IRS Schedule 2 Instructions

After Congress passed the Tax Cuts and Jobs Act into federal law in 2017, the Internal Revenue Service created several new schedules to help taxpayers filing their individual tax return. One of them, IRS Schedule 2, was created to help taxpayers report and consolidate different types of additional taxes into one place on their tax return.

In this article, we’ll help you better understand IRS Schedule 2, including:

- How to complete & file IRS Schedule 2

- Relevant documentation you should file with IRS Schedule 2

- Frequently asked questions about additional taxes

Let’s start with a step by step walkthrough of this new form.

Table of contents

How do I complete IRS Schedule 2?

There are two parts to this two-page tax form:

Let’s start at the top of Part I.

Part I: Tax

Before we start with Line 1, you’ll need to enter your name as shown on your federal income tax return.

Also, enter your Social Security number (SSN) in the space provided. For taxpayers who do not have a Social Security number, enter your individual taxpayer identification number (ITIN), instead.

For taxpayers using tax preparation to file your individual tax return, your personal information might auto-populate on this part of the form as needed.

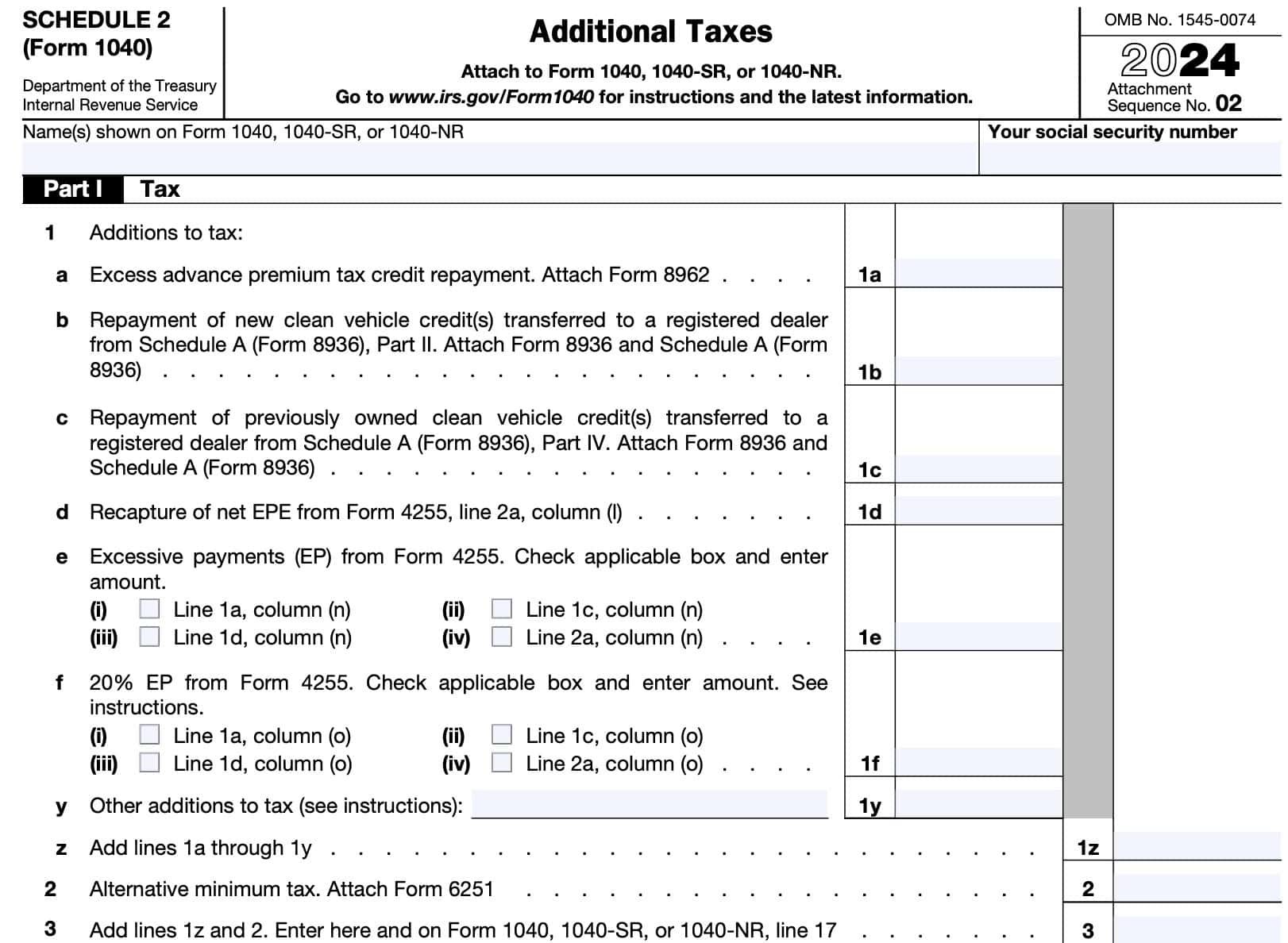

Line 1: Additions to tax

Beginning in 2024, this portion of Schedule 2 appears to be different from prior years. We’ll go through the additions to tax in order.

