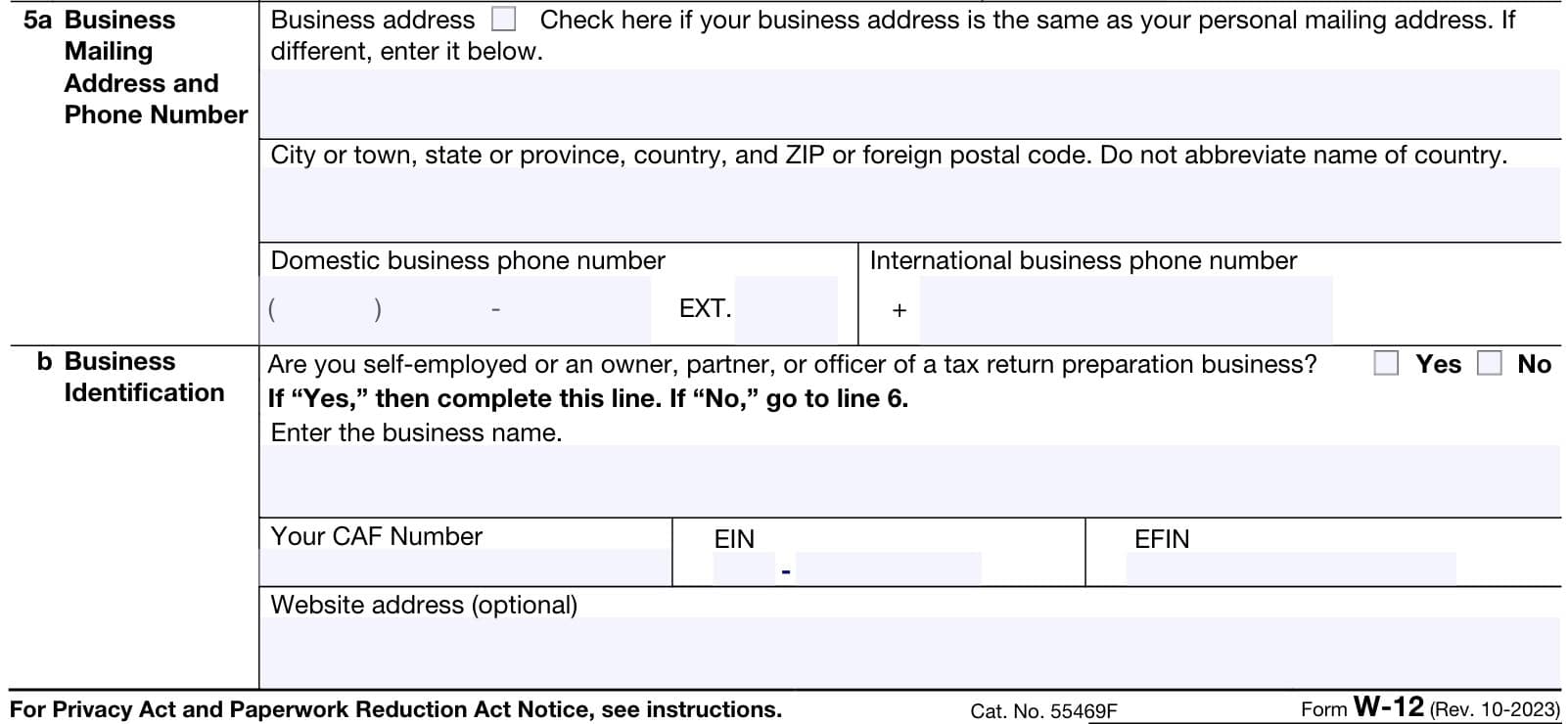

Line 5a: Business mailing address and phone number

Enter your business address if it is different from the address entered on Line 4. Entering the business phone number is optional.

If you obtained your PTIN using IRS Form 8946 and you still do not have a SSN, your address must be outside the United States.

Directory of Federal Tax Return Preparers with Credentials and Select Qualifications

The business address listed on Line 5a will be reflected in the online Directory of Federal Tax Return Preparers with Credentials and Select Qualifications if you meet the qualifications for inclusion.

If you have more than one business location, enter your primary business location address.

Line 5b: Business identification

Check Yes or No, depending on whether you are self-employed, or are an owner, partner, or officer of a tax return preparation business. If you are self-employed or an owner, partner, or officer of a tax return preparation business, enter the business name and your applicable identification numbers.

Entering the business website address is optional.