Line 1a: Excess advance premium tax credit repayment

Attach IRS Form 8962, and add any excess advance premium tax credit repayment.

The premium tax credit helps pay premiums for health insurance purchased from the Marketplace. Eligible individuals may have advance payments of the premium tax credit paid on their behalf directly to the insurance company.

If you or your spouse participated in health coverage from the Marketplace, then you may need to complete Form 8962 to reconcile your advance payments with your premium tax credit.

If the advance credit payments were more than the premium tax credit you can claim, the amount you must repay will be shown on Form 8962, Line 29. Enter this amount on Line 1a.

Line 1b: Repayment of new clean vehicle credits transferred to a registered dealer

If you purchased a new clean vehicle from a registered dealer and reduced the amount you paid at the time of sale by transferring the credit to the dealer, you may have to repay the amount of the credit you transferred if you no longer qualify.

Enter the amount from Part I, Line 4a on Schedule 2, Line 1b if you completed IRS Form 8936, Schedule A, Part II and you:

- Checked the “Yes” box on Part II, Line 8a or 8d; and

- Checked the “Yes” box on Part I, Line 4a;

If you completed more than one Schedule A (Form 8936), Part II, and you need to report an amount from more than one Schedule A (Form 8936), Part II, enter the total of those amounts on Line 1b.

Line 1c: Repayment of previously owned clean vehicle credits transferred to a registered dealer

If you purchased a previously owned clean vehicle from a registered dealer and reduced the amount you paid at the time of sale by transferring the credit to the dealer, you may have to repay the amount of the credit you transferred if you no longer qualify.

Enter the amount from Part I, Line 4a on Schedule 2, Line 1c if you completed IRS Form 8936, Schedule A, Part IV and you:

- Checked the “Yes” box on Part II, Line 13a or 13c; and

- Checked the “Yes” box on Part I, Line 4a;

If you completed more than one Schedule A (Form 8936), Part IV, and you need to report an amount from more than one Schedule A (Form 8936), Part IV, enter the total of those amounts on Line 1c.

Line 1d: Recapture of net EPE from IRS Form 4255

Enter any amount of net elective payment election (EPE) recapture from IRS Form 4255, Line 2a, Column (l).

Line 1e: Excessive payments (EP) from IRS Form 4255

If you reported an amount on IRS Form 4255, Column (n) on Line 1a, 1c, 1d, and/or 2a,

check the applicable box and enter the amount on Line 1e.

If you checked more than one box, enter the total amount on Line 1e.

Line 1f: 20% EP from IRS Form 4255

If Form 4255, Column (o), Line 1a, 1c, 1d, and/or 2a includes an additional 20% EP that you owe (calculated as 20% of the total EP before figuring the 20% EP), check the applicable box and enter the 20% EP amount included on Line 1f.

Enter only the 20% EP from Column (o) on Line 1f. If you checked more than one box, enter the total of the 20% EP amounts from each box on Line 1f.

Any other EP amounts reported on Form 4255, Column (o), Lines 1a, 1c, 1d, and/or 2a should be included on Line 1y, below.

Line 1y: Other additions to tax

Enter the following additions to tax:

- Recapture of the alternative fuel vehicle refueling property credit reported on IRS Form 8911

- Identify as “ARPCR.”

- Any EPE related to the credit applied against tax from IRS Form 8933 reported on Form 4255, Line 2a, Column (k).

- Identify as “EPE8933.”

- Recapture of any non-EPE credit from IRS Form 8933 reported on Form 4255, Line 2a, Column (j). Also, any Section 6418(g)(3) amounts attributable to recapture from Form 8933 reported on Form 4255, Line 2a, Column (m).

- Identify as “NEPE8933.”

- Any amount from IRS Form 4255, Column (o) that was not reported on Line 1f.

- Identify as “EPGEPE.”

- Any Section 6418(g)(2) excessive credit transfer amount reported on Form 4255, Column (m).

- Identify as “6418(g)(s)

Line 1z

Add Lines 1a, 1b, 1c, 1d, 1e, 1f, and 1y. Enter the total in Line 1z.

Line 2: Alternative minimum tax

In Line 2, enter the amount of alternative minimum tax from IRS Form 6251.

Worksheet to see if you should fill in Form 6251

If you do not know if you owe alternative minimum tax, or AMT, you may need to complete the following worksheet to help decide whether or not to complete IRS Form 6251.

However, if you claimed or received any of the following, then you must complete IRS Form 6251, regardless of whether you fill out the worksheet:

- Accelerated depreciation

- Tax-exempt interest from private activity bonds

- Intangible drilling, circulation, research, experimental, or mining costs

- Amortization of pollution-control facilities or depletion

- Income or (loss) from tax-shelter farm activities, passive activities, partnerships, S corporations, or activities for which you aren’t at risk

- Income from long-term contracts not figured using the percentage-of-completion method

- Investment interest expense reported on IRS Form 4952

- Net operating loss deduction

- Alternative minimum tax adjustments from an estate, trust, electing large partnership, or cooperative

- Section 1202 exclusion

- Stock by exercising an incentive stock option and you didn’t dispose of the stock in the same year

- Any general business credit claimed on IRS Form 3800 if either Line 6 (in Part I) or Line 25 of Form 3800 is more than zero

- Qualified electric vehicle credit

- Alternative fuel vehicle refueling property tax

- Credit for prior year minimum tax

- Foreign tax credit

- Net qualified disaster loss and you are reporting your standard deduction on Schedule A, line 16

Line 3

Add Line 1 and Line 2. Enter the sum here and on Line 17 of your U.S. individual income tax return:

- IRS Form 1040

- IRS Form 1040-SR

- IRS Form 1040-NR

When complete, move on to Part II.

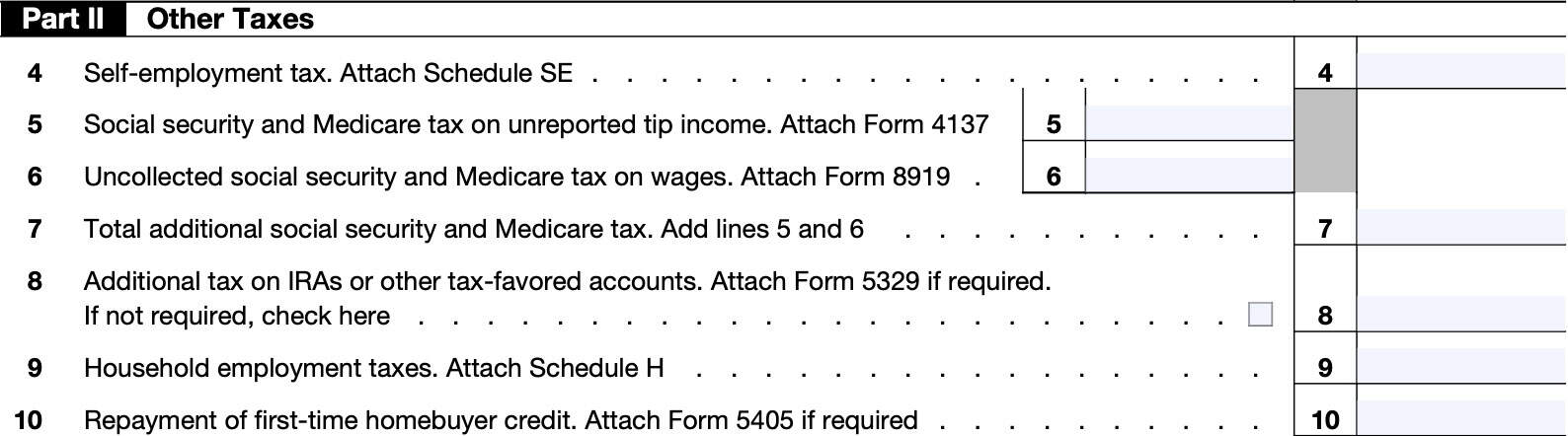

Part II: Other Taxes

In Part II, we’ll calculate other taxes that you’ll then enter in a different part of your Form 1040. Let’s start with self-employment taxes on Line 4.