Centralized Authorization File (CAF) Number

A CAF number is a unique nine-digit identification number and is assigned the first time you file a third party authorization with IRS. The IRS grants third party authorization based upon information provided in either of the following documents:

- IRS Form 2848, Power of Attorney and Declaration of Representative: This form allows a taxpayer to delegate certain representation authority to another individual.

- IRS Form 8821, Tax Information Authorization: This form allows a taxpayer to authorize a third party to receive certain tax information from the IRS. IRS Form 8821 does not authorize the third party to assume any representation authority

The IRS will send you a letter informing you of your assigned CAF number.

CAF numbers are different from the third party’s TIN (Taxpayer Identification Number), EIN (Employer Identification Number) or PTIN (Preparer Identification Number). CAF numbers may be assigned to an individual or a business entity.

Be sure to enter any letters that are part of your CAF number.

Employer identification number (EIN)

An employer identification number (EIN) is also known as a federal tax identification number, and is used to identify a business entity. Taxpayers may apply for an EIN through the IRS website or by filing IRS Form SS-4, Application for Employer Identification Number.

Watch this brief video to learn more about filing Form SS-4 to obtain an EIN.

Electronic filer identification number (EFIN)

Paid tax return preparers must obtain an electronic filer identification number (EFIN). To apply for an EFIN, you must establish an IRS account, then submit an online application through your account.

If you have multiple Employer Identification Numbers (EINs) or Electronic Filer Identification Numbers (EFINs), enter the number that is used most frequently on returns you prepare.