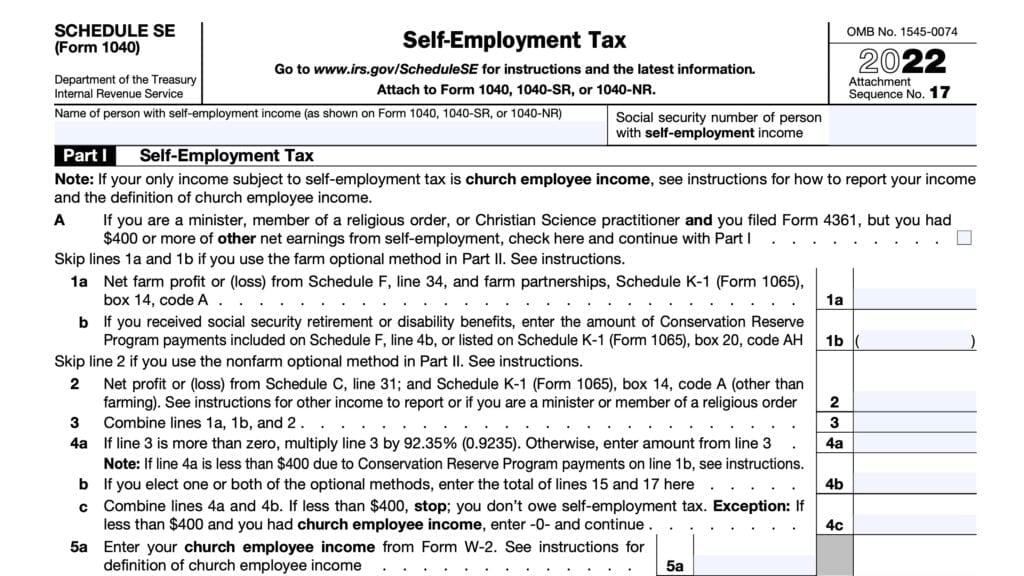

Line 4: Self-employment tax

In Line 4, enter the amount of self-employment tax from Schedule SE.

Line 5: Social Security and Medicare tax on unreported tip income

In Line 5, enter the amount of Social Security tax and Medicare tax you owe on unreported tip income. Most taxpayers calculate this on IRS Form 4137.

If you received tips of $20 or more in any month and you didn’t report the full amount to your employer, you must pay the social security and Medicare or railroad retirement (RRTA) tax on the unreported tips.

Don’t include the value of any noncash tips, such as tickets or passes. The federal government does not expect you to pay social security and Medicare taxes or RRTA tax on noncash tips.

Line 6: Uncollected Social Security and Medicare tax on Wages

If you have uncollected Social Security or Medicare tax on your earned income, you may need to file IRS Form 8919 to figure your share of the unreported tax.

If so, enter the amount from Line 13 of your completed Form 8919 on Line 6.

Line 7: Total Additional Social Security and Medicare Tax

In Line 7, enter the total additional Social Security and Medicare taxes that you owe.

To reach this number, add the values of Line 5 and Line 6. Enter the sum here.

Line 8: Additional tax on IRAs or other tax-favored accounts

You may need to file IRS Form 5329 to calculate additional taxes if any of the following apply:

- You received an early distribution from:

- An IRA or other qualified retirement plan

- An annuity, or

- A modified endowment contract entered into after June 20, 1988, and the total distribution wasn’t rolled over

- You made excess contributions were made to one of the following accounts:

- IRA

- Coverdell education savings account (ESA)

- Archer MSA

- Health savings account (HSA), or

- ABLE account

- You received a taxable distribution from a Coverdell ESA, qualified tuition program (or 529 plan), or ABLE account

- You didn’t take the minimum required distribution from your IRA or other qualified plan by April 1 of the year following the year you reached age 72.

If you must file Form 5329, attach the completed form and enter the amount into Line 8. Otherwise, check the block indicating that you do not need to complete Form 5329.

Line 9: Household employment taxes

Enter the amount of employment taxes you owe for having a household employee. If you do not know whether you have a household employee, you may need to determine the status of any persons you hire to work in your house.

Determining household employee status

Any person who does household work is a household employee if you can control the following parameters:

- What work will be done

- How that work gets done

Examples of household work include work that is done in, or around your home by:

- Babysitters & nannies

- Home health workers

- Housekeepers

- Yard workers or other similar domestic workers

Generally, you will need to complete Schedule H and pay any additional taxes if any of the following apply to your specific tax situation:

- You paid any one household employee (defined below) cash wages of $2,400 or more in the given tax year.

- Cash wages include wages paid by check, money order, etc.

- Don’t count amounts paid to an employee who was under age 18 at any time in 2024 and was a student.

- You withheld federal income tax during the tax year at the request of any household employee

- You paid total cash wages of $1,000 or more in any calendar quarter to household employees

If applicable, enter the amount of household taxes you owe into Line 9.

Line 10: Repayment of first-time homebuyer tax credit

If you bought a home in 2008, enter the amount of the first-time homebuyer credit you have to repay in the tax year.

If you bought the home in 2008, and used it as your primary residence for the entire tax year, you can enter the repayment for the current tax year without completing IRS Form 5405. Otherwise, enter the amount from your completed Form 5405 here.

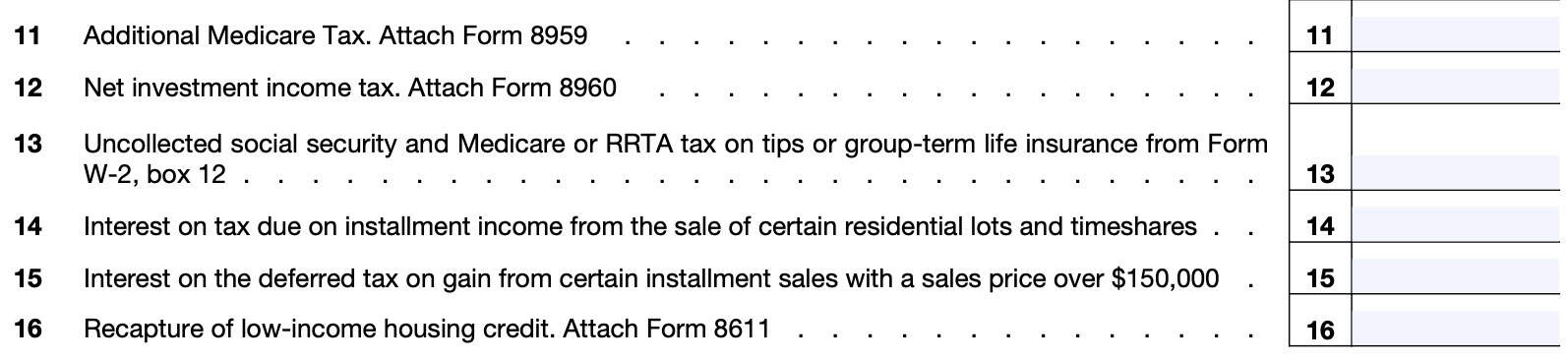

Line 11: Additional Medicare Tax

You may need to file IRS Form 8959 for additional Medicare taxes if your total wage and self-employment compensation was more than the following, based upon tax filing status:

- $125,000 if married filing separately

- $250,000 if married filing jointly, or

- $200,000 if single, head of household, or qualifying surviving spouse

If you are married filing jointly and either you or your spouse had wages or RRTA compensation of more than $200,000, your employer may have withheld additional medicare taxes even if you don’t owe the tax. In this case, you might be able to get a refund of the withheld tax.

Line 12: Net Investment Income Tax

You may need to use IRS Form 8960 to calculate net investment income tax if your adjusted gross income (AGI), from Line 11 on your Form 1040, exceeds:

- $125,000 for married couples filing separately

- $250,000 for married couples filing jointly or a qualifying surviving spouse

- $200,000 for single taxpayers or heads of household

If you have foreign income, and you file IRS Form 2555, you may need to file IRS Form 8960 if your AGI exceeds:

- $13,000 for married couples filing separately

- $138,000 for married couples filing jointly or a qualifying surviving spouse

- $88,000 for single taxpayers or heads of household

If you owe net investment income tax, enter that amount in Line 12.

Line 13

If you owe uncollected Social Security & Medicare or RRTA tax on tips or group life insurance, you should see this on your Form W-2, in Box 12. This tax would appear with one of the following codes in Box 12:

- Code A: Uncollected social security or RRTA tax on tips

- Code B: Uncollected Medicare tax on tips (but not Additional Medicare Tax)

- Code M: Uncollected social security or RRTA tax on taxable cost of group-term life insurance over $50,000 (former employees only)

- Code N: Uncollected Medicare tax on taxable cost of group-term life insurance over $50,000 (but not Additional Medicare Tax) (former employees only)

Line 14

In Line 14, enter any interest on taxes due for installment income from the sale of certain residential lots and timeshares under Internal Revenue Code Section 453(l)(3).

Line 15

For Line 15, enter interest on the deferred tax on gain from certain installment sales with a sales price over $150,000 under IRC Section 453A(c).

Line 16: Recapture of low-income housing credit

If applicable, enter any recapture of low-income housing credit you may have calculated on IRS Form 8611.