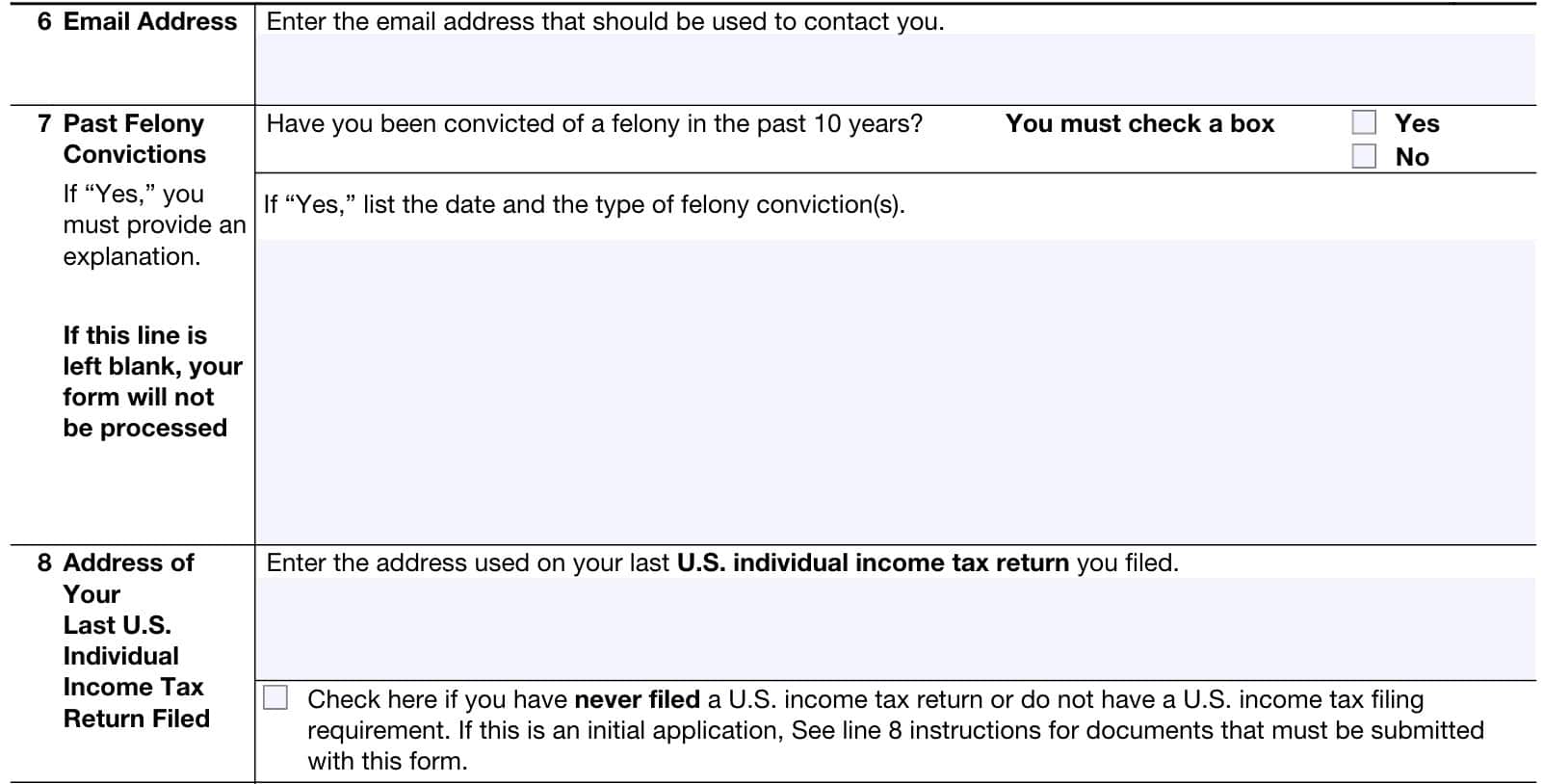

Line 6: Email address

Enter the email address we should use if we need to contact you about matters regarding your completed Form W-12.

The IRS will also send PTIN related emails with general information, reminders, and requirements. Any valid email address that you check regularly for PTIN communications is acceptable.

Line 7: Past felony convictions

Check Yes or No. This is not an optional question.

You must fully disclose any information concerning prior felony convictions. A felony conviction may not necessarily disqualify you from having a PTIN. However, generally, an individual who is currently incarcerated for any felony conviction will not be permitted to obtain or renew a PTIN.

Use the space provided to enter details of your prior felony conviction(s). The IRS will consider all facts and circumstances surrounding your felony conviction, and will contact you if additional information is required.

If this line is left blank the IRS will not process your PTIN application.

Providing false or misleading information on this form is a criminal offense that may result in prosecution and criminal penalties.

Line 8: Address of your last U.S. Individual Income Tax Return Filed

In Line 8, enter the address that you used for your most recent federal income tax return.

If you have an SSN and are requesting a PTIN but have never filed a U.S. income tax return, check the box and see below for additional requirements.

Never filed a U.S. tax return

If you have an SSN and are applying for a PTIN and any of the statements below apply to your current U.S. situation, then you must submit a paper PTIN application along with two identity verification documents:

- You have never filed a U.S. income tax return.

- You have not filed a U.S. income tax return in the past 4 years.

- You do not have a U.S. income tax filing requirement (such as certain individuals from Puerto Rico)

You must submit an original or notarized copy of your social security card along with an original, or notarized copy of one other government-issued document that contains a current photo ID. Below are acceptable copies:

- Passport or passport card.

- State-issued driver’s license.

- U.S. state identification card.

- Military ID card

- National ID card

When submitting supporting ID documentation, you can either submit online or by mail.

Online submissions

To submit supporting ID documents online, follow the online prompts to upload notarized copies of acceptable documentation.

Submitting documents by mail

Documents must be original or notarized.

One document must be government-issued and contain a current photo ID. All documents must be current (not expired), and must verify your name.

Notarized document requirements

Instead of sending original documents, you may send notarized copies.

A notarized copy is one that has been notarized by one of the following:

- U.S. notary public

- U.S. government military officer (such as a legal officer or JAG officer)

- U.S. State Department or Consul/Embassy employee

- Notary legally authorized within his or her local jurisdiction

To properly notarize a document, the notary must see the valid, unaltered, original documents and the copies must bear the notary’s mark. Notarized documents may or may not have a signature but will have a stamp and usually a raised seal.

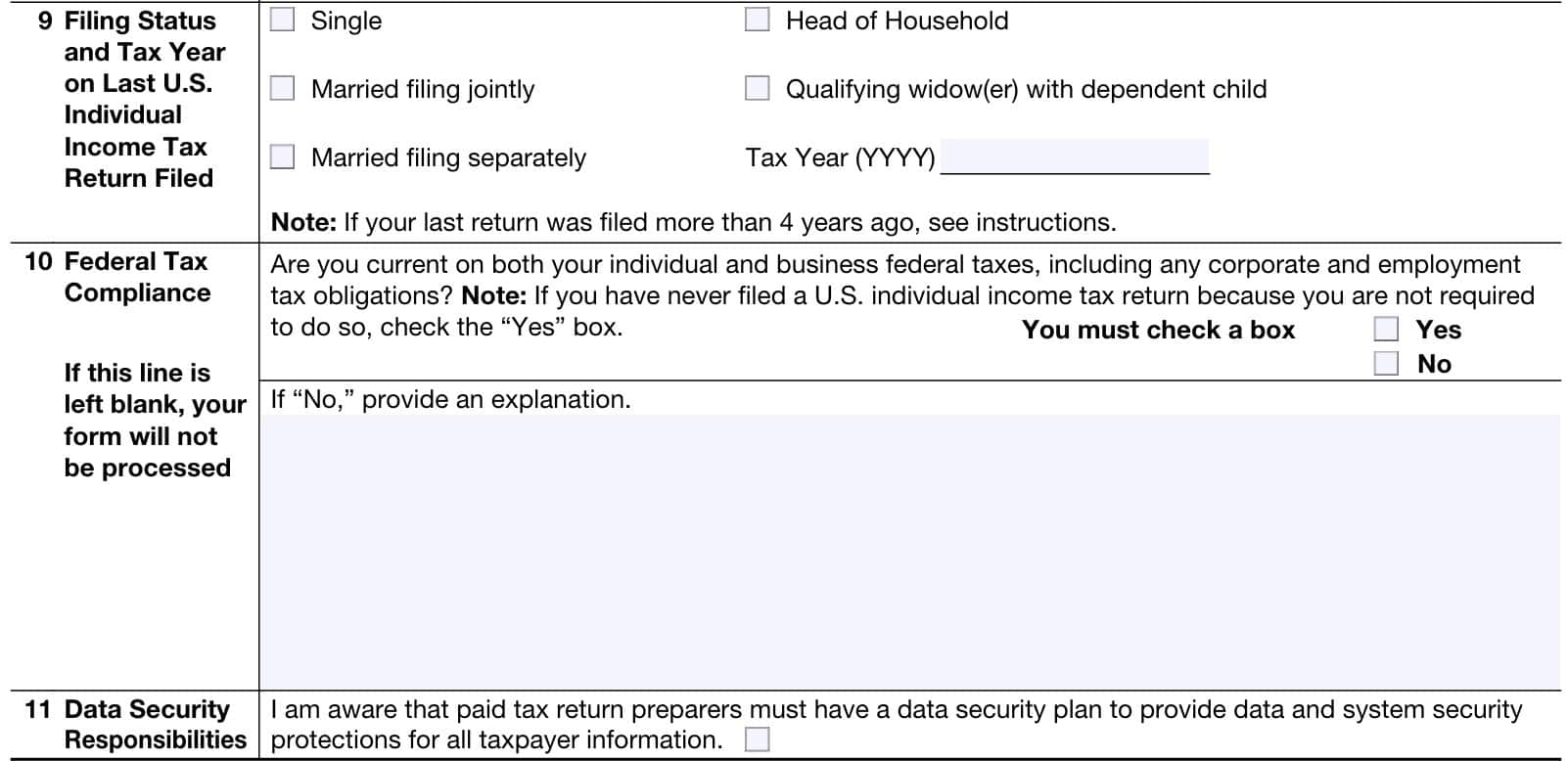

Line 9: Filing Status and Tax Year on Last U.S. Individual Income Tax Return Filed

Check the box that corresponds to your ta filing status on your most recent income tax return:

- Single

- Married filing jointly

- Married filing separately

- Head of household

- Qualifying widow(er) with dependent child

Enter the year of your most recent tax return.

If you filed your most recent individual income tax return more than 4 years ago, see the Line 8 instructions above for separate instructions on how to submit Form W-12 and the supporting

identification documents that must accompany your submission.

Line 10: Federal Tax Compliance

Check the appropriate box to indicate whether you are current on your individual and business federal tax requirements. This includes corporate and employment tax obligations.

If you have never filed a U.S. individual income tax return because the IRS does not require you to do so, then check Yes.

If you check No, then you must provide a written explanation in the space provided.

The IRS will not process your PTIN application if you leave this line blank.

Federal tax compliance requirements

Taxpayers must be in full compliance with federal tax laws. This includes the following:

- Filing all required tax returns

- Paying applicable taxes or making payment arrangements that are acceptable to the IRS

The filing of a tax return and the payment of the tax liability associated with that return are two separate and distinct requirements under the Internal Revenue Code. Taxpayers must satisfy each requirement within the periods specified for each taxable period in which you have a legal obligation to file.

Line 11: Data Security Responsibilities

Check the box to confirm awareness of your responsibility to protect taxpayer information.

You may find more complete information in the following publications:

Enrolled Agents who do not prepare returns may skip Line 11.

Line 12: Professional Credentials

Check the appropriate boxes to indicate your professional credentials. Check all boxes that apply.

Be sure to include the following information:

- Licensing number

- Jurisdiction

- Expiration date

If the expiration date is left blank or incomplete, that specific credential will not be added during the processing of your application.

Select only from the professional credentials listed below. There is no write-in option for credentials. If you do not have any professional credentials, check the ‘None’ box.

The IRS will recognize the tax professionals described below.

Attorney

An attorney is any individual who is licensed to practice law by the bar of the highest court of any state, territory, or possession of the United States, including a commonwealth, or the District of Columbia.