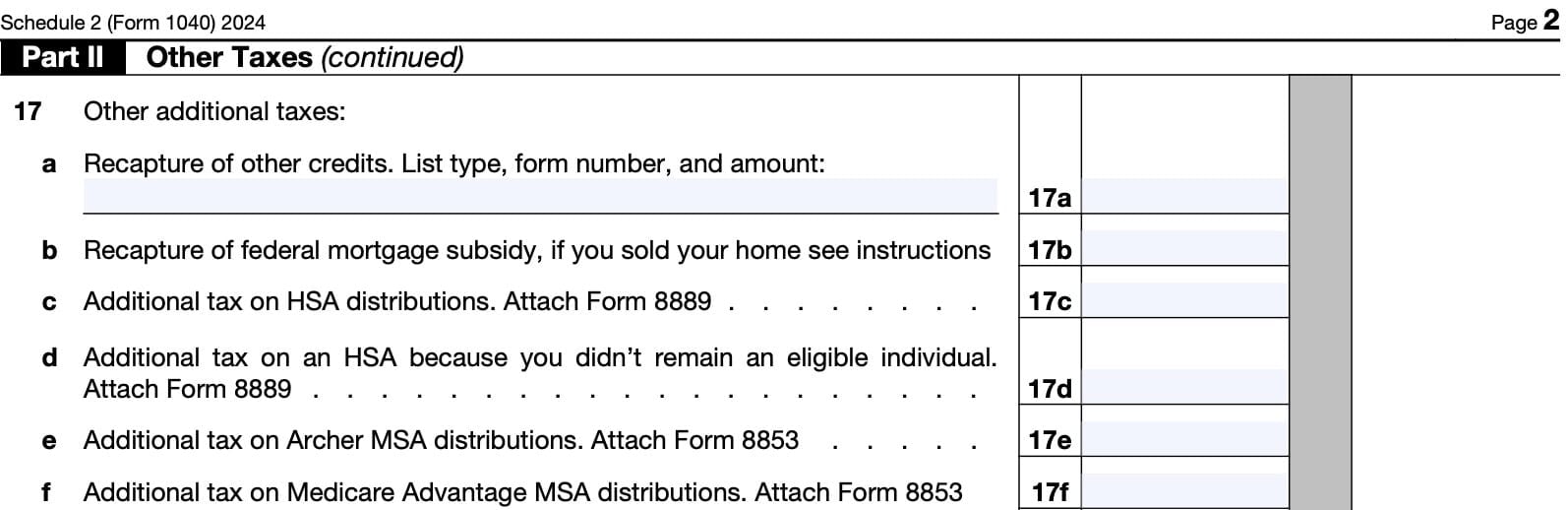

Line 17: Other additional taxes

For Line 17, we will capture a variety of additional taxes and other tax items. This might include credit recaptures, certain payments or items of taxable income, or calculated interest.

Let’s start with Line 17a.

Line 17a: Recapture of other credits

In Line 17a, enter the total of the following tax credits that may have been recaptured:

- Investment credit from IRS Form 4255

- Identify as ICR on Line 17a

- Indian employment credit from IRS Form 8845

- Identify as IECR

- New markets credit from IRS Form 8874

- Identify as NMCR

- Credit for employer-provided childcare facilities from IRS Form 8882

- Identify as ECCFR

- Alternative motor vehicle credit from IRS Form 8910

- Identify as AMVCR

- Alternative fuel vehicle refueling property credit from IRS Form 8911

- Identify as ARPCR

- Qualified plug-in electric drive motor vehicle credit from IRS Form 8936

- Identify as 8936R

Line 17b: Recapture of federal mortgage subsidy

If you sold your home during the tax year and it was financed (in whole or in part) from the proceeds of any tax-exempt qualified mortgage bond or you claimed the mortgage interest credit, you may owe a recapture tax on the mortgage subsidy.

If so, you will need to complete IRS Form 8828 to calculate the mortgage subsidy recapture. Enter the recaptured amount here.

Line 17c: Additional tax on HSA distributions

In Line 17c, enter any additional tax on health savings account (HSA) distributions you received, that you reported on IRS Form 8889, Line 17b.

Line 17d

In Line 17d, enter any additional tax you incurred for failure to remain an eligible individual during the testing period. You’ll find this tax on IRS Form 8889, Line 21.

Line 17e: Additional tax on Archer MSA distributions

On Line 17e, enter the additional tax on Archer MSA distributions from IRS Form

8853, Line 9b.

Line 17f: Additional tax on Medicare Advantage MSA Distributions

Enter any additional tax on Medicare Advantage MSA distributions. You’ll find these on IRS Form 8853, Line 13b.

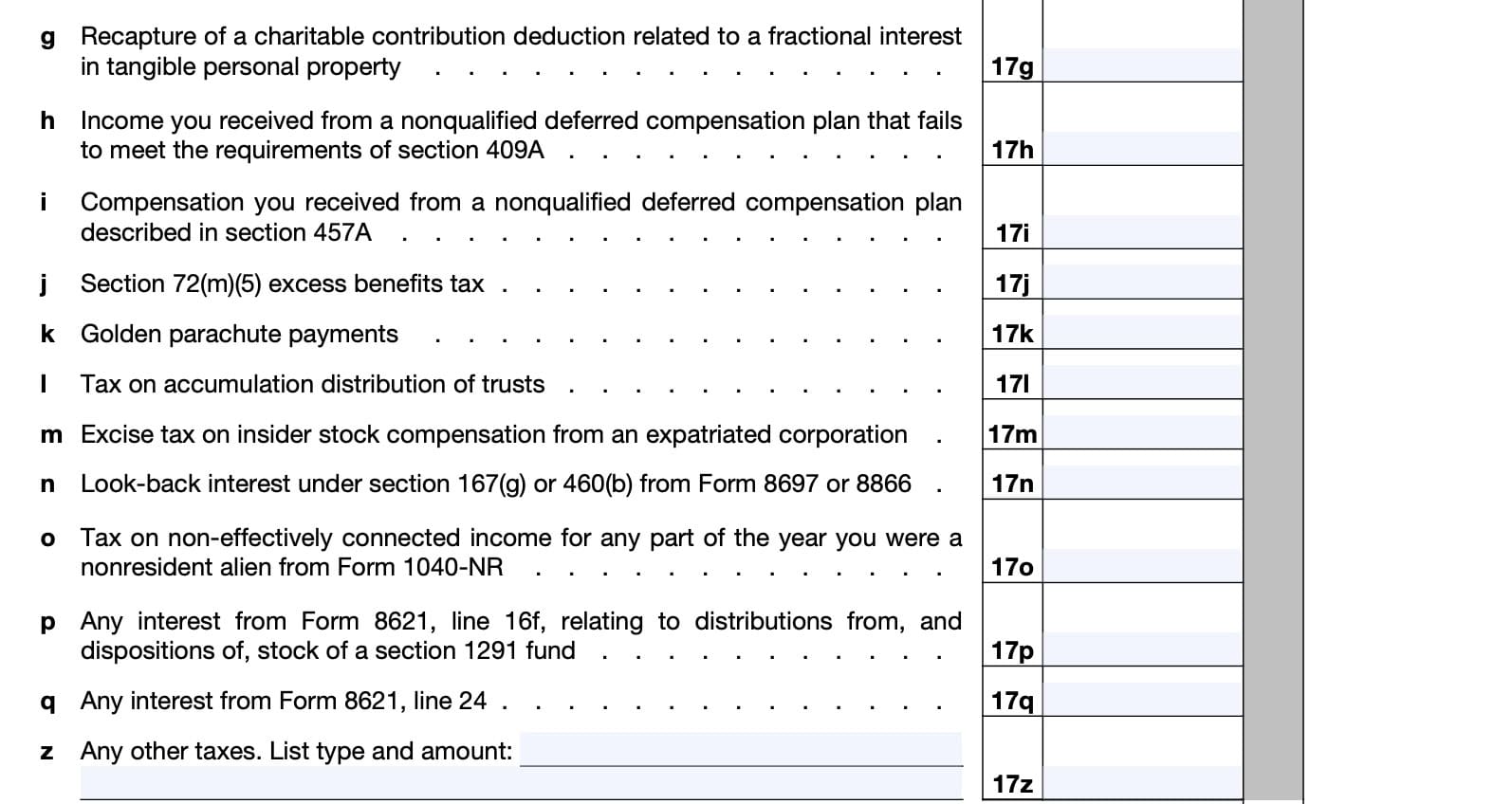

Line 17g

For Line 17g, enter any additional tax on the recapture of a charitable contribution deduction relating to a fractional interest in tangible personal property.

See IRS Publication 526, Charitable Contributions for more tax information.

Line 17h

If you received additional income from a nonqualified deferred compensation plan that does not meet the requirements outlined in IRC Section 409A, you may owe additional taxes.

You should notice this income in either:

- Box 12 of IRS Form W-2, code Z

- Box 15 of IRS form 1099-MISC

The tax is 20% of the amount required to be included in income plus an interest amount determined under IRC Section 409A(a)(1)(B)(ii).

Line 17i: Compensation from a nonqualified deferred compensation plan

In Line 17i, enter any additional tax on compensation you received from a nonqualified deferred compensation plan described in IRC Section 457A if the compensation would have been includible in your income in an earlier year except that the amount wasn’t determinable until the current tax year.

If applicable, the additional tax tax is 20% of the amount required to be included in income plus

an interest amount determined under IRC Section 457A(c)(2).

Line 17j: Section 72(m)(5) Excess Benefits Tax

If applicable, enter any excess benefits tax as defined in IRC Section 72(m)(5). IRS Publication 560, Retirement Plans for Small Business, contains additional details.

Line 17k: Golden parachute payments

If you received an excess parachute payment (EPP), you must pay a 20% tax on it. You will notice this tax in Box 12 of Form W-2 with code K.

If you received a Form 1099-MISC, the tax is 20% of the EPP shown in Box 14. Enter this amount on Line 17k.

Line 17l: Tax on accumulation distribution of trusts

If you owe tax on accumulation distribution of trusts, you’ll likely have to report that tax on IRS Form 4970. If applicable, enter that tax on Line 17l.

Line 17m: Excise tax on insider stock compensation

In Line 17m, enter any excise tax on insider stock compensation from an expatriated corporation. IRC Section 4985 contains additional details.

Line 17n: Look-back interest

If you owe look-back interest, you may have to file one of the following tax forms:

- IRS Form 8697: IRC Section 460(b)

- IRS Form 8886: IRC Section 167(g)

As applicable, enter the look-back interest in Line 17n.

Line 17o: Tax on non-effectively connected income

Enter any tax on non-effectively connected income for any part of the year you were a nonresident alien. If applicable, you may find additional tax information in the form instructions for IRS Form 1040-NR.

Line 17p

For Line 17p, enter any interest amount from IRS Form 8621, Line 16f.

This interest is charged on each net increase in tax as it relates to distributions from, and dispositions of, stock of a Section 1291 fund.