Certified public accountants

A certified public accountant (CPA) is any individual who is duly qualified to practice as a CPA in any state, territory, or possession of the United States, including a commonwealth, or the District of Columbia.

Enrolled agent

An EA is any individual enrolled as an agent who is not currently under suspension or disbarment from practice before the IRS. The enrolled agent credential is awarded licensed by the IRS.

Enrolled actuary

An enrolled actuary is any individual who is enrolled as an actuary by the Joint Board for the Enrollment of Actuaries.

Enrolled retirement plan agent

An enrolled retirement plan agent (ERPA) is any individual enrolled as a retirement plan agent who is not currently under suspension or disbarment from practice before the IRS.

State regulated tax return preparer

A state regulated tax return preparer is any individual who remains current with certain state-based tax return preparer programs. Tax return preparers who are registered with the following will fall into this category.

- Oregon Board of Tax Practitioners

- California Tax Education Council

- Maryland State Board of Individual Tax Preparers

Certifying acceptance agent

A certifying acceptance agent (CAA) is an individual or entity (college, financial institution, accounting firm, etc.) that has entered into a formal agreement with the IRS that permits them to assist alien individuals and other foreign individuals with obtaining Individual Taxpayer Identification Numbers.

A CAA cannot verify documents in order for individuals to obtain a PTIN.

CAAs should enter either their EFIN or the eight-digit office code assigned to them via the CAA application process.

Expired or retired credentials

Do not check any professional credentials that are currently expired or retired. Retired or expired credentials are those that are not valid or active at the time of the PTIN application.

Line 13: Fees

The application fee is a nonrefundable application processing fee. For 2024, the PTIN fee is $19.75.

Payment of the application registration/renewal fee(s) must accompany this form or it will be rejected.

PTIN Registration/Renewal Fees

- If you are applying for a valid PTIN in order to prepare federal tax returns beginning calendar year 2024, the registration/renewal fee is $19.75.

- If you are registering or renewing a PTIN for tax years 2021 – 2023, the PTIN fees are $19.75 for each year.

- If you are registering or renewing a PTIN for 2020 or any other prior year, there is no registration or PTIN renewal fee.

- You must submit a separate check or money order for each calendar year. Indicate the calendar year you intend the PTIN payment for on each check or money order.

- Make your check or money order payable to IRS Tax Pro PTIN Fee for the correct fee amount required based on the calendar year(s) you are registering or renewing your PTIN.

- Do not paper clip, staple, or otherwise attach the payment to your completed Form W-12.

- If your payment is returned your PTIN will be placed in Suspended status.

- You are responsible for submitting the proper payment to place your PTIN in active status

Signature

At the bottom of your Form W-12, enter your sworn signature in blue or black ink. Enter the date in MM/DD/YYYY format.

Filing considerations

Below are additional filing considerations for those who are attempting to file IRS Form W-12.

Who must file IRS Form W-12?

Anyone who is a paid tax return preparer must apply for and receive a PTIN annually. EAs also must obtain a PTIN and renew it on an annual basis.

For purposes of determining who must obtain a PTIN, a tax return preparer is any individual who receives compensation for preparing, or assisting in the preparation of, all or substantially all of a tax return or claim for refund of tax.

How do I file IRS Form W-12?

You may file Form W-12 online or by mail.

Online application

Go to the IRS’ PTIN page for additional information and follow the instructions to submit Form W-12.

If you submit your application and payment online, your PTIN generally will be provided to you immediately after you complete the application.

Application by mail

Complete and print IRS Form W-12. Send paper applications and payment to the following location:

IRS Tax Professional PTIN Processing Center

PO Box 380638

San Antonio, TX 78268

Allow 6 weeks for processing of PTIN applications.

Video walkthrough

Watch this instructional video for a step by step demonstration of IRS Form W-12.

Frequently asked questions

IRS Form W-12, IRS Paid Preparer Tax Identification Number (PTIN) Application and Renewal, is the tax form that paid tax return preparers use to obtain or renew their PTIN in the IRS’ PTIN system. Return preparers must file Form W-12 annually to maintain their PTIN.

Any professional who receives compensation for preparing, or assisting in the preparation of, all or substantially all of a tax return or claim for refund of tax must apply for a PTIN. Also, enrolled agents must maintain a PTIN to keep their enrolled agent credential.

Yes. IRS Form W-12 can be used to obtain a new PTIN or renew an existing PTIN.

Where can I find IRS Form W-12?

You may find IRS forms on the IRS website. For your convenience, we’ve enclosed the latest version of IRS Form W-12 in this article.