Line 17q

Enter any interest amount from Line 24 of IRS Form 8621. This is the accrued interest on deferred tax.

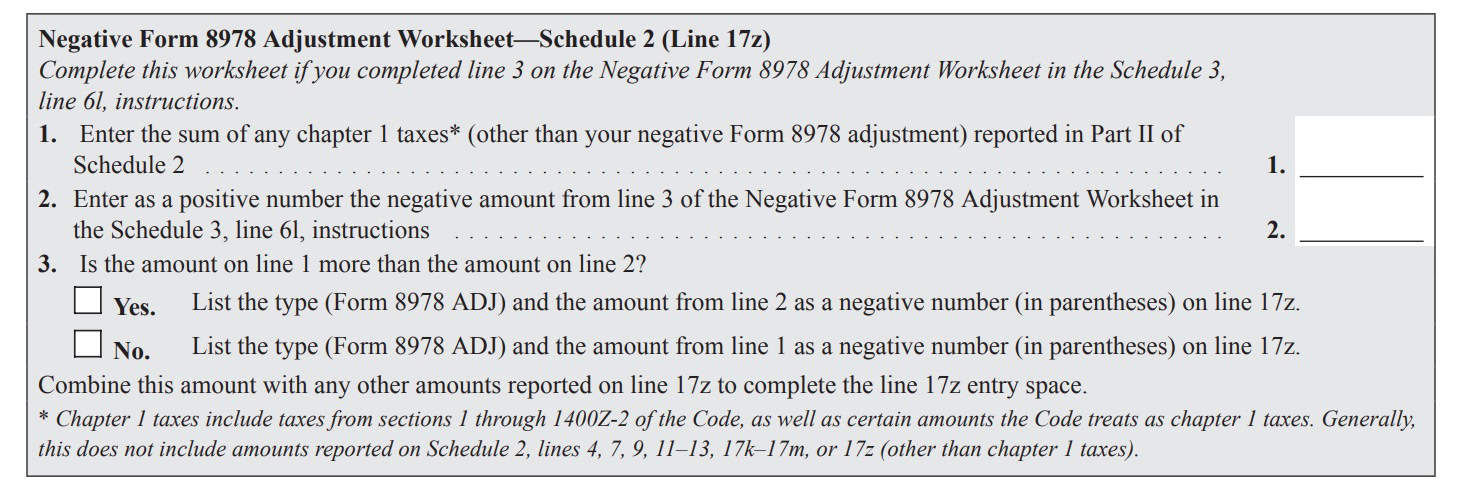

Line 17z

Use this line to report any other taxes not determined elsewhere.

For example, if you filed IRS Form 8978, you will need to complete the following worksheet if you:

- Completed the Negative Form 8978 Adjustment Worksheet in the Schedule 3, Line 6l instructions

- Line 3 from that worksheet is a negative number

As applicable, list the amount and type of each tax.

Line 18: Total additional taxes

Add Lines 17a through 17z. Enter the result in Line 18.

Line 19: Recapture of net EPE from IRS Form 4255

Enter the recapture amount of the net EPE claimed on Form 4255, Line 1d, Column (l) related to the credit from IRS Form 3468, Part IV.

Line 20: Section 965 net tax liability installment

If applicable, enter this number as calculated on IRS Form 965-A.

Line 21: Total other taxes

Add the following lines:

Enter this amount here and on Line 23b on your annual income tax return.

Video walkthrough

Watch this instructional video to learn more about using IRS Schedule 2 to report additional taxes with your regular income tax return.

Do you use TurboTax?

If you don’t, is it because the choices are overwhelming to you?

If so, you should check out our TurboTax review page, where we discuss each TurboTax software product in depth. That way, you can make an informed decision on which TurboTax offering is the best one for you!

Click here to learn more about which TurboTax option is best for you!

Frequently asked questions

IRS Schedule 2 helps taxpayers calculate any additional tax payments that might be required when filing their tax return. The purpose of Schedule 2 is for taxpayers to report additional taxes that can’t be entered directly on their income tax return.

Taxpayers who owe other taxes or need to make an excess advance premium tax credit repayment, may need to file IRS Schedule 2 with their tax return to determine their total tax liability. Examples include self-employment tax, household employment taxes, or alternative minimum tax.

Where can I find IRS Schedule 2?

You may find IRS Schedule 2, along with additional forms, on the IRS website. For easier access, we’ve attached the latest version of IRS Schedule 2 to this article.

Related tax articles

This tax form is one of the fillable tax forms provided by the Internal Revenue Service, to help taxpayers reduce their tax preparation costs. To see more forms like this, visit our free fillable tax forms page, where you’ll also find articles like this.

Unlike the IRS, our articles contain step by step instructions for each tax form, as well as video walkthroughs. You can also check out all of our videos by subscribing to our YouTube channel!